Journal of Mathematical Finance

Vol.08 No.01(2018), Article ID:82779,30 pages

10.4236/jmf.2018.81015

Asymptotic Analysis for Spectral Risk Measures Parameterized by Confidence Level

Takashi Kato

Association of Mathematical Finance Laboratory (AMFiL), Tokyo, Japan

Copyright © 2018 by author and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/

Received: January 21, 2018; Accepted: February 25, 2018; Published: February 28, 2018

ABSTRACT

We study the asymptotic behavior of the difference as , where is a risk measure equipped with a confidence level parameter , and where X and Y are non-negative random variables whose tail probability functions are regularly varying. The case where is the value-at-risk (VaR) at a, is treated in [1] . This paper investigates the case where is a spectral risk measure that converges to the worst-case risk measure as . We give the asymptotic behavior of the difference between the marginal risk contribution and the Euler contribution of Y to the portfolio . Similarly to [1] , our results depend primarily on the relative magnitudes of the thicknesses of the tails of X and Y. Especially, we find that is asymptotically equivalent to the expectation (expected loss) of Y if the tail of Y is sufficiently thinner than that of X. Moreover, we obtain the asymptotic relationship as , where is a constant whose value likewise changes according to the relative magnitudes of the thicknesses of the tails of X and Y. We also conducted a numerical experiment, finding that when the tail of X is sufficiently thicker than that of Y, does not increase monotonically with a and takes a maximum at a confidence level strictly less than 1.

Keywords:

Spectral Risk Measures, Quantitative Risk Management, Asymptotic Analysis, Extreme Value Theory, Euler Contribution

1. Introduction

The purpose of this paper is to investigate the asymptotic behavior of the difference

(1.1)

as , where X and Y are fat-tailed random variables (loss variables) and is a family of risk measures. The case where is an a-percentile value-at-risk (VaR), has been treated in [1] , where it was shown that the asymptotic behavior of drastically changes according to the relative magnitudes of the thicknesses of the tails of X and Y (the definition of the VaR is given in (2.1) in the next section). In this paper, we study a progressive case in which is given as a parameterized spectral risk measure, and we obtain similar results as in [1] . In particular, we find that if X and Y are independent and if the tail of X is sufficiently fatter than that of Y, then converges to the expected value as whenever are spectral risk measures converging to a risk measure of the worst case scenario. That is, whenever

(1.2)

for each loss random variable Z in some sense. Our result does not require any specific form for , implying that this property is robust. Furthermore, assuming some technical conditions for the probability density functions of X and Y, we study the asymptotic behavior of the Euler contribution, defined as

(1.3)

(see Remark 17.1 in [2] ), and show that is asymptotically equivalent to as . Here, is a constant determined according to the relative magnitudes of the thicknesses of the tails of X and Y.

We now briefly review the financial background for this study. In quantitative financial risk management, it is important to capture tail loss events by using adequate risk measures. One of the most standard risk measures is the VaR. The Basel Accords, which provide a set of recommendations for regulations in the banking industry, essentially recommend using VaR as a measure of risk capital for banks. VaRs are indeed simple, useful, and their values are easy to interpret. For instance, a yearly 99.9% VaR calculated as

means that the probability of a risk event with a realized loss larger than

is 0.1%. In other words, an amount  of risk capital is sufficient to prevent a default with 99.9% probability. The meaning of the amount

of risk capital is sufficient to prevent a default with 99.9% probability. The meaning of the amount  is therefore easy to understand. However, VaRs are often criticized for their lack of subadditivity (see, for instance, [3] [4] [5] and [6] ). VaRs do not reflect the risk diversification effect.

is therefore easy to understand. However, VaRs are often criticized for their lack of subadditivity (see, for instance, [3] [4] [5] and [6] ). VaRs do not reflect the risk diversification effect.

The expected shortfall (ES) has been proposed as an alternative risk measure that is coherent (in particular, subadditive) and tractable, with the risk amount at least that of the corresponding VaR. Note that there are various versions of ES, such as the conditional value-at-risk (CVaR), the average value-at-risk (AVaR), the tail conditional expectation (TCE), and the worst conditional expectation (WCE). These are all equivalent under some natural assumptions (see [4] [7] [8] , and [9] ). It should be noted that the Basel Accords have also considered recently the adoption of ESs as a minimal capital requirement, in order to better capture market tail risks (see for instance [10] and [11] ).

A spectral risk measure (SRM) has been proposed as a generalization of ESs, in [3] . SRMs are characterized by a weight function  that represents the significance of each confidence level for the risk manager. SRMs are equivalent to comonotonic law-invariant coherent risk measures (see Remark 1 in the next section).

that represents the significance of each confidence level for the risk manager. SRMs are equivalent to comonotonic law-invariant coherent risk measures (see Remark 1 in the next section).

VaRs and ESs as risk measures depend on a confidence level parameter . We let

. We let  (resp.,

(resp., ) denote the VaR (resp., ES) with confidence level a. When a is close to 1, the values of

) denote the VaR (resp., ES) with confidence level a. When a is close to 1, the values of  and

and  are increasing without bound as in (1.2). The parameter a corresponds to the risk aversion level of the risk manager. Higher values of a indicate that the risk manager is more risk-averse and evaluates the tail risk as more severe.

are increasing without bound as in (1.2). The parameter a corresponds to the risk aversion level of the risk manager. Higher values of a indicate that the risk manager is more risk-averse and evaluates the tail risk as more severe.

In this paper, we consider a family  of SRMs parameterized by the confidence level a. We make a mathematical assumption that intuitively implies situation (1.2) and investigate the asymptotic behaviors of (1.1) and (1.3) as

of SRMs parameterized by the confidence level a. We make a mathematical assumption that intuitively implies situation (1.2) and investigate the asymptotic behaviors of (1.1) and (1.3) as , when the tail probability function of X (resp., Y) is regularly varying with index

, when the tail probability function of X (resp., Y) is regularly varying with index  (resp.,

(resp., ). Our main theorem asserts that the asymptotic behaviors of (1.1) and (1.3) strongly depend on the relative magnitudes of

). Our main theorem asserts that the asymptotic behaviors of (1.1) and (1.3) strongly depend on the relative magnitudes of  and

and . Note that our results include the case

. Note that our results include the case , the inclusion of which was discussed as a future task in [1] .

, the inclusion of which was discussed as a future task in [1] .

The rest of this paper is organized as follows. In Section 2, we prepare the basic settings and introduce the definitions for SRMs based on confidence level. In Section 3, we give our main results. We numerically verify our results in Section 4. Finally, Section 5 summarizes our studies. Throughout the main part of this paper, we assume that X and Y are independent. The more general case where X and Y are not independent is studied in Appendix 1. All proofs are given in Appendix 2.

2. Preliminaries

Let  be a standard probability space and let

be a standard probability space and let  denote a set of non-negative random variables defined on

denote a set of non-negative random variables defined on . For each

. For each , we denote by

, we denote by  the distribution function of Z and by

the distribution function of Z and by  its tail probability function; that is,

its tail probability function; that is,  and

and . Moreover, for each

. Moreover, for each , we define

, we define

(2.1)

(2.1)

Note that  is exactly the left-continuous version of the generalized inverse function of

is exactly the left-continuous version of the generalized inverse function of .

