Modern Economy

Vol. 3 No. 1 (2012) , Article ID: 16788 , 13 pages DOI:10.4236/me.2012.31018

Schooling and Assets Ownership

Faculty of Economics, Kyushu University, Fukuoka, Japan

Email: bassojawara@yahoo.co.jp

Received July 3, 2011; revised September 2, 2011; accepted September 29, 2011

Keywords: Education; Asset Holdings; Africa; Senegal

ABSTRACT

We use the 1994, 2001 and 2005 Senegalese households’ surveys to examine to what extent the differences in asset ownership are associated with differences in education levels. The assets are mainly classified into savings, house, car/vehicle and household furniture while the education levels considered are the primary, secondary and university education. The results of the estimations show that education can play a significant role in the holding of household durables or house comfort related assets such as refrigerator and air conditioner. Besides, the findings show that more educated individuals are more likely to have net savings. The results of the stratified samples (rural vs urban and male vs female) show that secondary/tertiary education and most of the assets are positively and significantly associated, implying an intensive promotion of higher education. The results suggest an increase of the level of compulsory education. The results of the present study are modest and very indicative in the sense that the lack of various financial and productive assets does not help drawing straightforward conclusions.

1. Introduction

Assets are well-recognized as playing a determinant role in reducing the variability of consumption in developing countries’ environments characterized by income risk and the absence of sound credit markets [1]. For example, Rosenzweig and Wolpin [2] and Swinton [3] have shown that the sales of livestock can help households to maintain consumption following adverse income shocks. Besides, alternative levels of education affect an individual’s holdings of assets [4]. In the specific case of Ghana, Aryeetey [5] has found that livestock seems to be favored most among those with a little education while avoided by those with no or high levels of education. Differences in education levels seem to be associated with the composition and types of assets owned by households [4,5].

These observations are the starting point for this study. We examine the association between education levels and asset ownership using data from the 1994-1995 First Senegalese Household Survey (Enquête Sénégalaise Auprès des Ménages, commonly known as ESAM-I), the 2001-2002 Second Senegalese Household Survey (Enquête Sénégalaise Auprès des Ménages, commonly known as ESAM-II) and the 2005 Senegal Poverty Monitoring Survey (Enquête de Suivi de la Pauvreté au Sénégal, commonly known as ESPS-2005). The main idea behind the principal objective of the study is that since education is well-known to provide productive and allocative skills and positively impacting on individuals’ well-being, more educated people are expected to own assets with comparatively high returns. We compare the association between each of our education levels (primary, secondary and university education) and the four categories of assets owned by households namely the savings, house, car and households durables related assets1. This allows understanding as to what extent education can help households diversify their assets and to which types of assets educated individuals are likely to invest. The results of this study are indicative in the sense that we lack data on various other productive assets (livestock, for example) and the disaggregated savings.

Although studies on the association between education levels and asset ownership are scarce, especially for the case of developing countries, researchers have tried to investigate the question. For instance, Bradley and Graham [4] have used a sample of young married couples in Illinois to determine to what extent differences in the composition of assets can be explained by the differences in educational background. Through a descriptive data analysis, Aryeetey [5] has also explored the characteristics of households and asset holdings in rural Ghana. The correspondence between asset types and education of the head of household shows that more educated people are more likely to hold their assets in the form of land and non-farm enterprise assets. To the knowledge of the author, the association between education levels and assets’ holdings is not empirically examined in the case of developing countries in general and the case of Senegal in particular.

Senegal can be a useful study case because it is fairly representative of other low income countries with an economy mainly based on the primary sector with approximately more than 70 percent of the population in the agriculture. Senegal can be representative of most of West African countries with the majority of populations’ holdings in the form of durables, land and livestock related assets.

The paper proceeds in five sections. Section 2 gives some background information about the relation between assets and poverty; and education and assets. Section 3 presents an overview of the state of selected assets ownership in Senegal. Section 4 specifies the econometric model, describes the data sources and estimation method. Section 5 presents the empirical results. The last section concludes the paper.

2. Background

2.1. Asset and Poverty

Academics and practitioners have started to investigate the relationship between asset and poverty in the 1980s [6]. However, the various studies are mainly related to developed countries in general and the United Stated in particular. Grosso modo, two views can be distinguished: on the one hand, the supporters of asset-based welfare and on the other hand, the critics of the asset-based welfare [7].

Various arguments are advanced in favor of the view that assets can help reduce poverty. One argument is that asset-ownership yields an independent “asset-effect”, meaning that it urges individuals to save more and act in a more responsible manner [7]. That is, owing an asset creates an orientation toward the future [6]. This rationale is also shared by Sherraden [8] when he notes that owing assets provides a cushion against risk and usually makes it possible to acquire more assets. Another argument with respect to the role of assets in reducing poverty is their preventive as well as curative capabilities [8]. In fact, this view means that owing an asset can help individuals to not fall into poverty and the already-poor to easily escape from it.

Assets are a proxy for well-being. This view is also closely related to the asset-based welfare. In fact, asset is considered as a proxy for well-being in the sense that the stock of wealth an individual holds (and not just the income and consumption) should be seen as important when assessing the well-being [9].

It is to be noticed that, though the evidence on the asset-ownership reducing poverty capabilities is still modest, Gamble and Prabhakar [7] has reviewed the literature and suggested that there are reasons for thinking on the important role of assets. Given the association between assets and poverty as well the assimilation of assets to wealth and wellbeing, it is necessary to look at the main factors influencing their ownership. Although factors such as the policies designed to facilitate the ownership of assets and the transfers such as bequests are determinant for the asset ownership, we focus on the role of education and some main households’ characteristics.

Figure 1 describes the approach underlying the association between education and assets ownership in this study. In fact, the figure shows that education can affect poverty status through an increase of income (we called it market or pecuniary effect of education). This approach means that education increases the productivity of individuals who in turn get higher wages that can help them get out of poverty. This relationship is depicted by the bold line from education to poverty. On the other side, education can also influence the status of poverty through nonmarket or non-pecuniary channels such as, among other factors, the assets ownership and health status. In addition, it is possible to have an alternative reading of Figure 1. In fact, the assets and income constitute the wealth of individuals. Insofar as education affects wealth which in turn determines the poverty status of the households, we can think of the relationship between education and poverty as acting through the assets’ channel. This approach is shown in Figure 1 by the dashed line.

