Theoretical Economics Letters

Vol.05 No.06(2015), Article ID:62339,9 pages

10.4236/tel.2015.56089

Tax Evasion Dynamics via Non-Equilibrium Model on Complex Networks

Francisco W. S. Lima

Dietrich Stauffer Computational Physics Lab, Departamento de Física Universidade Federal do Piauí, Teresina, Brazil

Copyright © 2015 by author and Scientific Research Publishing Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received 17 November 2015; accepted 26 December 2015; published 29 December 2015

ABSTRACT

The Zaklan model has become an excellent mechanism to control the tax evasion fluctuations (TEF) in a people- or agent-based community. Initially, the equilibrium Ising model (IM) had been used as a dynamic of temporal evolution of the Zaklan model near the critical point of the IM. On some complex network the IM presents no critical points or well-defined phase transitions. Then, through Monte Carlo simulations we study the recurring problem of the TEF control using the version of non-equilibrium Zaklan model as a control mechanism for TEF via agent-based non-equilibrium majority-vote model (MVM). Here we study the TEF on directed Barabási-Albert (BAD) and Apollonian (ANs) networks where the IM is not applied. We show that the Zaklan model can be also studied using non-equilibrium dynamics through of the non-equilibrium MVM on complex topologies cited above, giving the behavior of the TEF regardless of dynamic or topology used here.

Keywords:

Opinion Dynamics, Sociophysics, Majority Vote, Non-Equilibrium

1. Introduction

The social and economic behavior of a community of people has been successfully studied using the Ising model close to its critical points [1] -[5] , see also [6] -[9] .

According [10] [12] -[14] , the tax evasion in a community of people remains a major cause of concern for governments. Second [15] , the higher levels of tax evasion generally occur in less developed countries that present a lower amount of trust that people have in governmental institutions. Gächter [16] , Frey and Torgler [17] have provided empirical evidences that indicate that tax payers tend to condition their decision regarding whether to pay taxes or not on the tax evasion decision of the members of their group or neighborhood as also provide experimental evidence on the relevance of conditional cooperation for tax morale. Within the context Zaklan et al. [7] [8] developed an economics model to study the problem of tax evasion dynamics on a people community. However, this model deals with illegal tax evasion only. They used the equilibrium Ising model on a square lattice (SL) and Monte-Carlo simulations with the Glauber algorithms to study the proposed model.

In Germany, the loss in taxes and social security by unreported “informal” work has been claimed to correspond to nearly two percent of the Gross Domestic Product.

Zaklan et al. [8] also have studied the implications of conditional cooperation in a multi-agent-based framework. They considered a large number of agents (people) who interact locally with each other and base their decision whether to evade taxes or not on the behavior of their neighbors. They used the Ising model on a SL to study the behavior of tax evasion and furthermore add a policy maker’s tax enforcement mechanism. In their model the enforcement mechanism consists of two components: a probability (p) of an audit each person is subject to in every period, and a length (k) of time detected tax evaders remain honest.

In this work, we study the behavior of the tax evasion on an agent community of honest citizens and tax evaders, where the agents are positioned on sites of complex networks, but now using a version of non-equilibrium of the Zaklan model proposed by Lima [18] [19] . Here, each agent does have an opinion in the presence of a constant social noise (q) as in the traditional Majority-Vote model (MVM) [20] .

The non-equilibrium model proposed by Lima [18] [19] is based on the knowledge that we do not live in a social equilibrium and any rumor or gossip can lead to a government or market chaos. Then, a non-equilibrium model (MVM) explains better events of non-equilibrium and makes this model more realistic to explain social and economic behavior of a community of people. We ask if also this more realistic model reproduces the main results of the earlier versions and the answer is yes. Other motivation to use Lima model is that this presents a well-defined phase transition on directed Barabási-Albert and Apollonian networks. In these complex networks the equilibrium IM does not present a phase transition making it impossible to use the equilibrium Zaklan model via IM because this has no “social temperature” on these complex networks.

