Low Carbon Economy

Vol.3 No.2(2012), Article ID:20441,4 pages DOI:10.4236/lce.2012.32005

A Study on Establishing Low-Carbon Auditing System in China

![]()

1Accounting Department, Hunan University of Finance and Economics, Changsha, China; 2Hunan University of Finance and Economics, Changsha, China.

Email: xxzhangwei@yahoo.com.cn

Received February 18th, 2012; revised March 18th, 2012; accepted March 26th, 2012

Keywords: Low-Carbon Auditing; Low Carbon Related Law Compliance Auditing; Low-Carbon Conduct Auditing; Low-Carbon Performance Auditing

ABSTRACT

This paper establishes the framework of low-carbon auditing based on the current environment of China which is a developing country. A comprehensive system of low-carbon auditing should be composed by low carbon related laws compliance auditing, low-carbon conduct auditing and performance auditing. The functional paths of low-carbon auditing include at least four things: building a comprehensive low-carbon auditing system, establishing sets of indicators, cultivating talents with diverse carbon related knowledge and providing policies step by step.

1. Introduction

As the increased energy usage leads to rapidly deterioration of global environment, “low-carbon economy” was getting more and more attention since 2003, when the United Kingdom for the first time put forward this concept. The UK Environmental Audit Committee published their work report in December 2009, which involved low-carbon measures and implementation of environment protection, sustainable development and climate change. It could be regarded as the first low-carbon auditing report. Before this, there are some studies on the productlevel carbon auditing [1], carbon labeling [2,3], carbon footprint, but a comprehensive low-carbon auditing system, the pattern, implementation subject and path, specific methods and technique of low-carbon auditing remain unresolved [4-6]. We focus on China in this article to explore the most favorable system of low-carbon auditing and the functions paths related to the realization of it, which can be applied in other developing countries.

The remainder of the paper is structured as follows: Section 2 reviews related literature. Section 3 discusses the framework and content of low-carbon auditing. This is followed, in Section 4, by a discussion of the functional paths to practice low-carbon auditing. A final Section 5 sums up the main findings of the paper.

2. Literature Review

Literature related low-carbon auditing in China focus on three aspects: firstly, the content and classification of low-carbon auditing. Reference [7] put forward the general vision of low-carbon auditing , which should be developed by combination with low-carbon production, low-carbon technique, new energy development and environmental performance auditing, energy saving auditing and energy auditing. There are studies classified the low-carbon auditing into tree types, one is the development and implement of low-carbon policies, the other is auditing supervision of low-carbon financial and tax funs, another is auditing certification of low-carbon economic conduct and products [8]. While other sududies divided low-carbon auditing into research proposals auditing of low-carbon economy policy, execution audit of low-carbon regulations and major policies, performance audit of low-carbon economy funs, low-carbon auditing of clear energy, low-carbon technique audit [9]. These literatures are not very in-depth, and for all of these papers, they didn’t establish a comprehensive low-carbon auditing system, especially, they didn’t point out the practice path of this new kind of auditing. Secondly, studies focus on the low-carbon auditing management. Some focus on the measures to develop low-carbon auditing, which stress mainly on the cultivation of awareness, the training of human resources and institutional innovation [10]. Others regarded it as urgent priority to make sure who should be the subject of low-carbon auditing execution and how to build the judging criteria [11]. These studies pay more attention to micro-level, less concerned about specific technique on the operational level. Thirdly, there are also studies about the specific audit procedure of energy saving audit [12], but the exploration was much more theoretic, less practical. On the whole, low-carbon auditing related literature in developing countries like China is now in the phase of introduce foreign theory and exploring the overall structure of low-carbon auditing, but it’s somewhat fragmented rather than systematic, more attention should be paid to the establishment of a comprehensive and systematic low-carbon auditing system, more importantly, it’s vital to explore the effective functions path and technical methods to achieve the object of this system.