2.2. Education and Asset Ownership: Theoretical Background

Education pays both market and nonmarket returns. One of the most cited nonmarket return of schooling is the increased efficiency that education imparts to asset management [4].

Based on past theoretical works, Bradley and Graham [4] have established a simple model showing how education can be associated with the ownership and composition of assets. On the one hand, education affects the composition of equilibrium assets in the sense that it is included in the assets function as an argument. In this perspective, alternative levels of schooling are considered as alternative nonmarketable assets and can consequently affect an individuals’ ownership of marketable assets. On the other hand, education affects the assets through the fact that it confers to individuals greater management ability and thus greater productivity. This view means that if two people devote the same amount of time to asset management, the more educated is likely to earn a higher return.

Figure 1. Education and asset ownership.

The theoretical framework developed in Bradley and Graham [4] is described as:

(1)

(1)

where θi is the rate of return on the ith asset, Θi represents the production function that generates the returns, ti is the assets management time, Ai is the total assets held and E is the education level.

The specification in (1) states that the rate of returns to assets depends on the time allocated for their management, the total amount of assets owned and the education level of the assets’ holders. The signs of the different parameters are assumed to be the following:

;

; ;

; (2)

(2)

The first derivative means that, all else equal, people who spend more time on managing their assets will have greater returns. The second derivative means that, ceteris paribus, assets yield decreasing returns. Increasing the amount of assets held produces smaller rates of returns. The third derivative means that, all things equal, compared to the less educated, individuals with higher education are more likely to hold assets with higher returns.

This theoretical framework showing the relationship between education and assets is the basic model underpinning the econometric specification used to deal empirically with the research question in this paper. However, it is noticeable that theoretical models dealing with overlapping generations are also developed to identify which variables influence the assets ownership of children focusing on the role of parents’ assets ownership [10]. We adopt the framework of Bradley and Graham [4] because of its simplicity and the characteristics of our data.

3. Households’ Characteristics and Asset Holdings in Senegal

In this section, we discuss the patterns of assets’ holdings with respect to the household’s education levels throughout the years. The data are taken from ESAM-I, ESAMII and ESPS-2005.

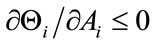

Table 1 shows that during the period 1994-2005 there is an increase in the percentage of individuals owing assets in Senegal. In fact, it is evident that most of the households own their houses (from 62 percent in 1994 to 68 percent in 2005). The decrease in the holding of own house and rented house observed between 2001-2002 and 2005 is mainly due to the high cost of construction and rental [17]. Consequently, the housing supply (construction and rental) seems to be too expensive for most of the households which are basically in the group of low-income. Besides, the car ownership has slightly increased from 5 percent in 1994 to 7 percent in 2005, suggesting the luxurious character and cost attached to cars. The air conditioner ownership has also followed a very slight increase. With respect to the value of net savings, the table shows that their average value has almost doubled from 1994 to 2002.

It is evident that an increase of the average income level of the households has played a great part in the assets’ ownership. However, an increase of the education level of the population with all its benefits in terms of income and orientation toward the future has also partly played a role in the ownership of assets.

Table 1. Assets ownership by Senegalese household heads, 1994-2005.

To get a preliminary idea of whether higher education levels are responsible, among other factors, for the increase in assets ownership, we compute how the holdings of assets have changed within each given education level. Results are displayed in Table 2. The education levels considered are: household heads that have no education, households’ heads that have completed primary education, households’ heads that have completed secondary education and household heads that have completed university education.

The basic conclusion we can draw from Table 2 is that, except for very few exceptional cases where the group of non-educated household heads shows higher increases, assets’ ownership between 1994 and 2005 has increased mainly for people with primary and secondary education. For example, the increase in the ownership of house, bicycle, motorcycle, refrigerator and air-conditioner for people with primary and secondary education are the largest. However, the largest increase in assets such as homephone, TV and radio-receiver by the group of non-educated household heads should also be noted.

Table 2. Assets ownership by education levels, 1994-2005.

Household assets according to education level have changed from 1994-1995 to 2005 (Table 2). With respect to the decrease of rented house, the main reason can be partly due to the fact that housing is too expensive for most of the Senegalese who have low income [17]. Related to the decrease of the car ownership, a probable reason for the constant decrease is the restrictions imposed on the car imports2 which greatly affect the probability to own a car. The decrease in the household durables can partly be explained by the decrease of the revenues which have lead Senegal to be degraded from middle-income country to low-income country [18].

With respect to the net savings, the results show that the value of the savings have increased during the period 1994-2002 for all groups, households with primary education having the highest increase. However, it is to be noticed that the higher the education level, the higher is the value of the net savings, meaning that every year the ranking is, in increasing order, household heads with no education, primary education, secondary education and tertiary education. This increase of the values of the savings is explained by the general increase of the revenues but also the boom observed in the sector of microfinance as evidenced by the proliferation of the decentralized financial systems.