R. Wintrobe and K. Gërxhani [15] argued that less developed countries may have high tax evasion because of less trust in government. Zaklan et al. [7] [8] proposed a model to study this problem , called here the Zaklan model, using Monte Carlo simulations and a equilibrium IM dynamics on square lattices. Their results are in good agreement with analytical and experimental results obtained by [15] . On some topologies like ANs and DBA the IM does not present a phase transittion making this model inappropriate to study TEF. However, the MVM does not present this limitation on these topologies. The source of this distinction is due to the different behavior of noise in each of these models [27] . In the IM, the probability of switching a highly connected spin against the local majority is smaller than a less connected one; since the energy variation is larger for a more connected spin. In the MVM, the probability of a spin switching against the local majority is always given by q, independent on the number of neighbors of this spin. The motivation of this work is to study tax evasion on complex networks via a nonequilibrium dynamics model (MVM) with the objective to make this model as realistic as possible.

2. Complex Networks

Here we briefly describe the complex networks used in this study as previously mentioned.

2.1. Undirected and Directed Apollonian Network

The Apollonian network is composed of  nodes, where n is the generation number and N the node number [21] [22] . On these ANs structures we can introduce a disorder, in such a way that we redirect a fraction

nodes, where n is the generation number and N the node number [21] [22] . On these ANs structures we can introduce a disorder, in such a way that we redirect a fraction  of the links. This redirecting results in a directed network, preserving the outgoing node of the redirected link but changing the incoming node. When

of the links. This redirecting results in a directed network, preserving the outgoing node of the redirected link but changing the incoming node. When  we have the standard AP networks, while for

we have the standard AP networks, while for  we have something similar to random networks [26] . In this procedure of the redirecting links, the number of outgoing links of each node is preserved even when

we have something similar to random networks [26] . In this procedure of the redirecting links, the number of outgoing links of each node is preserved even when  and the networks still have hubs that are the most influent nodes. These networks display a scale-free degree distribution and a hierarchical structure. In the undirected case there exists the reciprocity of redirected links, i.e., if node A selects node B as incoming neighbor then A is also an incoming neighbor of B.

and the networks still have hubs that are the most influent nodes. These networks display a scale-free degree distribution and a hierarchical structure. In the undirected case there exists the reciprocity of redirected links, i.e., if node A selects node B as incoming neighbor then A is also an incoming neighbor of B.

2.2. Undirected Barabási-Albert Network

The undirected Barabási-Albert network [24] [25] is grown such that the probability of a new node to be connected to one of the already existing nodes is proportional to the number of the previous connections to this already existing node: the rich get richer. In this way, each new node selects exactly m old nodes as neighbors. If a new node selects randomly m old nodes as neighbors, then the m old nodes are added to a long array of node indices called the Kertész list, and the new node is also added m times to that list. At the start of the network growth, this Kertész list is empty. The above random selections are made by selecting m random nodes from the Kertész list. The neighbor relations were such that if A has B as a neighbor, B has A as a neighbor.

2.3. Directed Barabási-Albert Network

In directed Barabási-Albert networks, the network itself is produced in the undirected Barabási-Albert networks way [23] . When interacting agents are put onto this network, each node is influenced by the fixed number m of neighbors with it had selected when joining the network. It is not influenced by other nodes that selected it as neighbor after it joined the network, i.e., the neighbor relations were such that if A has B as a neighbor, B in general does not have A as a neighbor in the later interactions of agents on this DBA network.

3. Zaklan Model via Non-Equilibrium Dynamics of MVM

The traditional Zaklan model [7] consists of a number of homogeneous agents located on a regular or irregular structure. In every time period each network site is inhabited by an individual, spin , who can either be an honest tax payer

, who can either be an honest tax payer  or a cheater

or a cheater . It is assumed that initially everybody is honest. Each period individuals can rethink their behaviour and have the opportunity om become the opposite type of agent they were in the previous period. The network neighborhood of every individual is composed of z people, agents to network nodes. Each agent’s social network may either prefer tax evasion or reject it. Individual decision making depends on two factors: First, the type of network every agent is connected with, exerts influence on what type of citizen she becomes in the respective period. On the other hand, people’s decisions are partly autonomous, i.e. they are not only influenced by the constitution of their vicinity. The autonomous part of individual decision making is responsible for the emergence of the tax evasion problem, because some initially honest tax payers decide to evade taxes and then exert influence on others to do so as well. Applied to tax evasion we can interpret the model as follows: Tax evaders have the greatest influence to turn honest citizens into tax evaders if they constitute a majority in the respective neighborhood. If the majority evades, one is likely also to evade. On the other hand, if most people in the vicinity are honest, the respective individual is likely to become a tax payer if she was a tax evader before. The model also presents an enforcement mechanism that consists of two components: a probability of an efficient audit p; and if tax evasion is detected and punished, the individual remains honest for a number k of periods. One time unit is one sweep through the entire system. The temporal evolution this model can be performed by using an equilibrium or non-equilibrium dynamics. In the MVM on network, the system dynamics traditionally is as follows. We assign a spin variable