.

We now introduce the definition of SRMs.

Definition 1

1) A Borel measurable function  is called an admissible spectrum if

is called an admissible spectrum if  is right-continuous, non-decreasing, and satisfies

is right-continuous, non-decreasing, and satisfies

(2.2)

(2.2)

2) A risk measure  is called an SRM if there is an admissible spectrum

is called an SRM if there is an admissible spectrum  such that

such that , where

, where

Remark 1 SRMs are law-invariant, comonotonic, and coherent risk measures. However, as shown in [12] [13] , and [14] , if  is atomless, then for any law-invariant comonotonic convex risk measure

is atomless, then for any law-invariant comonotonic convex risk measure , there is a probability measure

, there is a probability measure  on

on  such that

such that

(2.3)

(2.3)

for each . This is due to the generalized Kusuoka representation theorem (Theorem 4.93 in [12] ), where

. This is due to the generalized Kusuoka representation theorem (Theorem 4.93 in [12] ), where  is the a-percentile expected shortfall of Z:

is the a-percentile expected shortfall of Z:

(2.4)

(2.4)

Moreover, such a  is always coherent and satisfies the Fatou property [13] . Furthermore, representation (2.3) can also be rewritten as

is always coherent and satisfies the Fatou property [13] . Furthermore, representation (2.3) can also be rewritten as , where

, where

Here, it is easy to see that  is non-negative, non-decreasing, right-continuous, and satisfies

is non-negative, non-decreasing, right-continuous, and satisfies

meaning that  is an admissible spectrum (see [15] ). Therefore, any law-invariant comonotonic convex (or coherent) risk measure is completely characterized as an SRM. Arguments similar to those above, replacing

is an admissible spectrum (see [15] ). Therefore, any law-invariant comonotonic convex (or coherent) risk measure is completely characterized as an SRM. Arguments similar to those above, replacing  with

with , where

, where , can be found in [15] and [16] .

, can be found in [15] and [16] .

Next, we introduce a family  of SRMs parameterized by the confidence level a.

of SRMs parameterized by the confidence level a.

Definition 2 Let  be a family of admissible spectra and let

be a family of admissible spectra and let . Then

. Then  is called a set of confidence-level-based spectral risk measures (CLBSRMs) if

is called a set of confidence-level-based spectral risk measures (CLBSRMs) if

(2.5)

(2.5)

where  is a probability measure on

is a probability measure on  defined by

defined by  and

and  is the Dirac measure with unit mass at 1.

is the Dirac measure with unit mass at 1.

Condition (2.5) formally implies (1.2). Indeed, if  is a bounded random variable with a distribution function that is continuous and strictly increasing on

is a bounded random variable with a distribution function that is continuous and strictly increasing on , where

, where , then the function

, then the function  is bounded and continuous, so that (2.5) gives

is bounded and continuous, so that (2.5) gives

where we recognize . Moreover, we see that

. Moreover, we see that

Lemma 1 Relation (2.5) is equivalent to

(2.6)

(2.6)

We now give some examples of CLBSRMs.

Example 1. Expected Shortfalls

defined by (2.4) is a typical example of a CLBSRM. The corresponding admissible spectra are given as

defined by (2.4) is a typical example of a CLBSRM. The corresponding admissible spectra are given as

It is easy to see that (2.5) does hold. Indeed, for any bounded continuous function f defined on , we see that

, we see that

due to the bounded convergence theorem. Equivalently, we can also check that  satisfies (2.6).

satisfies (2.6).

is characterized as the smallest law-invariant coherent risk measures that are greater than or equal to

is characterized as the smallest law-invariant coherent risk measures that are greater than or equal to  [14] . Note that if the distribution function of the target random variable Z is continuous, then

[14] . Note that if the distribution function of the target random variable Z is continuous, then  coincides with

coincides with , where

, where

(see [8] for details).

Example 2. Exponential/Power SRMs

An admissible spectrum f corresponding to an SRM  represents the preferences of a risk manager for each quantile of the loss distribution. Therefore, the form taken by f corresponds to the manager’s risk aversion, which is also described in terms of utility functions in classical decision theory. Recently, the relation between expected utility functions and SRMs has been studied, though it has not been entirely resolved. Here we introduce some examples of SRMs based on specific utility functions.

represents the preferences of a risk manager for each quantile of the loss distribution. Therefore, the form taken by f corresponds to the manager’s risk aversion, which is also described in terms of utility functions in classical decision theory. Recently, the relation between expected utility functions and SRMs has been studied, though it has not been entirely resolved. Here we introduce some examples of SRMs based on specific utility functions.

The exponential utility function is a typical example of tractable utility functions

where p denotes the profit-and-loss ( indicating profit) and g characterizes the degree of risk preference. We focus on the case

indicating profit) and g characterizes the degree of risk preference. We focus on the case  so that

so that  describes a risk-averse utility function. We transform the parameter g into the confidence level

describes a risk-averse utility function. We transform the parameter g into the confidence level  using

using . Note that the original parameter g can be recovered using the inverse

. Note that the original parameter g can be recovered using the inverse . The exponential utility of the loss l with confidence level a is then given as

. The exponential utility of the loss l with confidence level a is then given as . Cotter and Dowd [17] have proposed an SRM

. Cotter and Dowd [17] have proposed an SRM  based on the exponential utility by constructing an admissible spectrum

based on the exponential utility by constructing an admissible spectrum  for some

for some , so that

, so that  satisfies (2.2). Then,

satisfies (2.2). Then,  must be set as

must be set as , giving

, giving

Note that the theoretical validity of the above method is still unclear. Other methods to adequately construct SRMs from exponential utility functions have been discussed in [18] [19] , and [20] , but no definite answer has been reached. In particular, it is pointed out in [18] that there exists no general consistency between expected utility theory and SRM-decision making. In any case, we can easily verify that  as defined above satisfies (2.5)-(2.6), which implies that

as defined above satisfies (2.5)-(2.6), which implies that  is actually a CLBSRM.

is actually a CLBSRM.

Similarly to the above, an SRM  based on the power utility function has been studied in [21] . After changing the risk aversion parameter to the confidence level

based on the power utility function has been studied in [21] . After changing the risk aversion parameter to the confidence level  as above,

as above,  is given as

is given as

We can also verify that  is a CLBSRM.

is a CLBSRM.

We now introduce some notations and definitions used in asymptotic analysis and extreme value theory.

Let f and g be positive functions defined on , where

, where  and

and . We say that f and g are asymptotically equivalent (denoted as

. We say that f and g are asymptotically equivalent (denoted as ) as

) as  if

if . When

. When , we say that f is regularly varying with index

, we say that f is regularly varying with index  if it holds that

if it holds that  for each

for each . Moreover, we say that f is ultimately decreasing if f is non-increasing on

. Moreover, we say that f is ultimately decreasing if f is non-increasing on  for some

for some . For more details, we refer the reader to [22] and [23] .

. For more details, we refer the reader to [22] and [23] .