4. Empirical Strategy

4.1. Econometric Specification

To investigate the contribution of alternative explanations in explaining assets’ ownership in Senegal over the period 1994-2005, we regress various types of assets for every year against a series of educational, demographic, occupational and regional dummies characteristics. The econometric model adapted in this study draws from Bradley and Graham [4]. The equation seeking to answer to the question related to the association between education levels and households’ asset holdings after controlling for some relevant characteristics is given by:

(3)

(3)

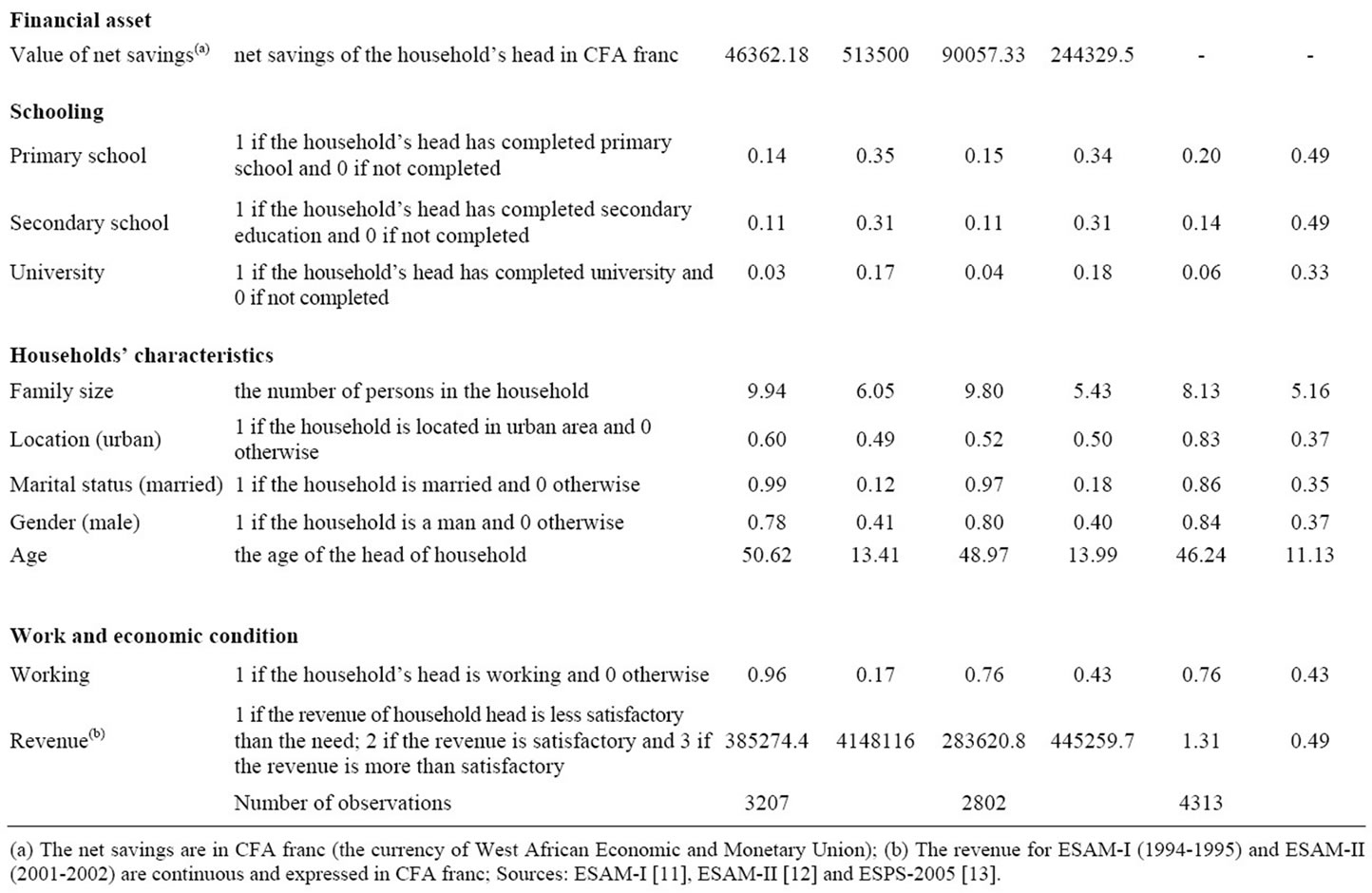

where ASSETSij is household j’s asset i holdings (see Table 3 for a summary statistics and definition of the different dependent variables used). EDU is the set of education levels included to capture the effects of households’ education on asset holdings.

Other independent variables do also affect the asset holdings and consequently need to be considered in the empirical analyses. The controls included are related to the households’ characteristics (family size, marital status, location, gender and age) and working and economic condition (revenue and employment status). See Table 3 for a summary statistics.

From Table 3, most of the assets show little systematic variation and the education levels with it also, implying the probable association between assets ownership and schooling. The average number of people in the representative household has slightly decreased but remains at the relatively high number of 8 individuals per family. Besides, most of the people considered are married and average age is at least 46 years old in 2005.

4.2. Data Issues and Estimation Method

Data issues Data were extracted from the 1994-1995 First Senegalese Household Survey (ESAM-I) [11], the 2001-2002 Second Senegalese Household Survey (ESAM-II) [12] and the 2005 Senegal Poverty Monitoring Survey (ESPS- 2005) [13].

ESAM-I is a nation-wide survey conducted from March 1994 to April 1995 by the Statistics Direction (Direction de la Prévision et de la Statistique) of the Senegalese Ministry of Finance. Data were collected on 3300 households from three strata, namely Dakar (the capital), other urban areas and rural areas. The database contains rich information on individual characteristics (age, education, gender, occupation and labor activity, marital status, etc), household characteristics (size, structure and composition, living conditions, etc), budget (consumption, incomes, etc.), and wealth (housing, other assets and liabilities, etc.). See DPS [11].

ESAM-II was also a nation-wide survey conducted from May 2001 to March 2002. Approximately 6600 households from all of the regions and departments in Senegal were surveyed using similar sampling strategy as in ESAM-I. However, it contains important information regarding the characteristics of the individuals, households and wealth. See DPS [12].

ESPS-2005 is the first survey conducted in the framework of the global program for the monitoring-assessment of the poverty reduction strategies. It aims at analyzing relevant and easy-to-collect indicators for a regular follow-up of poverty progression in Senegal. ESPS-2005 is a nationally representative sample with a large number of variables allowing seeing various relationships explaining the behaviour and characteristics of the Senegalese households. The information collected are related to education, health, employment, household’s assets and comfort, access to basic community services, viewpoint of the populations vis-à-vis their life conditions and expectations from the government. The data are also related to the priorities and solutions for poverty reduction but also populations’ perception of the institutions. Consequently, the survey provides a large series of variables allowing estimating various valuable indicators at different geo-

Table 3. Summary statistics of the variables used in the regressions.