. It is assumed that initially everybody is honest. Each period individuals can rethink their behaviour and have the opportunity om become the opposite type of agent they were in the previous period. The network neighborhood of every individual is composed of z people, agents to network nodes. Each agent’s social network may either prefer tax evasion or reject it. Individual decision making depends on two factors: First, the type of network every agent is connected with, exerts influence on what type of citizen she becomes in the respective period. On the other hand, people’s decisions are partly autonomous, i.e. they are not only influenced by the constitution of their vicinity. The autonomous part of individual decision making is responsible for the emergence of the tax evasion problem, because some initially honest tax payers decide to evade taxes and then exert influence on others to do so as well. Applied to tax evasion we can interpret the model as follows: Tax evaders have the greatest influence to turn honest citizens into tax evaders if they constitute a majority in the respective neighborhood. If the majority evades, one is likely also to evade. On the other hand, if most people in the vicinity are honest, the respective individual is likely to become a tax payer if she was a tax evader before. The model also presents an enforcement mechanism that consists of two components: a probability of an efficient audit p; and if tax evasion is detected and punished, the individual remains honest for a number k of periods. One time unit is one sweep through the entire system. The temporal evolution this model can be performed by using an equilibrium or non-equilibrium dynamics. In the MVM on network, the system dynamics traditionally is as follows. We assign a spin variable  with values

with values  to each node of the network. At each step we try to spin flip a node. The flip is accepted with probability

to each node of the network. At each step we try to spin flip a node. The flip is accepted with probability

(1)

(1)

where  is the sign

is the sign  of x if

of x if ,

,  if

if . To calculate

. To calculate  our sum runs over the z nearest neighbors j of spin i on the network. Equation (1) means that with probability

our sum runs over the z nearest neighbors j of spin i on the network. Equation (1) means that with probability  the spin will adopt the same state as the majority of its neighbors. The noise parameter

the spin will adopt the same state as the majority of its neighbors. The noise parameter  plays a role similar to the temperature in equilibrium systems: the smaller q, the greater the probability of parallel aligning with the local majority.

plays a role similar to the temperature in equilibrium systems: the smaller q, the greater the probability of parallel aligning with the local majority.

In this model an agent has an opinion and can assume the value  depending on the opinion of the majority of its neighbors.

depending on the opinion of the majority of its neighbors.

We further use a probability of an efficient audit p. Therefore, if tax evasion is detected by this audit, the agent must remain honest for a number k of time steps. Again, one time step is one sweep through the entire network.

4. Controlling the Tax Evasion Dynamics

In order to verify if there is a phase transition in MVM models on ANs Lima et al. [27] measured the relaxation time  as a funtion of the noise parameter q, independent of our tax question. They started the system with all spins up and a number N of spins equal to 7,174,456 (

as a funtion of the noise parameter q, independent of our tax question. They started the system with all spins up and a number N of spins equal to 7,174,456 ( ). They determined the time

). They determined the time  after which the magnetisation

after which the magnetisation  has flipped its sign for the first time, and then took the median value of nine samples. As one can see in Figure 1, the relaxation time goes to infinity at some positive q value near 0.176 (

has flipped its sign for the first time, and then took the median value of nine samples. As one can see in Figure 1, the relaxation time goes to infinity at some positive q value near 0.176 ( ), indicating a second order phase transition. In contrast, the Ising model on ANs [21] [22] and directed BA networks has no phase transition and agrees with the modified Arrhenius law for relaxation time [23] .

), indicating a second order phase transition. In contrast, the Ising model on ANs [21] [22] and directed BA networks has no phase transition and agrees with the modified Arrhenius law for relaxation time [23] .

Figure 1. Reciprocal logarithm of the relaxation times  on (a) apollonian networks versus q for

on (a) apollonian networks versus q for  (MVM) and (b) directed BA network (IM). The curves are parabolas correponding to an asymptotic Arrhenius law

(MVM) and (b) directed BA network (IM). The curves are parabolas correponding to an asymptotic Arrhenius law  (Figure courtesy of D. Stauffer).

(Figure courtesy of D. Stauffer).