3. Main Results

Our main purpose is to investigate the property of (1.1) for a CLBSRM  and random variables

and random variables  whose distributions are fat-tailed. To consider this case, we assume that

whose distributions are fat-tailed. To consider this case, we assume that  and

and  are regularly varying functions with indices

are regularly varying functions with indices  and

and , respectively. That is,

, respectively. That is,  for each

for each  and

and

(3.1)

(3.1)

for some .

.

In [1] , we study the asymptotic property of (1.1) as  when

when . The results display the following five patterns: (i)

. The results display the following five patterns: (i) , (ii)

, (ii) , (iii)

, (iii) , (iv)

, (iv) , and (v)

, and (v) . In cases (iv) and (v), we consider the difference

. In cases (iv) and (v), we consider the difference  instead of

instead of , and the results are restated consequences of cases (i) and (ii). Hence, we assume here that

, and the results are restated consequences of cases (i) and (ii). Hence, we assume here that  and focus on cases (i)-(iii) only. We further assume that

and focus on cases (i)-(iii) only. We further assume that . This assumption guarantees the integrability of X and Y (see, for instance, Proposition A3.8 in [23] ).

. This assumption guarantees the integrability of X and Y (see, for instance, Proposition A3.8 in [23] ).

Let  be a CLBSRM with a family of admissible spectra

be a CLBSRM with a family of admissible spectra . Here we assume that

. Here we assume that

(3.2)

(3.2)

for each . Then, Lemma A.23 in [12] implies that

. Then, Lemma A.23 in [12] implies that

for each . This immediately implies that

. This immediately implies that . Furthermore, by (17.9b) and Proposition 17.2 in [2] , we see that

. Furthermore, by (17.9b) and Proposition 17.2 in [2] , we see that

(3.3)

(3.3)

where  is given by (1.3) if

is given by (1.3) if  is continuously differentiable in h. Note that inequality (3.3) holds for each

is continuously differentiable in h. Note that inequality (3.3) holds for each  whenever

whenever  is coherent.

is coherent.

Our main purpose in this section is to investigate in detail the asymptotic behavior of , as well as

, as well as  if it is defined, as

if it is defined, as . To clearly state our main results, we establish the following conditions, which are assumed to hold in Section 4 of [1] .

. To clearly state our main results, we establish the following conditions, which are assumed to hold in Section 4 of [1] .

[C1] X and Y are independent.

[C2] There is some  such that

such that  has a positive, non-increasing

has a positive, non-increasing

density function  on

on ; that is,

; that is, .

.

[C3] The function  converges to some real number k as

converges to some real number k as .

.

Let us adopt the notation

(3.4)

(3.4)

for . Note that

. Note that  is finite for each fixed

is finite for each fixed  (see Corollary 1 in Appendix 2). Our main results are the two following theorems.

(see Corollary 1 in Appendix 2). Our main results are the two following theorems.

Theorem 1 Assuming [C1]-[C3],  as

as .

.

Formally, assertions (i)-(iii) of Theorem 4.1 in [1] are the same as the assumptions of Theorem 1, by setting . That is, we have

. That is, we have  as

as , where

, where

(3.5)

(3.5)

Theorem 1 justifies the following relation:

Note that condition [C3] is not required for Theorem 1 when . Moreover, when

. Moreover, when , Theorem 1 implies that

, Theorem 1 implies that  converges to

converges to  as

as . The limit

. The limit  does not depend on the forms of

does not depend on the forms of , so this result is robust. The second main result is as follows.

, so this result is robust. The second main result is as follows.

Theorem 2 Assume [C1] and [C3]. Moreover, assume that

[C4] X and Y have positive, continuous, and ultimately decreasing density functions  and

and , respectively, on

, respectively, on .

.

Under these assumptions,  as

as , where

, where  is a positive constant given by

is a positive constant given by

(3.6)

(3.6)

Theorems 1 and 2 together imply that if X and Y are independent, and if  and

and  have adequate density functions, then

have adequate density functions, then

(3.7)

(3.7)

Note that  is always smaller than or equal to 1, so that (3.7) is consistent with inequality (3.3). In particular, if

is always smaller than or equal to 1, so that (3.7) is consistent with inequality (3.3). In particular, if , then the asymptotic equivalence between the marginal risk contribution

, then the asymptotic equivalence between the marginal risk contribution  and the Euler contribution

and the Euler contribution  is justified (see (17.10) in [2] for the definition of marginal risk contributions).

is justified (see (17.10) in [2] for the definition of marginal risk contributions).

Note that  is always larger than or equal to

is always larger than or equal to  so long as the random vector

so long as the random vector  satisfies a suitable technical condition, such as Assumption (S) in [24] . (Here, we modify some conditions of the original version of Assumption (S) to facilitate focusing on non-negative random variables.) Indeed, because

satisfies a suitable technical condition, such as Assumption (S) in [24] . (Here, we modify some conditions of the original version of Assumption (S) to facilitate focusing on non-negative random variables.) Indeed, because  is a convex risk measure, the function

is a convex risk measure, the function  is convex. Thus, we get

is convex. Thus, we get

(3.8)

(3.8)

where the last equality in the above relation is obtained from (5.12) in [24] ,

(3.9)

(3.9)

and

due to the dominated convergence theorem. Therefore, if , then

, then

In Section 4, we numerically verify the above relation. Note that we can also verify a version of Assumption (S) under [C4].

Remark 2

1) If  is continuous, then

is continuous, then  has a uniform distribution on

has a uniform distribution on  (see, for instance, Lemma A.21 in [12] ). Therefore,

(see, for instance, Lemma A.21 in [12] ). Therefore,  with

with  is rewritten as

is rewritten as

where  denotes the expectation operator with respect to the probability measure

denotes the expectation operator with respect to the probability measure  defined as

defined as

(3.10)

(3.10)

Note that we have , and so

, and so  represents the risk scenario that attains the maximum in the following robust representation of

represents the risk scenario that attains the maximum in the following robust representation of :

:

where  is a set of probability measures on

is a set of probability measures on . Also note that if

. Also note that if , then

, then  is given by

is given by

and therefore

Until the end of Remark 2, we assume that  and

and  are continuous.

are continuous.

2) We can relax the independence condition [C1] so that X may weakly depend on Y within the negligible joint tail condition (see Remark A.1 in [1] ). In this case, under some additional assumptions such as [A5] and [A6] in [1] , we can make the same assertion as in Theorem 1, where the value  in the definition (3.4) of

in the definition (3.4) of  is replaced by

is replaced by . In particular, if

. In particular, if , then

, then

(3.11)

(3.11)

Indeed, our proof in Appendix 2 also works by applying Theorem A.1 in [1] instead of Theorem 4.1. Note that we need some additional condition to have that

(3.12)

(3.12)

(see Proposition 3 in Appendix 2).