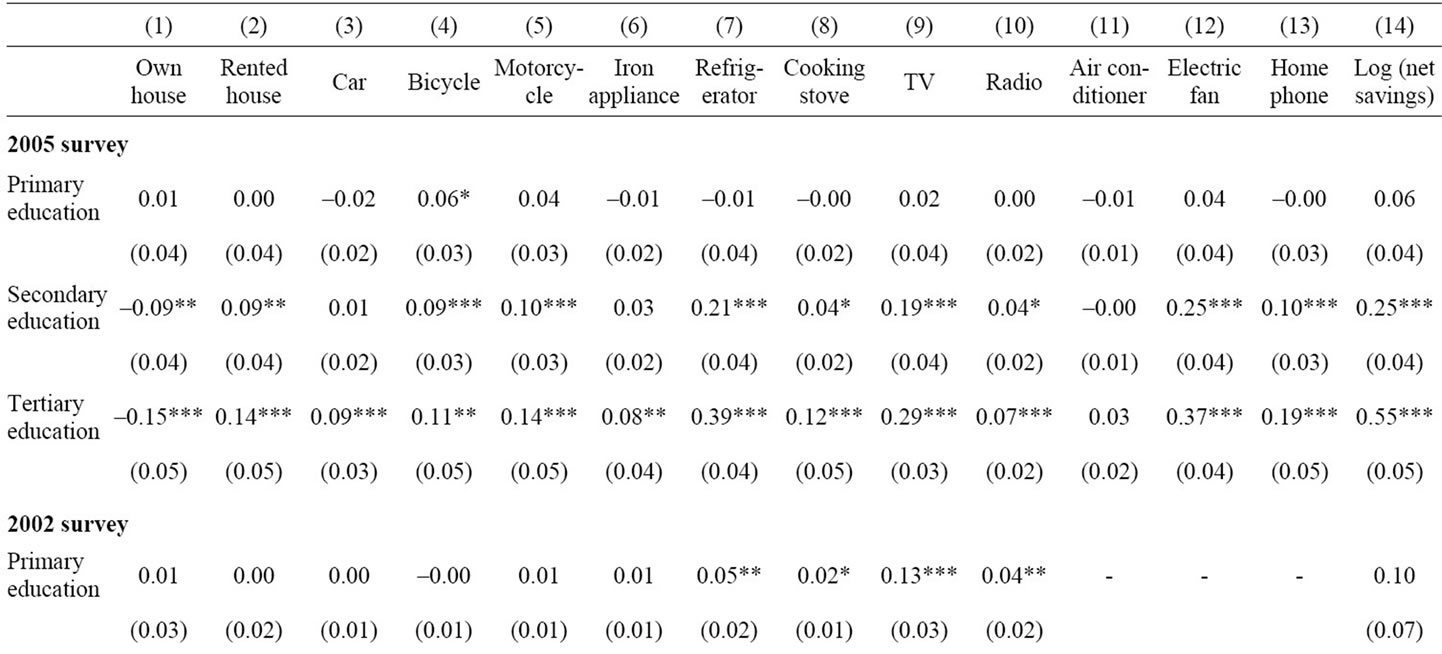

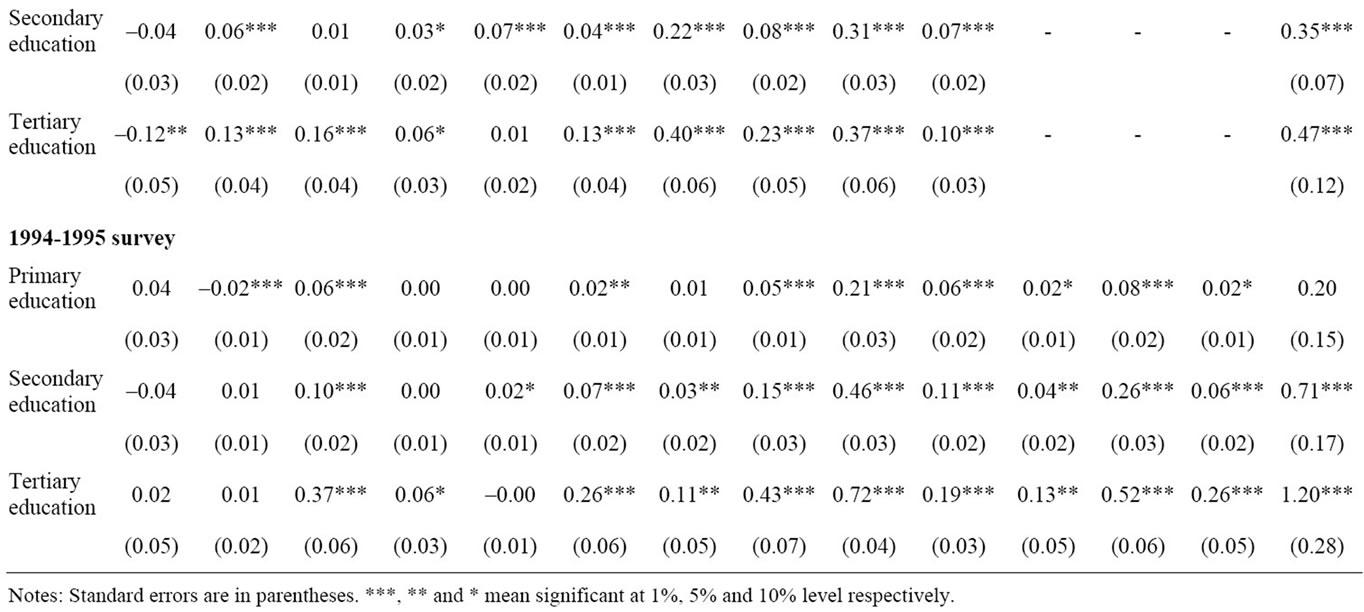

Table 4. Marginal effects of education on households’ assets ownerships.

graphical levels and for many social categories [13].