The fraction of tax evaders is

(2)

(2)

where N is the total number and  the honest number of agents. The tax evasion is calculated at every time step t of system evolution.

the honest number of agents. The tax evasion is calculated at every time step t of system evolution.

For MVM it is known that for , half of the people are honest and the other half cheat, while for

, half of the people are honest and the other half cheat, while for  either one opinion or the other opinion dominates. Because of this behavior we set a fixed noise (q) to some values slightly below

either one opinion or the other opinion dominates. Because of this behavior we set a fixed noise (q) to some values slightly below , where the case that agents distribute in equal proportions onto the two alternatives is excluded. We set

, where the case that agents distribute in equal proportions onto the two alternatives is excluded. We set  with

with  (ANs) and

(ANs) and  (DBA) such that we see flips of the whole system in the baseline cases

(DBA) such that we see flips of the whole system in the baseline cases . Then we vary the degrees of punishment (

. Then we vary the degrees of punishment ( , 10 and 50) and audit probability rate (

, 10 and 50) and audit probability rate ( , 10% and 90%). Therefore, if tax evasion is detected, the enforcement mechanism p and the time of punishment k are triggered in order to control the tax evasion level. The punished individuals remain honest for a certain number k of periods, as explained before in Section 3.

, 10% and 90%). Therefore, if tax evasion is detected, the enforcement mechanism p and the time of punishment k are triggered in order to control the tax evasion level. The punished individuals remain honest for a certain number k of periods, as explained before in Section 3.

5. Results and Discussion

Here, we follow the same steps we did in a previous work [18] . Therefore, we first will present the baseline case  and

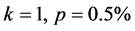

and , i.e., no use of enforcement, at

, i.e., no use of enforcement, at  and with

and with  sites for ANs and DBA. All simulations are performed over 20,000 time steps, as shown in Figure 2. For very low noise the part of autonomous decisions almost completely disappears. The individuals then base their decision solely on what most of their neighbours do. A rising noise has the opposite effect. Individuals then decide more autonomously. Therefore, Figure 2 was expanded to two examples (Figure 2(b) and Figure 2(d)), in order to show how much the results change if one uses various random numbers, average on 20 different seeds. Error bars cannot describe this randomness properly. (For the later figures the error bars are visible from the fluctuations in time which show a band of fractions.) Although everybody is honest initially, it is impossible to predict roughly which level of tax compliance will be reached at some time step in the future.

sites for ANs and DBA. All simulations are performed over 20,000 time steps, as shown in Figure 2. For very low noise the part of autonomous decisions almost completely disappears. The individuals then base their decision solely on what most of their neighbours do. A rising noise has the opposite effect. Individuals then decide more autonomously. Therefore, Figure 2 was expanded to two examples (Figure 2(b) and Figure 2(d)), in order to show how much the results change if one uses various random numbers, average on 20 different seeds. Error bars cannot describe this randomness properly. (For the later figures the error bars are visible from the fluctuations in time which show a band of fractions.) Although everybody is honest initially, it is impossible to predict roughly which level of tax compliance will be reached at some time step in the future.

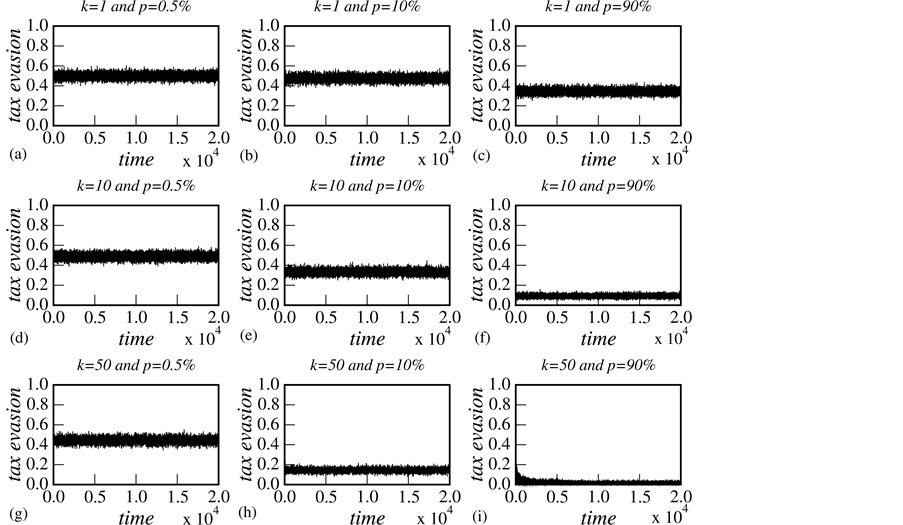

Figure 3 and Figure 4 illustrate different simulation settings for ANs and DBA, for each considered combination of degree of punishment ( , 10 and 50) and audit probability (