3) As mentioned in Appendix A.1 of [1] , we can get another version of Theorem A.1 by switching the roles of  and X and by imposing modified (though somewhat artificial) mathematical conditions such as [A5’] and [A6’] in [1] . In particular, if

and X and by imposing modified (though somewhat artificial) mathematical conditions such as [A5’] and [A6’] in [1] . In particular, if , we see that

, we see that

(3.13)

(3.13)

and then (by the same proof as Theorem 1 with (3.13))

(.14)

(.14)

under some assumptions. Here,  is a probability measure defined by (3.10) with replacing X by

is a probability measure defined by (3.10) with replacing X by . If X and Y are independent (with natural assumptions on the density functions), then (3.7) implies that (3.14) is also true. Here, note that the last equality of (3.14) is obtained by (1.3), (3.9), and the dominated convergence theorem. Indeed, we have

. If X and Y are independent (with natural assumptions on the density functions), then (3.7) implies that (3.14) is also true. Here, note that the last equality of (3.14) is obtained by (1.3), (3.9), and the dominated convergence theorem. Indeed, we have

(3.15)

(3.15)

because  is uniformly distributed on

is uniformly distributed on . In Appendix 1, we will show that under some technical conditions that are more natural than both [A5]-[A6] and [A5’]-[A6’] in [1] , relations (3.11) and (3.14) simultaneously hold in the case

. In Appendix 1, we will show that under some technical conditions that are more natural than both [A5]-[A6] and [A5’]-[A6’] in [1] , relations (3.11) and (3.14) simultaneously hold in the case , even if X and Y are dependent.

, even if X and Y are dependent.

Note that if , then

, then

which is known as the component CVaR (also known as the CVaR contribution) and widely used, particularly in the practice of credit portfolio risk management (see for instance [25] [26] , and [27] ).

4. Numerical Analysis

In this section, we numerically investigate the behavior of . Throughout this section, we assume that the distributions of X and Y are given as

. Throughout this section, we assume that the distributions of X and Y are given as  and

and , respectively, with

, respectively, with  and

and , where

, where  denotes the generalized Pareto distribution whose distribution function is given by

denotes the generalized Pareto distribution whose distribution function is given by ,

, . Then,

. Then,  and

and  satisfy (3.1) with

satisfy (3.1) with  and

and . Note that condition [C3] is satisfied with

. Note that condition [C3] is satisfied with

(see (5.2) in [1] ). Also note that  and

and  are analytically solved as

are analytically solved as

We numerically compute , and

, and , where we let

, where we let  for brevity. In all calculations, we fix

for brevity. In all calculations, we fix  and

and . For

. For  and

and , we examine several patterns to study each of the following three cases: 1)

, we examine several patterns to study each of the following three cases: 1) , 2)

, 2) , and 3)

, and 3) .

.

Case 1)

We set  and

and . Hence,

. Hence,  and

and , so that

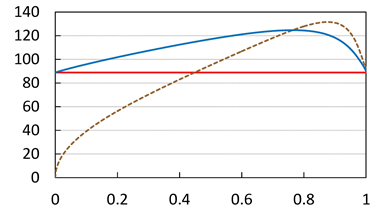

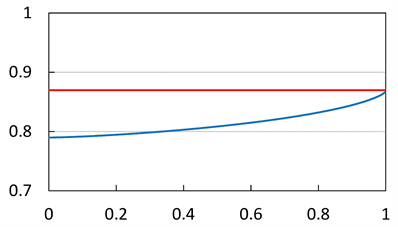

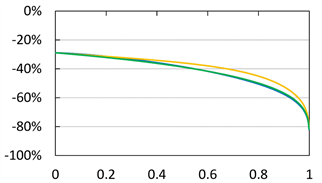

, so that  holds. Figure 1 shows the graphs of

holds. Figure 1 shows the graphs of , and

, and . These values are always larger than

. These values are always larger than  whenever

whenever , and they converge to

, and they converge to  for both

for both  and

and . Indeed,

. Indeed,

(4.1)

(4.1)

holds because ,

,  for each

for each . The limit as

. The limit as  is a consequence of Theorem 1. Moreover, the forms of these graphs are unimodal. That is, the function

is a consequence of Theorem 1. Moreover, the forms of these graphs are unimodal. That is, the function  increases on

increases on  and decreases on

and decreases on  for some

for some . Intuitively, the values of

. Intuitively, the values of  seem to become large as a increases because a larger a implies a greater risk sensitivity. However, our result implies that the impact of adding loss variable Y into the prior risk profile X is maximized at some

seem to become large as a increases because a larger a implies a greater risk sensitivity. However, our result implies that the impact of adding loss variable Y into the prior risk profile X is maximized at some .

.

Figure 2 shows the relation between  and

and . We see that

. We see that  takes a maximum at

takes a maximum at , where

, where  is a solution to

is a solution to

(4.2)

(4.2)

Indeed, we have the following result.

Proposition 1 If there is a unique solution  to (4.2), then

to (4.2), then

.

.

Note that unlike the case of SRMs,  takes a value smaller than

takes a value smaller than  if a is small. This is because VaR is not a convex risk measure, so the relation (3.8) is not guaranteed for

if a is small. This is because VaR is not a convex risk measure, so the relation (3.8) is not guaranteed for . In particular, we observe that

. In particular, we observe that

Figure 1. Graphs of  (blue),

(blue),  (orange),

(orange),  (green) and

(green) and  (black, dashed) with

(black, dashed) with  and

and . The red solid line shows

. The red solid line shows . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 2. Graphs of  (blue) and

(blue) and  (brown, dashed) with

(brown, dashed) with  and

and . The red solid line shows

. The red solid line shows . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

(4.3)

(4.3)

Case 2)

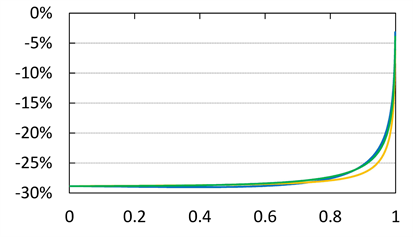

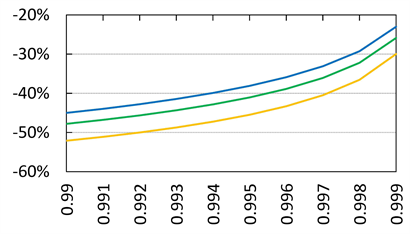

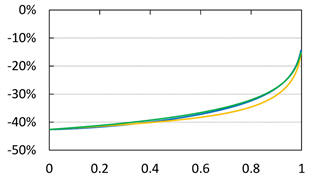

Figure 3 shows the approximation errors, defined as

(4.4)

(4.4)

with  (

( ) and

) and  (

( ). We see that

). We see that  is close to 0 as

is close to 0 as  for each case of

for each case of . Moreover, we numerically verify the assertion of Theorem 2 for

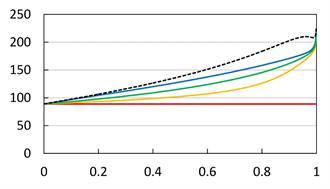

. Moreover, we numerically verify the assertion of Theorem 2 for  in Figure 4. We observe that

in Figure 4. We observe that  converges to

converges to  as

as .

.