All three surveys provide basic information that can help to see the relationship existing between education levels and assets ownership. The study samples included household heads who were aged between 16 and 98. After listwise deletion of missing data, the final sample includes at best 3207, 2802 and 4313 heads of households for respectively 1994-1995, 2001-2002 and 2005.

Estimation method In order to examine the association between household’s education levels and asset ownership, probit and ordinary least squares (OLS) models are estimated. Given the nature of the dependent variables, we use probit model when the dependent variable is binary and an OLS estimation method in the case of a continuous dependent variable [14]. In fact, given that in this paper our savings related assets are continuous while the other dependent variables are binary (see Table 3), using respectively the OLS and probit methods is appropriate. We estimate Equation (3) for the years 1994-1995, 2001-2002 and 2005 and for each of the dependant variable.

5. Empirical Results

5.1. Pooled Sample

5.1.1. Impact of Education

The results show that there is no single factor contributing to the ownership of assets but there are several forces working in the same direction to influence the assets’ holding. The results related to the relationship between the other independent variables and assets ownership are available upon request. Table 4 presents the results of the marginal effects of education on assets ownership for 1994- 1995, 2001-2002 and 2005.

With respect to the relationship between education and housing, Table 4 shows that at higher education levels (mainly secondary and university), the probability that household heads own a house is negative, the association being significant in 2005. In 2001-2002, it is only the tertiary education that is significant. This negative relationship between higher education level and home ownership is also found in Bradley and Graham [4]. Their findings show a negative association between husbands’ education and home assets, the relationship being significant for college education. This relationship can be partly explained by the fact that more educated people may invest in assets with higher returns. Although houses provide secure shelter for the households, the selfish and pecuniary inclination of educated individuals may lead them to invest in more financially productive assets. Besides, the expensive character associated with houses ownership can also be a reason.

Individuals with secondary and tertiary education are more likely to rent their residences. In effect, the association between education and rented houses is positive and significant for the secondary and tertiary education except in 1994-1995. This result can reflect the advantages and facilities offered to educated people in terms of rented houses by the employers; mainly various public and private companies rent temporary accommodations for their staffs. In general, governments have adopted provider-based approaches, often acting as social welfare agencies to build houses for those sections of the urban populations who need or deserve special treatment, namely the poor, government workers and those who have provided political support of favors to the ruling party [15].

Considering the relationship between education and vehicle ownership, the results in Table 4 show that households’ heads with tertiary education are more likely to possess a car; this relationship is significant for the three surveys. However, it is also significant for individuals that have completed primary and secondary education when using ESAM-I. This result is in conformity with the findings of Torche and Spilerman [16] that have shown that the education level of the husband/wife’s father is positively associated with the vehicle ownership in Chile in 2003.

For the case of ESAM-I, those with university education are more likely to own a bicycle while those with secondary education are more likely to own a motorcycle. Using ESAM-II, the results show that household heads with secondary and university education have higher probability to have a bicycle while those with secondary education have higher likelihood to get a motorcycle. Regression results from ESPS-2005 show that the higher the education levels the higher the probability to have a bicycle and motorcycle.

Regarding the association between education and households’ furniture, Table 4 shows that the higher the education levels (mainly secondary and tertiary education) the higher the probability to own a flatiron, refrigerator, cooking stove, TV, radio, electric fan and home-phone. Thus, the higher the education levels (mainly secondary and university education), the higher is the probability to have home comfort. Those results suggest the relatively high standard and comfortable lifestyle of high-educated household heads.

Related to the association between education and net savings, Table 4 shows that household heads with higher education (secondary and university) are more likely to have higher net savings; educated people are more likely to hold savings. This result corroborates the findings of Bradley and Graham [4] which show that more educated earn higher returns on their liquid assets.

5.1.2. Impact of the Other Factors

Besides the education levels, households’ characteristics and working and economic conditions are important factors helping in the decision of asset ownerships. For example, the results show that male headed households are more likely to hold motorcycle but less likely to own durable assets such as refrigerator, coking stove, etc. Throughout the surveys, the results show that the association between gender and housing is not robust. This result suggests the tendency for men to hold more productive assets or at least assets helpful for productive purposes while women are more prone to possess household comfort related assets. With respect to the assets owned by women, it should be noted that they can be used in traditional and handicraft industries to generate additional income (for example, food sales, seamstress and household services)3. The gender status is not consistent in the determination of net savings.

The results also show that elderly headed households are more likely to have their own house and less likely to rent their accommodation. This result conveys the probable wealth built up by the elderly throughout their career and along the years.

The marital status of the household head is positively associated with the ownership of comfort related assets; however, the impact is not robust throughout the different surveys.

The family size is significantly associated with the house and vehicle ownership for all three surveys: positive for the vehicle and own house ownership and negative for the rented house.

The findings also show that households living in urban areas are more likely to rent their houses, to own a car and motorcycle and most of the households’ durable assets (refrigerator, TV, etc.). The results are verified for all surveys. This result implies the higher opportunities in terms of job and income offered by the cities relatively to villages where most of the activities are agricultural with low revenues. This difference has motivated the use of stratified samples by location (rural versus urban).

In addition, working household heads are less likely to own their houses (ESAM-II and ESPS-2005) and more likely to rent and possess vehicle (ESPS-2005). The revenue of the household head seems to play a significant role on the asset ownership. In fact, the higher the revenue the higher is the probability to possess vehicle and households durable assets; the impact is significant for all years. These findings mean that the purchasing power of the head of household is very important in the ownership of assets. With respect to the net savings, the results show that married household heads with larger family are more likely to have some savings and potentially more likely to invest. Besides, the results related to the relationship between household head living in urban areas and net savings are not conclusive. The inclusion of the regional dummies has helped to increase the explanatory power of the model. Moreover, the results show the following patterns: household heads in the provinces are more likely to own a motorcycle but less likely to possess a household durable. This result can be explained by the opportunities and development level of the capital relative to the other regions of the country.