, 10 and 50) and audit probability ( , 10% and 90%), where the tax evasion is plotted over 20,000 time steps. Both a rise in audit probability (greater p) and a higher penalty (greater k) work to flatten the time series of tax evasion and to shift the band of possible non-compliance values towards more compliance. However, the simulations show that even extreme enforcement measures (

, 10% and 90%), where the tax evasion is plotted over 20,000 time steps. Both a rise in audit probability (greater p) and a higher penalty (greater k) work to flatten the time series of tax evasion and to shift the band of possible non-compliance values towards more compliance. However, the simulations show that even extreme enforcement measures ( and

and ) cannot fully solve the problem of tax evasion.

) cannot fully solve the problem of tax evasion.

Figure 2. Baseline case:  in (a) and (c), and the average over twenty different seeds in (b) and (d). We use

in (a) and (c), and the average over twenty different seeds in (b) and (d). We use  on both ANs and DBA perform all simulations over 20,000 time steps, also in the later figures.

on both ANs and DBA perform all simulations over 20,000 time steps, also in the later figures.

Figure 3. Tax evasion for ANs and degrees of punishment , 1, 10 and 50 and audit probability

, 1, 10 and 50 and audit probability , 10% and 90%.

, 10% and 90%.

Figure 4. The same as Figure 3, but now for DBA.

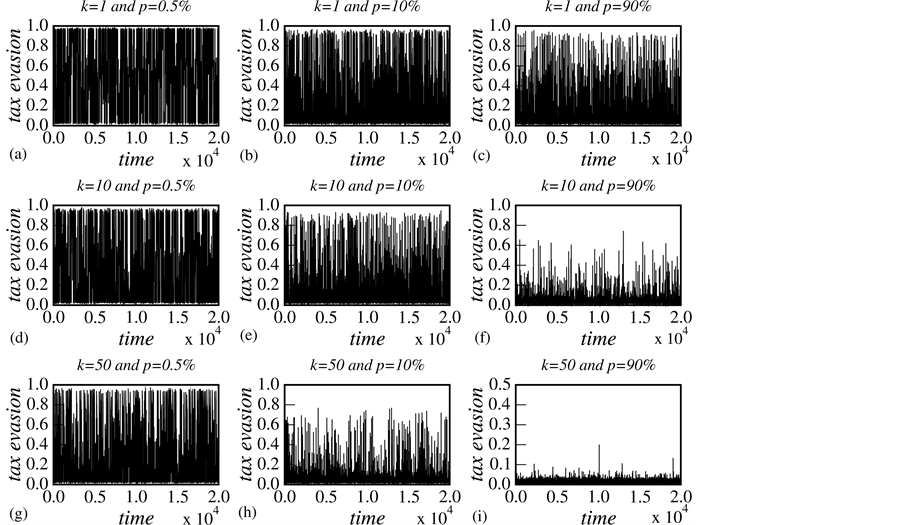

In Figure 5 and Figure 6 we plot tax evasion for ANs and DBA, but now with , again for different enforcement k and audit probability p. Now the fluctuations are much smaller since the network is nearly nine times larger. For case Figure 5(a) and Figure 5(b) we plot the baseline case

, again for different enforcement k and audit probability p. Now the fluctuations are much smaller since the network is nearly nine times larger. For case Figure 5(a) and Figure 5(b) we plot the baseline case  and

and , i.e., no use of enforcement for ANs and DBA and parameters as in Figure 3 and Figure 4. The probable error for part 5(c) fluctuates near 0.0031 (ANs) and is much smaller than the symbols (circle), but the one in 6(c)

, i.e., no use of enforcement for ANs and DBA and parameters as in Figure 3 and Figure 4. The probable error for part 5(c) fluctuates near 0.0031 (ANs) and is much smaller than the symbols (circle), but the one in 6(c)

Figure 5. Tax evasion ANs and degrees of punishment , 1, 10 and 50 and audit probability

, 1, 10 and 50 and audit probability , and 90% for

, and 90% for  sites (nodes) of ANs and using 50,000 time steps. Here, for

sites (nodes) of ANs and using 50,000 time steps. Here, for  and

and  (c), we present the average over twenty different seeds.