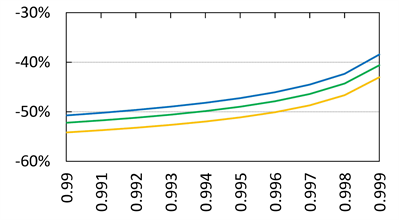

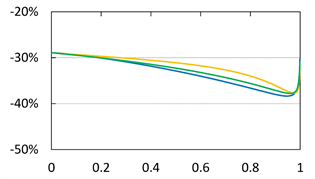

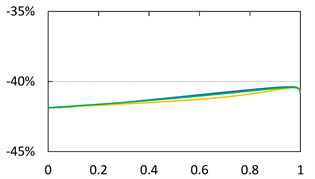

By contrast, the convergence speed of  as

as  decreases if the tails of X and Y are less fat-tailed. Figure 5 shows

decreases if the tails of X and Y are less fat-tailed. Figure 5 shows  with

with  (

( ) and

) and  (

( ). We find that

). We find that  decreases as a tends to 1, but the gap between

decreases as a tends to 1, but the gap between  and 0 is still large, even in the case

and 0 is still large, even in the case .

.

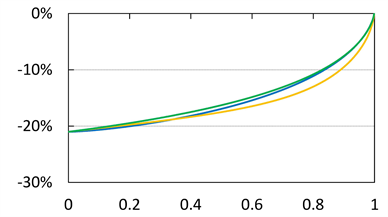

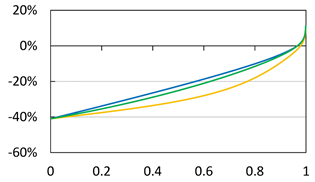

Case 3)

Finally, we look at the case . The results are summarized in Figure 6 and Figure 7. We see that

. The results are summarized in Figure 6 and Figure 7. We see that  approaches 0 as

approaches 0 as  for each case of

for each case of . We also confirm that

. We also confirm that  converges to

converges to  as

as .

.

Similarly to Case 2), the convergence speed of  decreases as the tails of X and Y become thinner. Figure 8 shows the graph of

decreases as the tails of X and Y become thinner. Figure 8 shows the graph of  with

with . The approximation error tends to zero as

. The approximation error tends to zero as , but remains smaller than −20% even when

, but remains smaller than −20% even when .

.

5. Concluding Remarks

In this paper, we have studied the asymptotic behavior of the difference between  and

and  as

as  when

when  is a parameterized SRM satisfying (1.2). We have shown that

is a parameterized SRM satisfying (1.2). We have shown that  is asymptotically equivalent to

is asymptotically equivalent to  given by (3.4), whose form changes according to the relative magnitudes

given by (3.4), whose form changes according to the relative magnitudes

Figure 3. Approximation errors defined by (4.4) with  and

and . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 4.  (blue) and

(blue) and  (red). We set

(red). We set  and

and . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 5. Approximation errors defined by (4.4) with  and

and . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 6. Approximation errors defined by (4.4) with . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 7.  (blue) and

(blue) and  (red). We set

(red). We set . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

Figure 8. Approximation errors defined by (4.4) with . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a.

. The horizontal axis corresponds to a.

of the thicknesses of the tails of X and Y. In particular, for , we found the convergence

, we found the convergence  for general CLBSRMs

for general CLBSRMs . Moreover, we also found that

. Moreover, we also found that  as

as  for a constant

for a constant  given by (3.6). This clarifies the asymptotic relation between the marginal risk contribution and the Euler contribution.

given by (3.6). This clarifies the asymptotic relation between the marginal risk contribution and the Euler contribution.

Our numerical results in the case  showed that

showed that  is not increasing but is unimodal with respect to a, which implies that the impact of Y in the portfolio

is not increasing but is unimodal with respect to a, which implies that the impact of Y in the portfolio  does not always increase with a. Interestingly, this phenomenon is inconsistent with intuition.

does not always increase with a. Interestingly, this phenomenon is inconsistent with intuition.

Our results essentially depend on the assumption that X and Y are independent. However, the dependence structure of the loss variables X and Y plays an essential role in financial risk management. The case of dependent X and Y for  has already been studied in Section A.1 of [1] . As mentioned in Remark 2, we have now generalized this result to the case of CLBSRMs. However, we require the somewhat strong assumption that X and Y are not strongly dependent on each other. With the additional analysis in Appendix 1, we will see that our main results still hold for a general dependence structure if

has already been studied in Section A.1 of [1] . As mentioned in Remark 2, we have now generalized this result to the case of CLBSRMs. However, we require the somewhat strong assumption that X and Y are not strongly dependent on each other. With the additional analysis in Appendix 1, we will see that our main results still hold for a general dependence structure if , but that they are easily violated if

, but that they are easily violated if . In future work, we will continue to study the asymptotic behavior of

. In future work, we will continue to study the asymptotic behavior of  as

as , without the independence condition.

, without the independence condition.

Cite this paper

Kato, T. (2018) Asymptotic Analysis for Spectral Risk Measures Parameterized by Confidence Level. Journal of Mathematical Finance, 8, 197-226. https://doi.org/10.4236/jmf.2018.81015

References

- 1. Kato, T. (2017) Theoretical Sensitivity Analysis for Quantitative Operational Risk Management. International Journal of Theoretical and Applied Finance, 20, 23 p. https://doi.org/10.1007/PL00011399

- 2. Tasche, D. (2008) Capital Allocation to Business Units and Sub-Portfolios: The Euler Principle. In: Resti, A., Ed., Pillar II in the New Basel Accord: The Challenge of Economic Capital, Risk Books, London, 423-453.

- 3. Acerbi, C. (2002) Spectral Measures of Risk: A Coherent Representation of Subjective Risk Aversion. Journal of Banking & Finance, 26, 1505-1518. https://doi.org/10.1016/S0378-4266(02)00281-9

- 4. Acerbi, C. and Tasche, D. (2002) Expected Shortfall: A Natural Coherent Alternative to Value at Risk. Economic Notes, 31, 379-388. https://doi.org/10.1111/1468-0300.00091

- 5. Embrechts, P. (2000) Extreme Value Theory: Potential and Limitations as an Integrated Risk Management Tool, Derivatives Use. Trading & Regulation, 6, 449-456.