3. The Framework and Content of Low-Carbon Auditing

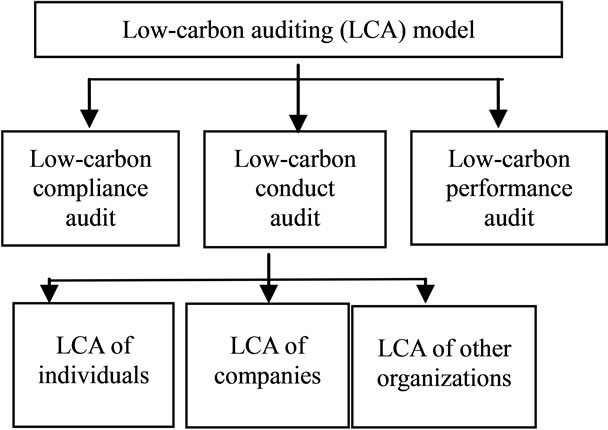

As Figure 1 shown, the framework and content of lowcarbon auditing is breakdown into three categories, namely low-carbon compliance audit, low-carbon conduct audit and low-carbon performance audit. Low-carbon conduct audit could be developed from three dimensions as family or individuals, companies and other organizations. The low-carbon performance mainly means the government level.

3.1. Low-Carbon Compliance Auditing

Low-carbon compliance auditing mainly concerns whether the low-carbon economy related laws, legislations, procedures or rules are abided by organizations or individuals, or the low-carbon related requirements of operation, specific terms of contracts are followed. So it’s necessary to build the framework of low-carbon auditing related main laws and regulations, and probe the principal audit techniques and methods. Who should be the auditors to practice low-carbon compliance auditing? For government departments, it’s sure the internal audit as well as national audit department at all levels can be the auditors, the former can be in charge of the internal auditing and they will pay more attention to prevention, the latter can

Figure 1. The framework of low-carbon auditing.

be responsible for checking whether important low-carbon related laws are abided by, which emphasis more on supervision.

3.2. Low-Carbon Conduct Auditing

Based on the social reality, taking consideration to the practical feasibility, low-carbon conduct audit can be broken down into low-carbon auditing of individuals or family, companies, and other organizations according to the actors. Of these three types of actors, the individuals or families scattered over the nation, it’s the most difficult one to measure their carbon emissions of everyday lives.

Individuals or families are the basic constituent elements of society, which are the most extensive part of low-carbon conduct subject. This kind of low-carbon auditing focus on the everyday life of individuals or families, it stresses more on prevention than on supervising upon specific behavior. In cities, the auditors could be district office, while in rural, it could be the village self-government committee. It’s necessary to establish a series of indicators and general criterion with regard to low-carbon conduct, so that everyday life of individuals and families can be low-carbon oriented. In the initial phase of low-carbon auditing of individuals or family, the audit outcome could be combined to the appraising of outstanding community or village rating, and this kind of audit should be incentive-based at this phase. When the condition gets better, it can be turned to punishment or warning oriented, so that lead people to standardize their behavior to be low carbon oriented.

Low-carbon auditing of companies should be the most meaningful as well as socially impacted part of the whole low-carbon auditing system, this is because it’s industry who should take charge of the most amount of carbon emission, especially for developing countries which are in the process of industrialization. Chinese companies can be classified by the location into two kinds: domestic enterprises and multinational ones. For domestic companies, it’s feasible to build uniform standards on lowcarbon production and operation process. The auditor could be certified public accountants. It’s voluntary for companies to have low-carbon auditing in the beginning, when the standards get relatively perfect, it would be statutory to practice low-carbon auditing for all listed companies, and then extend to other companies step by step, just like the public announcement of financial statements. For multinational companies, they across broads and break the space of nations, as countries are uneven at developmental levels, it’s hard for companies to follow general unified standards. Also, restrictions on carbon emission are quite different between developed countries and developing ones according to UNFCCC. So the international coordination of carbon emission standards is a major issue and prerequisite to carry out low-carbon auditing in multinational companies.

The low-carbon conduct audit of other organizations like schools, social intermediary organizations, non-profit organization etc. could learn from companies, though the nature and goals are different from organization to organization, the final goal of low-carbon conduct remain the same. The enormous difference between companies and other organizations lies in the fact that for companies, we can fully follow the laws of the market, the companies have the freedom of choosing certified auditors. When it turn to organizations which are fiscal subsidized, the auditors may be the national audit departments. For still other organizations which haven’t any national finance funs, the auditors may be certified CPAs, just like the companies do. In addition, all kinds of organizations can be involved into the self-appraise of low-carbon auditing into their internal audit works.