(c), we present the average over twenty different seeds.

Figure 6. The same of Figure 5, but now to DBA.

fluctuates near 0.082 (DBA). Case 5(b) with  shows already a strong reduction of tax evasion on ANs, the same does not occur for DBA 6(b). In case 5(c) and 6(c) we show the tax evasion level decreases, on ANs and DBA, for a more realistic set of possible values for the degree of punishment

shows already a strong reduction of tax evasion on ANs, the same does not occur for DBA 6(b). In case 5(c) and 6(c) we show the tax evasion level decreases, on ANs and DBA, for a more realistic set of possible values for the degree of punishment  and audit probability

and audit probability  [7] [15] .

[7] [15] .

In case 5(d) and 6(d) we also show that the tax evasion level decreases much more for an extreme set of punishment  and audit probability

and audit probability  [7] for both networks. Therefore, our model also works for large networks.

[7] for both networks. Therefore, our model also works for large networks.

To understand statistical errors, in Figure 5 and Figure 6 we plot tax evasion for ANs and DBA with  now for the case

now for the case  and

and . We found from 20 samples in part (c) that the tax evasion remains at around 20% (ANs) and 30% (DBA), but with fluctuations in time larger than from sample to sample: The probable errors are much smaller than the fluctuations seen in part (c).

. We found from 20 samples in part (c) that the tax evasion remains at around 20% (ANs) and 30% (DBA), but with fluctuations in time larger than from sample to sample: The probable errors are much smaller than the fluctuations seen in part (c).

6. Conclusion

In this work we show that the Zaklan model of tax evasiom is very robust because we use the non-equilibrium dynamics of the MVM to simulate the Zaklan model, with results similar to equilibrium dynamics of the IM [7] [8] , and also on various topologies [18] . Therefore, as the model of Zaklan incorporates concepts from both sociophysics and econophysics, we argue here that the best framework for simulating this kind of a model is the one of complex networks like ANs and DBA networks, where citizens always make a prior consultation with their nearest neighbors before making any final decisions. Also here we found the plausible result that tax evasion is diminished by higher audit probability p and stronger punishment k on both ANs and DBA networks.

Acknowledgements

F. W. S. Lima thanks Dietrich Stauffer for many suggestions and fruitful discussions during the development of this work. We thank CNPq and FUNCAP for financial support. This work also was supported the system SGI Altix 1350 the computational park CENAPAD.UNICAMP-USP, SP-BRAZIL.

Cite this paper

Francisco W. S.Lima, (2015) Tax Evasion Dynamics via Non-Equilibrium Model on Complex Networks. Theoretical Economics Letters,05,775-783. doi: 10.4236/tel.2015.56089

References

- 1. Stauffer, D., de Oliveira, S.M., de Oliveira, P.M.C. and Martins, J.S.S. (2006) Biology, Sociology, Geology by Computational Physicists. Elsevier, Amsterdam.

- 2. Galam, S. (2012) Sociophysics: A Physicist’s Modeling of Psycho-Political Phenomena. Springer, Berlin-Heidelberg. http://dx.doi.org/10.1007/978-1-4614-2032-3

- 3. Ball, P. (2012) Why Society Is a Complex Matter? Springer, Berlin-Heidelberg.

http://dx.doi.org/10.1007/978-3-642-29000-8 - 4. Helbing, D. (2012) Social Self-Organization: Agent-Based Simulations and Experiments to Study Emergent Social Behavior. Springer, Berlin-Heidelberg. http://dx.doi.org/10.1007/978-3-642-24004-1

- 5. Sen, P. and Chakrabarti, B.K. (2014) Sociophysics—An Introduction. Oxford University Press, Oxford.