The differences observed between male headed and female headed households and between household heads living in urban areas and those living in rural areas and the significant sign associated with the coefficients of the variables “urban” and “male” suggest the segmentation of the sample by gender (female vs male) and location (rural vs urban).

5.2. Stratified Samples

5.2.1. By Gender

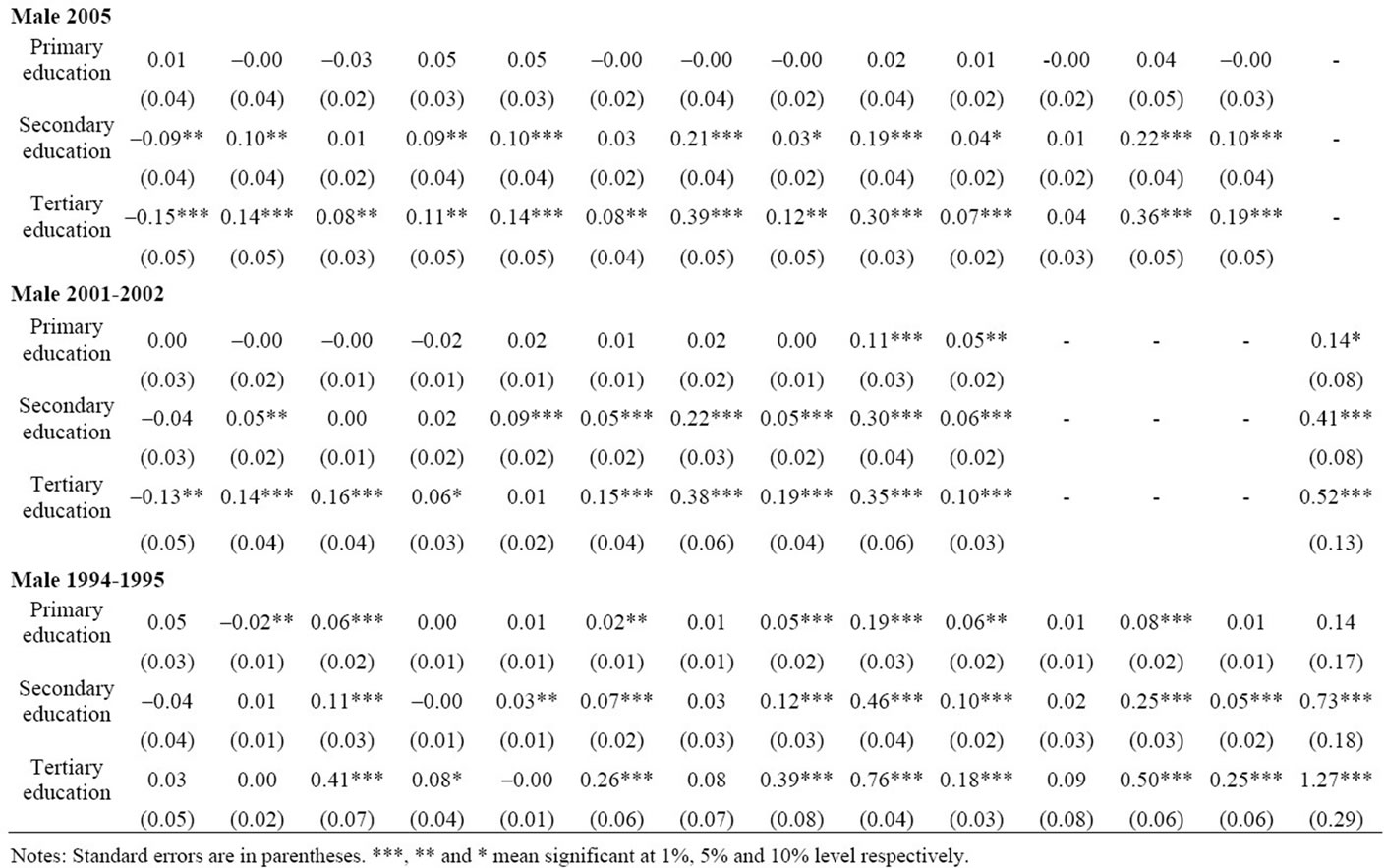

The effects of education by gender show that there is no significant relationship between education and own house ownership in the sample of female headed households while the effect is negative and significant for secondary and university education in 2005. With respect to vehicle ownership (car, bicycle and motorcycle), schooling seems to have a higher effect in 2005 when the sample of female headed households is considered. For example, in 2005, the probability to own a vehicle is approximately 1 percent for the female headed households with university education while it is 0.1 percent for the male headed households. Besides, the results show that it is in the sample of male headed households that individuals with secondary and tertiary education are more likely to own assets. For instance, in the sample of male householdsthe impact of both variables is significant in 11 out of 14 regressions in 2005, 8 out of 15 regressions in 2001- 2002 and 9 out of 15 regressions in 1994-1995 (Table 5).

The marginal effects of age by gender indicate that age is significantly and positively associated with the probability of owning a house and various house facilities among males and females headed households. However, the magnitude is fairly small (approximately 0.01 percent). The family size and location also play a role in the ownership of assets among males and females headed households. The effect of income is important in the probability of owning a house only among the female headed households. However, its impact is significant for the ownership of the other assets among both sexes [Results upon request].