- 6. Tasche, D. (2002) Expected Shortfall and Beyond. Journal of Banking & Finance, 26, 1519-1533. https://doi.org/10.1016/S0378-4266(02)00272-8

- 7. Acerbi, C., Nordio, C. and Sirtori, C. (2001) Expected Shortfall as a Tool for Financial Risk Management. Preprint. https://arxiv.org/pdf/cond-mat/0102304.pdf

- 8. Acerbi, C. and Tasche, D. (2002) On the Coherence of Expected Shortfall. Journal of Banking & Finance, 26, 1487-1503. https://doi.org/10.1016/S0378-4266(02)00283-2

- 9. Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999) Coherent Measures of Risk. Mathematical Finance, 9, 203-228. https://doi.org/10.1111/1467-9965.00068

- 10. Basel Committee on Banking Supervision (2012) Fundamental Review of the Trading Book. Press Release, Bank for International Settlements. http://www.bis.org/publ/bcbs219.pdf

- 11. Basel Committee on Banking Supervision (2016) Minimum Capital Requirements for Market Risk. Press Release, Bank for International Settlements. http://www.bis.org/bcbs/publ/d352.pdf

- 12. Föllmer, H. and Schied, A. (2016) Stochastic Finance: An Introduction in Discrete Time. 4th Edition, De Gruyter. https://doi.org/10.1515/9783110463453

- 13. Jouini, E., Schachermayer, W. and Touzi, N. (2006) Law Invariant Risk Measures Have the Fatou Property, In: Kusuoka, S. and Yamazaki, A., Eds., Advances in Mathematical Economics, 9, 49-71, Springer, Japan. https://doi.org/10.1007/4-431-34342-3_4

- 14. Kusuoka, S. (2001) On Law-Invariant Coherent Risk Measures. In: Kusuoka, S. and Maruyama, T., Eds., Advances in Mathematical Economics, 3, 83-95, Springer, Japan. https://doi.org/10.1007/978-4-431-67891-5_4

- 15. Shapiro, S. (2013) On Kusuoka Representation of Law Invariant Risk Measures. Mathematics of Operations Research, 38, 142-152. https://doi.org/10.1287/moor.1120.0563

- 16. Pflug, G.Ch. and Römisch, W. (2007) Modeling, Measuring and Managing Risk. World Scientific Publishing Co., London. https://doi.org/10.1142/6478

- 17. Cotter, J. and Dowd, K. (2006) Extreme Spectral Risk Measures: An Application to Futures Clearinghouse Margin Requirements. Journal of Banking & Finance, 30, 3469-3485. https://doi.org/10.1016/j.jbankfin.2006.01.008

- 18. Brandtner, M. and Kürsten, W. (2017) Consistent Modeling of Risk Averse Behavior with Spectral Risk Measures: Wächter/Mazzoni Revisited. European Journal of Operational Research, 259, 394-399. https://doi.org/10.1016/j.jbankfin.2006.01.008

- 19. Sriboonchitta, S., Nguyen, H.T. and Kreinovich, V. (2010) How to Relate Spectral Risk Measures and Utilities. International Journal of Intelligent Technologies and Applied Statistics, 3, 141-158. https://doi.org/10.6148/IJITAS.2010.0302.03

- 20. Wächter, H.P. and Mazzoni, T. (2013) Consistent Modeling of Risk Averse Behavior with Spectral Risk Measures. European Journal of Operational Research, 229, 487-495. https://doi.org/10.1016/j.ejor.2013.03.001

- 21. Dowd, K., Cotter, J. and Sorwar, G. (2008) Spectral Risk Measures: Properties and Limitations. Journal of Financial Services Research, 34, 61-75. https://doi.org/10.1007/s10693-008-0035-6

- 22. Bingham, N.H., Goldie, C.M. and Teugels, J.L. (1989) Regular Variation. Cambridge University Press, Cambridge.

- 23. Embrechts, P., Klüppelberg, C. and Mikosch, T. (1997) Modelling Extremal Events, Springer, Berlin. https://doi.org/10.1007/978-3-642-33483-2

- 24. Tasche, D. (2000) Risk Contributions and Performance Measurement, Working Paper. https://pdfs.semanticscholar.org/2659/60513755b26ada0b4fb688460e8334a409dd.pdf

- 25. Andersson, F., Mausser, H., Rosen, D. and Uryasev, S. (2001) Credit Risk Optimization with Conditional Value-at-Risk Criterion. Mathematical Programming Series B, 89, 273-291. https://doi.org/10.1007/PL00011399

- 26. Kalkbrener, M., Kennedy, A. and Popp, M. (2007) Efficient Calculation of Expected Shortfall Contributions in Large Credit Portfolios. Journal of Computational Finance, 11, 1-43. https://doi.org/10.21314/JCF.2007.162

- 27. Puzanova, N. and Düllmann, K. (2013) Systemic Risk Contributions: A Credit Portfolio Approach. Journal of Banking & Finance, 37, 1243-1257. https://doi.org/10.1016/j.jbankfin.2012.11.017

- 28. McNeil, A.J., Frey, R. and Embrechts, P. (2005) Quantitative Risk Management. Princeton University Press, Princeton.

- 29. Bingham, N.H., Goldie, C.M. and Omey, E. (2006) Regularly Varying Probability Densities, Publications de l’Institut Mathematique, 80, 47-57. https://doi.org/10.2298/PIM0694047B

Appendix 1. A Short Consideration of the Dependent Case

Here, we briefly investigate the asymptotic behavior of  as

as  when X and Y are not independent. Throughout this section, we assume that

when X and Y are not independent. Throughout this section, we assume that ,

,  , and

, and  are continuous. With this, (3.8) is rewritten as

are continuous. With this, (3.8) is rewritten as . Combining this result with (3.3), we have

. Combining this result with (3.3), we have

(A.1)

(A.1)

Note that (A.1) holds for general SRM  whenever (3.9) holds.

whenever (3.9) holds.

1.1. Comonotonic Case

We consider the case where X and Y are comonotone. In other words, they are perfectly positively dependent (see Definition 4.82 of [12] and Definition 5.15 in [28] ). In this case, the following proposition is straightforwardly shown.

Proposition 2 If X and Y are comonotone, then

(A.2)

(A.2)

This proposition implies that when , the asymptotic relations (3.11) and (3.14) still hold, even if X and Y are strongly correlated, but that the assertions of Theorems 1 and 2 do not necessarily hold when

, the asymptotic relations (3.11) and (3.14) still hold, even if X and Y are strongly correlated, but that the assertions of Theorems 1 and 2 do not necessarily hold when .

.

1.2. Additional Numerical Analysis

Similarly to Section 4, we assume that  and

and  with

with ,

, . To describe the dependence between X and Y, we introduce a copula. By Sklar’s theorem, we see that the joint distribution function

. To describe the dependence between X and Y, we introduce a copula. By Sklar’s theorem, we see that the joint distribution function  of the random vector

of the random vector  is represented by

is represented by

for a copula , which is a distribution function with uniform marginals. Here, we examine the following three copulas:

, which is a distribution function with uniform marginals. Here, we examine the following three copulas:

1) The Gaussian copula ,

,  ,

,

2) The Gumbel copula ,

,  ,

,

3) The countermonotonic copula ,

,

where  is the distribution function of the standard

is the distribution function of the standard

normal distribution (for more details on the copulas, see, for instance, Chapter 5 of [28] ). The parameters  in (a) and

in (a) and  in (b) describe the strength of the dependence between X and Y. We always set

in (b) describe the strength of the dependence between X and Y. We always set  and

and  in this section. If

in this section. If , then X and Y are perfectly negatively dependent. In particular, in that case, X and Y are represented as

, then X and Y are perfectly negatively dependent. In particular, in that case, X and Y are represented as  and

and , where U is a random variable with uniform distribution on

, where U is a random variable with uniform distribution on .

.

Figure A1 summarizes the results with  and

and . We compare the values of

. We compare the values of  (with

(with ) and

) and . We find that all these values converge to the same value, which is not equal to

. We find that all these values converge to the same value, which is not equal to , by letting

, by letting . Note that when X and Y are countermonotonic, they converge to zero as

. Note that when X and Y are countermonotonic, they converge to zero as , so (3.12) does not hold in this case.