3.3. Low-Carbon Performance Audit

Low-carbon performance audit aims to measure the lowcarbon auditing efficiency and effectiveness of government at all levels. It can be involved into the national audit system, as part of performance audit. To carry out low-carbon performance audit, it’s necessary to build a series of indexes, which mainly based on policies and measures related low-carbon conduct adopted by government. So to develop this performance audit, first and for most important, studies should be thorough concerned about the formulation of related policies, the techniques of low-carbon auditing and the indexes of low-carbon performance, it’s necessary to combination the practice of other kinds of low-carbon auditing.

4. The Function Paths to Practice Low-Carbon Auditing

4.1. Building a Comprehensive Low-Carbon Auditing System

As low-carbon auditing can be divided into different types, a comprehensive low-carbon auditing system is a prerequisite to carry out this auditing. Generally, it should include three kinds of auditors: the national audit, the CPAs and the internal auditors.

4.2. Establishing Sets of Indicators

To improve the feasibility and impartiality, it’s necessary for low-carbon conduct auditing, performance auditing to establish sets of indicators. As the low-carbon compliance auditing is contingency according to the specific project, it’s needless to set standards for auditing. As there are three kinds of low-carbon conduct auditing, then the indicators should be designed based on each one. For the performance auditing of government at all levels, the indicators could be involved into the government performance auditing.

4.3. Cultivating Talents with Diverse Knowledge

As to be competent low-carbon auditor one need to know not only audit technique, but environment science, it’s necessary for auditors to have interdisciplinary knowledge, so cultivating the current auditors with environmental science or training environmental science majors to be auditors are two feasible and relative quick paths to meet the needs of low-carbon auditing in the near future.

4.4. Providing Policies Step by Step

For the practice of low-carbon auditing have some difficulties in reality in China, it’s rational to provide policies step by step. This is quite important, we can lay down long-term plan, for every step there are some feasible measures and specific objectives. Examples are showed in the above analysis of low-carbon conduct audit of companies, other organizations etc.

5. Conclusion

China as a development country is now in the phase of capital-intensive stage of industrialization and urbanization, which is becoming to the world factory by the division of international trade. China’s investment scale is unprecedented, which lead to tremendous pressure of controlling of carbon emission. The UK practice provided an initial pattern of low-carbon auditing, while a comprehensive low-carbon auditing system in China should be composed by low-carbon related law compliance audit, low-carbon conduct auditing and low-carbon performance auditing. The functional paths of low-carbon auditing included at least four things, building a comprehensive low-carbon auditing system, establishing sets of indicators, cultivating talents with diverse knowledge and providing policies step by step.

REFERENCES

- A. C. McKinnon, “Product-Level Carbon Auditing of Supply Chains,” International Journal of Physical Distribution & Logistics Management, Vol. 40, No. 1/2, 2010, pp. 42-46.

- T. Berry, D. Crossley and J. Jewell, “Check Out Carbon: The Role of Carbon Labeling in Delivering a Low Carbon Shopping Basket,” Forum for the Future, London, 2008.

- B. Boardman, S.-K. Bright, K. Ramm and R. White, “Carbon Labeling, Report on Roundtable,” UK Energy Research Centre (UKERC), Oxford, 2007.

- Carbon Trust, “Carbon Footprints in the Supply Chain,” Carbon Trust, London, 2006.

- Carbon Trust, “Working with Boots: Product Carbon Footprinting in Practice,” Carbon Trust, London, 2008.

- Carbon Trust, “Working with Pepsico and Walkers: Product Carbon Footprinting in Practice,” Carbon Trust, London, 2008.

- W. Tian, “Probing on the Low Economic Auditing Model,” Commercial Accounting, Vol. 194, No. 9, 2010, pp. 7-9.

- Z. D. Li and L. Yan, “Motivation, Objective and Content of Low Economy Auditing,” Monthly Journal of Auditing, Vol. 188, No. 9, 2010, pp. 21-22.

- L. L. Jiang, “Probing on the Low Economy Auditing Model Using the Immune System Theory,” Chinese Agricultural Accounting, Vol. 130, No. 1, 2011, pp. 56-58.

- J. P. Wen and T. Li, “Analysis on the Auditing Mechanism Based on Low Economy,” Commercial Accounting, Vol. 206, No. 21, 2010, pp. 45-47.

- Y. X. He, “It’s Necessary to Build Perfect Low Carbon Auditing Standard,” Chinese Auditing Newspaper, 12 January 2011.

- Y. Ma, “The Implementing Frame of Energy Auditing Based on the Sustainable Development,” Commercial Accounting, Vol. 195, No. 10, 2010, pp. 59-60.