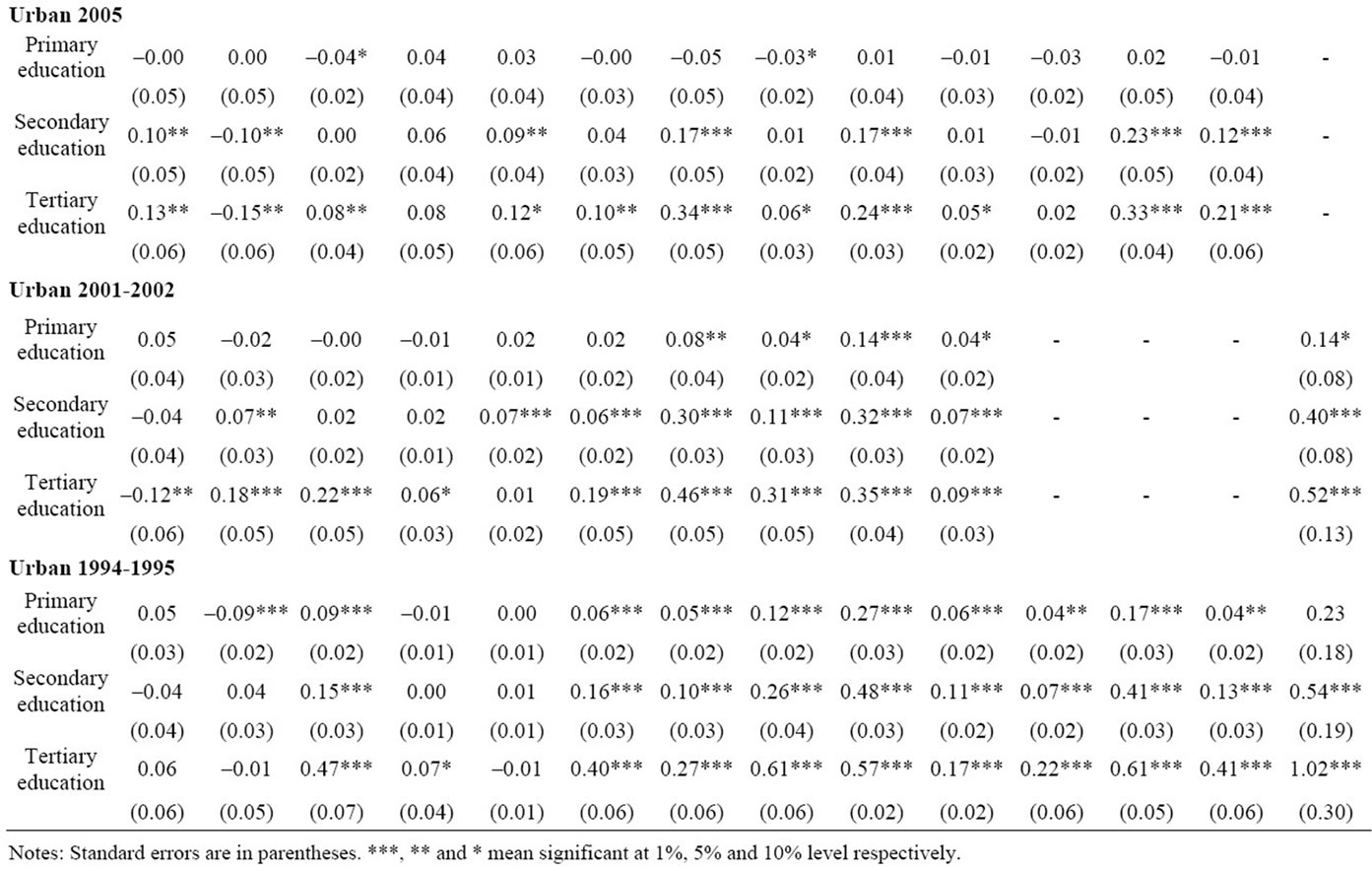

5.2.2. By Location

Table 6 shows that the impact of education is positive and significant for the ownership of house among households living in urban areas and for the 2005 survey. In fact, the impact is around 0.10 percent. Besides, among households living in urban areas, individuals with university education are more likely to own households facilities (7 out of 9 regressions in 2005, 6 out of 6 regressions in 2001-2002 and 10 out of 10 regressions in 1994- 1995). However, for urban areas, secondary education is positively and significantly associated with the ownership of motorcycle, refrigerator, TV, electric fan and home phone in 2005.

The marginal effects of the income by location indicate that the households’ revenue is significantly and positively associated with the ownership of vehicle and household comforts only amongst urban households. Note that the impact has increased from approximately 0.001 percent in 1994-1995 to at least 0.03 percent 2005. Besides, the family size is positively and significantly associated with the probability of households’ furniture and vehicle ownerships among rural and urban households. The impact is, however, very small (around 0.001 percent). The variable “age” is also positively and significantly associated with the ownership of various households’ related assets only among urban households. However, its impact is fairly small and not consistent when we consider all surveys. In addition, the impacts of the marital and working status are not consistent among the rural and urban households and through the surveys.

In conclusion, we can say that while education plays a principal role in the ownership of house and some house comfort related assets, the income and family characteristics of the household head are at least equally important in the assets’ ownership decisions. The following observations can be made with respect to the results of the estimations. First, secondary and tertiary education is

Table 5. Education and assets ownership, the marginal effects (female vs male).

Table 6. Education and assets ownership, the marginal effects (rural vs urban).

associated with the ownership of vehicle and household comfort. However, the impact of education has generally reduced throughout the years. Second, disaggregating the sample allows having an in-depth understanding of the impacts of the different explanatory variables. For example, the impact of education is relatively important when considering male headed households and households living in urban areas. Third, the size of the family seems to be determinant in the assets ownership decisions in Senegal. Besides, the revenue of the head of household plays a significant role in the ownership of car and households comforts related assets only among urban households.

6. Conclusions

Households in developed as well as developing countries hold various types of assets in order to secure themselves from the incertitude of the future but also smooth their consumption behavior. This paper investigates the association between education levels and asset ownership. This study’s objective is based on the presumption that more educated people may be more efficient assets managers than the less educated either because they have more information or because they can make efficient choices. The empirical setting is Senegal and we use the surveys conducted in 1994-1995, 2001-2002 and 2005.

The results of the present study offer some preliminary evidence on how education levels and assets holdings are associated. Also, the role played by the characteristics of the Senegalese family is empirically highlighted. The findings show that besides the economic conditions (revenue), the size of the family also affects the probability of holding assets. More interestingly, individuals with higher education (namely secondary and tertiary) levels are more likely to have vehicles. Secondary and university education seems to be the most decisive in the ownership of households’ durables assets or house comfort (refrigerator, TV).