, so (3.12) does not hold in this case.

Figure A2 shows the graphs of the relative errors defined by (4.4) with  when we set

when we set  and

and . We find that

. We find that  does not converge to zero as

does not converge to zero as . Similar phenomena are observed in Figure A3 with the settings

. Similar phenomena are observed in Figure A3 with the settings . Therefore, the assertion of Theorem 1 does not hold when

. Therefore, the assertion of Theorem 1 does not hold when  if X and Y are correlated.

if X and Y are correlated.

Figure A1. Graphs of  (blue),

(blue),  (orange),

(orange),  (green) and

(green) and  (black, dashed) with

(black, dashed) with  and

and . The red solid line shows

. The red solid line shows . The horizontal axis corresponds to a. Top:

. The horizontal axis corresponds to a. Top:  with

with . Center:

. Center:  with

with . Bottom:

. Bottom: .

.

Figure A2. Approximation errors defined by (4.4) with  and

and . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a. Top:

. The horizontal axis corresponds to a. Top:  with

with . Center:

. Center:  with

with . Bottom:

. Bottom: .

.

Note that the above findings are consistent with the comonotonic case (Proposition 2).

1.3. Theoretical Result in the Case

We describe the following conditions.

[C5] For each ,

,  has a positive, non-increasing density function

has a positive, non-increasing density function  on

on , where

, where  is the conditional distribution function of X given

is the conditional distribution function of X given . Moreover,

. Moreover,  is continuous in

is continuous in  and y.

and y.

[C6] There is a  such that

such that  is uniformly regularly varying with index

is uniformly regularly varying with index  in the following sense:

in the following sense:

Figure A3. Approximation errors defined by (4.4) with . Blue line:

. Blue line: . Orange line:

. Orange line: . Green line:

. Green line: . The horizontal axis corresponds to a. Top:

. The horizontal axis corresponds to a. Top:  with

with . Center:

. Center:  with

with . Bottom:

. Bottom: .

.

(A.3)

(A.3)

for each . Moreover,

. Moreover,  is ultimately decreasing.

is ultimately decreasing.

[C7] It holds that

(A.4)

(A.4)

for some .

.

Conditions [C5]-[C7] strongly correspond to conditions [A5]-[A6] in [1] . It should be noted that the index parameter  is assumed to be equal to

is assumed to be equal to  in condition [A6] in [1] , but that this equality is not required to obtain our results. Note also that

in condition [A6] in [1] , but that this equality is not required to obtain our results. Note also that  may be different from

may be different from . Indeed, we can verify, at least numerically, that for each

. Indeed, we can verify, at least numerically, that for each , the function

, the function  is regularly varying with index

is regularly varying with index  (resp.,

(resp., ) if we adopt

) if we adopt  (resp.,

(resp., ) as a copula for the random vector

) as a copula for the random vector  whose marginal distributions are given by the generalized Pareto distribution.

whose marginal distributions are given by the generalized Pareto distribution.

Using a similar argument as in the proof of the uniform convergence theorem (Theorem 1.2.1 in [22] ), together with the continuity of  in y, we get from (A.3) that

in y, we get from (A.3) that

(A.5)

(A.5)

for each compact set .

.

We now introduce the following result.

Theorem 3 Assume [C5]-[C7] and (3.12). If , it holds that

, it holds that

This theorem claims that both (3.11) and (3.14) are true under some conditions, even when X and Y are dependent.

Appendix 2. Proofs

\Proof of Lemma 1. Assume (2.5). Fix any . Then, (2.5) implies that

. Then, (2.5) implies that

(B.1)

(B.1)

Because  is non-decreasing and non-negative, we see that

is non-decreasing and non-negative, we see that

(B.2)

(B.2)

Combining (B.1) with (B.2), we have .

.

Conversely, if we assume (2.6), then Prokhorov’s theorem implies that for

each increasing sequence  with

with  there is a further subsequence

there is a further subsequence  and a probability measure

and a probability measure  on

on  such that

such that

weakly converges to  as

as . Then, for each

. Then, for each , we see that

, we see that

This immediately leads us to , hence

, hence . We therefore arrive at (2.5).

. We therefore arrive at (2.5).

Proof of Proposition 1. Let . We observe that

. We observe that

where . By (4.1), (4.3), and Theorem 1, we see that g is continuous on

. By (4.1), (4.3), and Theorem 1, we see that g is continuous on ,

,  and

and . Moreover, by the assumption, it holds that

. Moreover, by the assumption, it holds that  and

and  for all

for all . Together, these imply that g is positive on

. Together, these imply that g is positive on  and negative on

and negative on , and that

, and that  has the same pattern. Therefore,

has the same pattern. Therefore,  takes a maximum at

takes a maximum at .

.

Proof of Proposition 2. Because  is comonotonic, we obviously have

is comonotonic, we obviously have

Here, we see that  and

and  for some random variable U with uniform distribution on

for some random variable U with uniform distribution on  (see Lemmas 4.89-4.90 in [12] and their proofs). Then we have

(see Lemmas 4.89-4.90 in [12] and their proofs). Then we have

and thus

Similarly, because , we have

, we have

and , which completes the proof.

, which completes the proof.

2.1. Proof of Theorem 1

We first state some propositions and prove them. For this, let  be given as (3.5). Note again that

be given as (3.5). Note again that  defined in (3.4) satisfies

defined in (3.4) satisfies

Proposition 3 .

.

Proof. If , we see that

, we see that  because Y is non-negative and

because Y is non-negative and  is positive. If

is positive. If , we observe

, we observe

where  is a real number satisfying

is a real number satisfying . The existence of such an

. The existence of such an  can be proven using Propositions 1.5.1 and 1.5.15 in [22] . Similarly, if

can be proven using Propositions 1.5.1 and 1.5.15 in [22] . Similarly, if , we have

, we have

Proposition 4 .

.

Proof. If , the assertion is obvious from the assumption

, the assertion is obvious from the assumption . If

. If , we see that

, we see that

because of . If

. If , we have

, we have

Corollary 1 ,

, .

.

Proof. This follows from (3.2) and Proposition 4.

Proof of Theorem 1. Let ,

, . Note that

. Note that

(B.3)

(B.3)

by virtue of Theorem 4.1(i)-(iii) in [1] . Moreover, (B.3) immediately implies

(B.4)

(B.4)

Furthermore, it holds that

(B.5)

(B.5)

hence  is integrable. The integrability of

is integrable. The integrability of  is guaranteed by Proposition 4.

is guaranteed by Proposition 4.

Temporarily fix any . From (2.6) and (B.5), we easily see that

. From (2.6) and (B.5), we easily see that

(B.6)

(B.6)

Similarly, we have

(B.7)

(B.7)

Additionally, we have

(B.8)

(B.8)

where . Using (B.7) and Proposition 3, we obtain

. Using (B.7) and Proposition 3, we obtain

(B.9)

(B.9)

By (B.8) and (B.9), we have

Combining this with (B.6) and Proposition 3, we arrive at

Because  is arbitrary, we obtain the desired assertion by (B.4).

is arbitrary, we obtain the desired assertion by (B.4).