- 6. Latané, B. (1981) The Psychology of Social Impact. American Psychologist, 36, 343.

http://dx.doi.org/10.1037/0003-066X.36.4.343 - 7. Zaklan, G., Westerhoff, F. and Stauffer, D. (2008) Analysing Tax Evasion Dynamics via the Ising Model. Journal of Economic Interaction and Coordination, 4, 1. http://dx.doi.org/10.1007/s11403-008-0043-5

- 8. Zaklan, G., Lima, F.W.S. and Westerhoff, F. (2008) Controlling Tax Evasion Fluctuations. Physica A, 387, 5857. http://dx.doi.org/10.1016/j.physa.2008.06.036

- 9. Stauffer, D. (2013) A Biased Review of Sociophysics. Journal of Statistical Physics, 151, 9.

http://dx.doi.org/10.1007/s10955-012-0604-9 - 10. Bloomquist, K. (2006) A Comparison of Agent-Based Models of Income Tax Evasion. Social Science Computer Review, 24, 411. http://dx.doi.org/10.1177/0894439306287021

- 11. Follmer, H. (1974) Random Economies with Many Interacting Agents. Journal of Mathematical Economics, 1, 51-62. http://dx.doi.org/10.1016/0304-4068(74)90035-4

- 12. Andreoni, J., Erard, B. and Feinstein, J. (1998) Tax Compliance. Journal of Economic Literature, 36, 818-860.

- 13. Lederman, L. (2003) The Interplay between Norms and Enforcement in Tax Compliance. Public Law Research Paper No. 49. http://dx.doi.org/10.2139/ssrn.391133

- 14. Slemrod, J. (2007) Cheating Ourselves: The Economics of Tax Evasion. Journal of Economic Perspective, 21, 25-48. http://dx.doi.org/10.1257/jep.21.1.25

- 15. Wintrobe, R. and Gerxhani, K. (2004) Tax Evasion and Trust: A Comparative Analysis. Proceedings of the Annual Meeting of the European Public Choice Society, Berlin, 15-18 April 2004.

- 16. Gachter, S. (2006) Conditional Cooperation: Behavioral Regularities from the Lab and the Field and Their Policy Implications. Discussion Papers 2006-03 CeDEx, University of Nottingham, Nottingham.

- 17. Frey, B.S. and Togler, B. (2006) Tax Evasion, Black Activities and Deterrence in Germany: An Institutional and Empirical Perspective. IEW-Working Papers 286, Institute for Empirical Research in Economics, University of Zurich, Zurich.

- 18. Lima, F.W.S. (2010) Analysing and Controlling the Tax Evasion Dynamics via Majority-Vote Model. Journal of Physics: Conference Series, 246, Article ID: 012033.

http://dx.doi.org/10.1088/1742-6596/246/1/012033 - 19. Lima, F.W.S. (2012) Controlling the Tax Evasion Dynamics via Majority-Vote Model on Various Topologies. Theoretical Economics Letters, 2, 87-93. http://dx.doi.org/10.4236/tel.2012.21017

- 20. Oliveira, M.J. (1992) Isotropic Majority-Vote Model on a Square Lattice. Journal of Statistical Physics, 66, 273-281. http://dx.doi.org/10.1007/BF01060069

- 21. Andrade, R.S.F. and Herrmann, H.J. (2005) Magnetic Models on Apollonian Networks. Physical Review E, 71, Article ID: 056131. http://dx.doi.org/10.1103/PhysRevE.71.056131

- 22. Andrade, R.S.F., Andrade Jr., J.S. and Herrmann, H.J. (2009) Ising Model on the Apollonian Network with Node-Dependent Interactions. Physical Review E, 79, Article ID: 036105.

http://dx.doi.org/10.1103/PhysRevE.79.036105 - 23. Sumour, M.A. and Shabat, M.M. (2005) Monte Carlo Simulation of Ising Model on Directed Barabasi-Albert Networks. International Journal of Modern Physics C, 16, 585-589.

http://dx.doi.org/10.1142/S0129183105007352 - 24. Aleksiejuk, A., Holyst, J.A. and Stauffer, D. (2002) Ferromagnetic Phase Transition in Barabási-Albert Networks. Physica A, 310, 260-266. http://dx.doi.org/10.1016/S0378-4371(02)00740-9

- 25. Albert, R., Jeong, H. and Barabási, A.-L. (1999) Internet: Diameter of the World-Wide Web. Nature, 401, 130-131. http://dx.doi.org/10.1038/43601

- 26. Watts, D.J. and Strogatz, S.H. (1998) Collective Dynamics of “Small-World” Networks. Nature, 393, 440-442. http://dx.doi.org/10.1038/30918

- 27. Lima, F.W.S., Moreira, A.A. and Araújo, A.D. (2012) Nonequilibrium Model on Apollonian Networks. Physical Review E, 86, Article ID: 056109. http://dx.doi.org/10.1103/PhysRevE.86.056109