The disaggregation of the full samples by gender and location has shown that secondary and tertiary education remains important for the assets ownership among urban households. Interestingly, the results show that in 2005 higher education is associated with the house ownership only among urban households. It is also to be noted that the income level and size of the households are signifycantly associated with the ownership of various types of households’ furniture.

The suggestions of the study are very modest and might be more appropriate when considering only urban households. In fact, given the marginal role played by schooling on the assets ownership and the close relationship (although descriptive) between assets holding and poverty, one can indirectly suggest the promotion of education. Basically, the results suggest continuing an intensive promotion of higher education for the Senegalese households in the sense that, as shown throughout the results, the heads of household with higher education (mainly secondary and tertiary education) are more likely to own a house and have comfortable houses, meaning wellequipped. In addition, the findings have shown that individuals with higher education (secondary and university) are more likely to hold some net savings. From one survey to another, we have seen that the direction of the impact is positive.

For an effective promotion of education, the level of compulsory education needs to be reviewed with basically coercive and legal safeguards. The legal system underlying the Senegalese education system should be strengthened in the sense that there are many children of-education-age out of school without the parents being alarmed by the law.

In addition, the results suggest encouraging households to hold some assets (our descriptive results have shown that poverty and asset ownership are related) in the sense that they can be helpful in smoothing the consumption and assisting against the uncertainties. However, care should be taken for this point because poverty can be the explanatory factor behind the assets ownership. What is certain is that schooling is somehow related with both assets and poverty.

7. Acknowledgements

We are indebted to the Agence Nationale de la Statistique et de la Démographie (ANSD) of the Republic of Senegal for providing the datasets and the Ministry of Education, Culture, Sports, Science and Technology (MEXT) of Japan for supporting this research. Helpful comments on this work have been provided by an anonymous referee, Hitoshi Osaka, Hideo Noda and the participants at the Japanese Association for Applied Economics 11th Conference (June 2010, Seinan Gakuin University). We are grateful to Priyanga Dunusinghe, Bhusal Bhim Prasad and Papa Saliou Sarr for encouragement, help and advices. We thank Mazhar Yasin Mughal for checking the manuscript and his suggestions.

REFERENCES

- T. Bundervoet, “Assets, Activity Choices, and Civil War: Evidence from Burundi,” World Development, Vol. 38, No. 7, 2010, pp. 955-965. doi:10.1016/j.worlddev.2009.12.007

- M. Rosenzweig and K. Wolpin, “Credit Market Constraints, Consumption Smoothing, and the Accumulation of Durable Production Assets in Low-Income Countries: Investment in Bullocks in India,” Journal of Political Economy, Vol. 101, No. 2, 1993, pp. 223-244. doi:10.1086/261874

- S. Swinton, “Drought Survival Tactics of Subsistence Farmers in Niger,” Human Ecology, Vol. 16, No. 2, 1998, pp. 123-144. doi:10.1007/BF00888089

- G. M. Bradley and J. W. Graham, “Education and Asset Composition,” Economics of Education Review, Vol. 7, No. 2, 1988, pp. 209-220. doi:10.1016/0272-7757(88)90045-3

- E. Aryeetey, “Household Asset Choice among the Rural Poor in Ghana,” Institute of Statistical, Social and Economic Research, University of Ghana and Cornell University, Accra, 2004.

- M. Miller-Adams, “Building Assets,” In: M. MillerAdams, Eds. Owning Up: Poverty, Asset, and the American Dream, Brookings Institution Press, Washington DC, 2002, pp. 1-22.

- A. Gamble and R. Prabhakar, “Assets and Poverty,” Theoria, Vol. 52, No. 107, 2005, pp. 1-18. doi:10.3167/004058105780956813

- M. Sherraden, “Assets and the Poor: A New American Welfare Policy,” Sharpe Incorporated, New York, 1991.

- W. Paxton, “Introduction,” In: W. Paxton, Eds., Equal Shares? Building a Progressive and Coherent Asset-Based Welfare Policy, Institute for Public Policy Research, London, 2003, pp. 1-8.

- N. S., Chiteji and F. P. Stafford, “Asset Ownership across Generations,” Population Studies Center Research Report No. 00-454, University of Michigan, Ann Arbor, 2000.

- DPS (Direction de la Prévision et de la Statistique), “Deuxième Enquête Sénégalaise auprès des Ménages (ESAM II),” Ministère de l’Economie et des Finances, Dakar, 2002.

- DPS (Direction de la Prévision et de la Statistique), “Première Enquête Sénégalaise auprès des Ménages (ESAM I),” Ministère de l’Economie et des Finances, Dakar, 1995.

- ESPS (Enquête de Suivi de la Pauvreté au Sénégal), Agence Nationale de la Statistique et de la Demographie (ANSD) de la Republique du Senegal, 2005. www.ansd.sn.

- A. M. Jones, “Applied Econometrics for Health Economists: A Practical Guide,” 2nd Edition, Office of Health Economics, London, 2007.

- A. G. Tipple, “The Need for New Urban Housing in SubSaharan Africa: Problem or Opportunity,” African Affairs, Vol. 93, 1994, pp. 587-608.

- F. Torche and S. Spilerman, “Parental Wealth Effects on Living Standards and Assets Holdings: Results from Chile,” ISERP Working Paper 04-06, Columbia University, New York City, 2004.

- A. Fall, “Dakar dans une Spirale Inflationsite,” Les Afriques, Genève, 2008.

- République du Sénégal, “Programme de Développement de l’Education et de la Formation (Education pour tous)”, Ministère de l’Education, 2003.

NOTES

1The definition of assets adopted in this paper is based on the classification made by the World Bank when conducting the different surveys on developing countries. There are four sub-categories under the section “households’ assets”: housing, land, livestock and equipment/facilities. Assets can be described as savings and capital stocks that can be used to generate means for the households to survive or maintain their material wellbeing.

2The Decree No. 2001-71 (January 26th, 2001) has redefined the imports of cars in Senegal and set the legal age of (touristic and light) vehicles to a maximum of five years.

3We thank the reviewer for this suggestion.