2.2. Proof of Theorem 2

Let  for brevity. We see that Z has a density function

for brevity. We see that Z has a density function

Lemma 2  is positive and continuous on

is positive and continuous on . Moreover,

. Moreover,  is regularly varying with index

is regularly varying with index  and it holds that

and it holds that

(B.10)

(B.10)

Proof. Continuity and positivity are obvious. By [C4] and Theorem 1.1 in [29] , we see that ,

,  and that

and that  is regularly varying with index

is regularly varying with index . The last assertion is obtained by Proposition 1.5.10 in [22] .

. The last assertion is obtained by Proposition 1.5.10 in [22] .

Let  be the conditional distribution function of Y given

be the conditional distribution function of Y given . Then we have

. Then we have

(B.11)

(B.11)

Proposition 5 It holds that

Proof. For each , a straightforward calculation gives

, a straightforward calculation gives

which implies our assertion.

Note that (B.11) and Proposition 5 lead to

(B.12)

(B.12)

Proposition 6 If , then

, then

Proof. Let

(B.13)

(B.13)

(B.14)

(B.14)

(B.15)

(B.15)

Then, we see that

(B.16)

(B.16)

Therefore, we need to show that

(B.17)

(B.17)

First, we show that

(B.18)

(B.18)

Using (B.10), Lemmas A.1 and A.3 in [1] , and Proposition A3.8 in [23] , we obtain

Furthermore, we observe that

(B.19)

(B.19)

and that the function  is regulary varying with index

is regulary varying with index . Thus, we obtain

. Thus, we obtain

Now, (B.18) is obvious.

Next, we observe that

Because  and

and  are convergent (as

are convergent (as ), they are bounded. Thus, we have

), they are bounded. Thus, we have

(B.20)

(B.20)

for some . By (B.18) and (B.20), we can apply the dominated convergence theorem to obtain (B.17).

. By (B.18) and (B.20), we can apply the dominated convergence theorem to obtain (B.17).

Proposition 7 If , then

, then

Proof. Let ,

,  , and

, and  be the same as in (B.13)-(B.15). First, we have

be the same as in (B.13)-(B.15). First, we have ,

,  by the same argument as in the proof of Proposition 6. Next, for each

by the same argument as in the proof of Proposition 6. Next, for each , we see that

, we see that

due to [C3], (B.10), Proposition A3.8 in [23] , Proposition 3.1(i) in [1] , and Lemmas A.1 and A.3 in [1] . Moreover, we have (B.19), and the right-hand side of this inequality converges to  as

as , and so it is bounded. Therefore, we apply the dominated convergence theorem to obtain

, and so it is bounded. Therefore, we apply the dominated convergence theorem to obtain  as

as . We complete the proof by combining these with (B.16).

. We complete the proof by combining these with (B.16).

Proposition 8 If , we have

, we have

Proof. Let ,

,  and

and  be set as earlier. Similarly to the proof of Propositions 6 and 7, we get

be set as earlier. Similarly to the proof of Propositions 6 and 7, we get ,

, . This implies that

. This implies that ,

,  , where

, where . Therefore, it suffices to show that

. Therefore, it suffices to show that  as

as , which is easy to see by using similar calculations as in the proof of Proposition 7 and by using Proposition 3.1(i) in [1] .

, which is easy to see by using similar calculations as in the proof of Proposition 7 and by using Proposition 3.1(i) in [1] .

Proposition 9 If , then

, then

Proof. Similarly to the proof of Proposition 8, we need to show only that

(B.21)

(B.21)

where . Note that Lemmas A.1 and A.2 in [1] imply

. Note that Lemmas A.1 and A.2 in [1] imply ,

,  and

and ,

, . Therefore, for each

. Therefore, for each , we observe

, we observe

by [C3], (B.10), Proposition A3.8 in [23] , and Lemma A.3 in [1] . Moreover, we have

and thus we obtain (B.21) by applying the dominated convergence theorem.

Proof of Theorem 2. We can verify that the random vector  satisfies (a version of) Assumption (S) in [24] by using a standard argument. Therefore, (3.9) is true from (5.13) in [24] . Additionally, using Propositions 6-9, we see that for each

satisfies (a version of) Assumption (S) in [24] by using a standard argument. Therefore, (3.9) is true from (5.13) in [24] . Additionally, using Propositions 6-9, we see that for each , there is an

, there is an  such that

such that

(B.22)

(B.22)

where we denote . Moreover, it is easy to see that

. Moreover, it is easy to see that  and

and  are bounded on

are bounded on . Therefore, combining (3.9), (3.15), and (B.22), we get

. Therefore, combining (3.9), (3.15), and (B.22), we get

where , which is positive due to Proposition 3. Because

, which is positive due to Proposition 3. Because

is arbitrary, we obtain the desired assertion.

is arbitrary, we obtain the desired assertion.

2.3. Proof of Theorem 3

First, note that condition [C5] immediately implies [C2] with  and

and

Second, note that by [C6], Proposition 3.1(i) in [1] (see also Remark 3.2 therein) and Proposition A3.8 in [23] , we have (B.10) and

(B.23)

(B.23)

To prove Theorem 3, we give the following three propositions.

Proposition 10  is continuously differentiable in

is continuously differentiable in  and it holds that

and it holds that

Proposition 10 is obtained by an argument similar to the proof of Lemma 5.3 in [24] , using the implicit function theorem.

Proposition 11 The function  is regularly varying with index

is regularly varying with index .

.

Proof. Fix any . We observe that

. We observe that

and therefore, using [C5], we arrive at

Proposition 12 .

.

Proof. Fix any . Then we have

. Then we have

where we denote  and

and

By [C7] and the Chebyshev inequality, we get

(B.24)

(B.24)

for some . Because Proposition 11 tells us that

. Because Proposition 11 tells us that  is regularly varying with index

is regularly varying with index , the right-hand side of (B.24) converges to zero as

, the right-hand side of (B.24) converges to zero as  (see Proposition 1.5.1 in [22] ).

(see Proposition 1.5.1 in [22] ).

Moreover, we see that

Here, we observe that

for each . Note that if

. Note that if  (resp.,

(resp., ), we have

), we have  (resp.,

(resp., ). Moreover, by (B.23),

). Moreover, by (B.23),  converges to 1 as

converges to 1 as , and so it is bounded. Therefore, we get

, and so it is bounded. Therefore, we get

for some .

.

Now we arrive at

by using (A.5) and (B.23). Because  is arbitrary, we obtain the desired assertion.

is arbitrary, we obtain the desired assertion.

Proof of Theorem 3. First, note that Proposition 10 guarantees that

where  and

and .

.

Then, fix any . By Propositions 11-12 and Lemma A.3 in [1] , we see that

. By Propositions 11-12 and Lemma A.3 in [1] , we see that

Thus, there is an  such that

such that

Therefore, we have

by virtue of (3.12). Because  is arbitrary, we get that

is arbitrary, we get that ,

, . Combining this result with (A.1), we obtain the desired assertion.

. Combining this result with (A.1), we obtain the desired assertion.