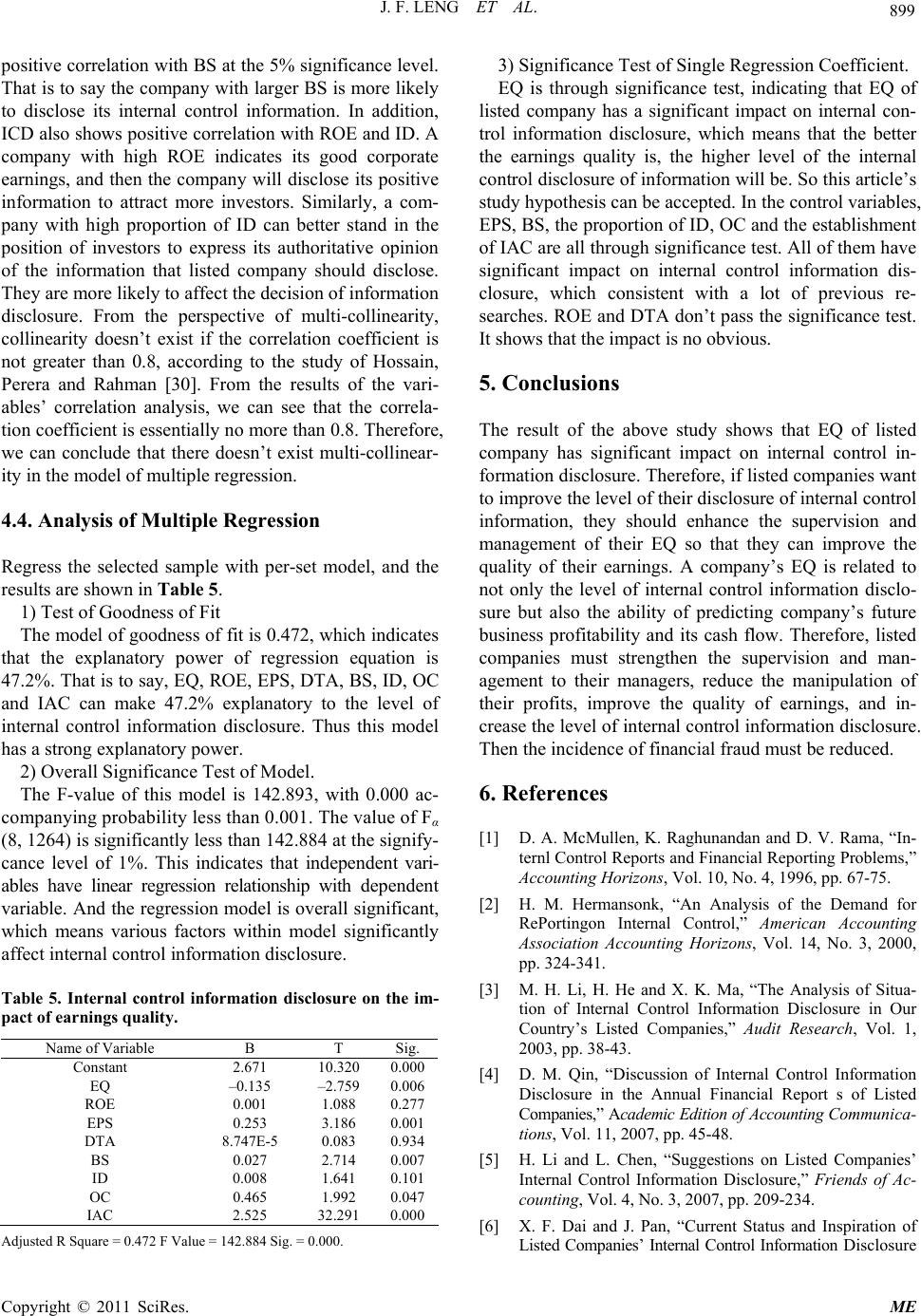

Modern Economy, 2011, 2, 893-900 doi:10.4236/me.2011.25100 Published Online November 2011 (http://www.SciRP.org/journal/me) Copyright © 2011 SciRes. ME 893 Analysis of the Relationship between Listed Companies’ Earnings Quality and Internal Control Information Disclosure* Jianfei Leng, Lu Li School of Business, Hohai University, Nanjing, China E-mail: ljf200209@gmail.com, lilu_nanjing@sina.com Received September 11, 2011; revised October 10, 2011; accepted October 22, 2011 Abstract This article examines the relationship of earnings quality and internal control disclosure information in the sample of 1273 nonfinancial firms in shanghai and Shenzhen Stock Exchange in 2010. Using multiple re- gression model, we launch an empirical analysis on the relationship between earnings quality and internal control disclosure information. We find a positive relation between earnings quality and internal control dis- closure information. The better the earnings quality is, the higher level of the internal control disclosure in- formation will be. This provides a theoretical support to perfect our system of internal control disclosure of information, and to reduce the occurrence of financial fraud. Keywords: Earnings Quality, Internal Control, Disclosure of Information 1. Introduction The cases of financial fraud lead to incalculable losses in these years, which are related to firm’s weak system of internal control. Now, both domestic and foreign have issued a series of legal norms. For example, Sarbanes- Oxley (SOX) Act force listed Companies to disclose their internal control information, including internal con- trol deficiencies and internal self-assessment report and external auditor’s audit opinion. We formulate two im- portant files: “Shanghai Stock Exchange listed compa- nies internal control guidelines” and “Shenzhen Stock Exchange listed companies internal control guidelines”. These files require companies to disclose internal control self-assessment report and comments of external audi- tor’s audit, which greatly improve company’s effective- ness of internal control and quality of financial informa- tion. Accounting earnings is the score and one of the most important elements in all of the accounting infor- mation, which mainly refers to the company’s ability of forecasting future net cash flow. Higher earnings quality is the key to the effective function of the market and the insurance of the company’s future cash flow. The better quality of company’s earnings inclined to disclose more internal control information and to get more outside in- vestment. Therefore, earnings quality is one of the most important factors to affect internal control information disclosure. In this article, with the analysis of multiple regressions, we examine the relationship of earnings quality and internal control disclosure of information in the sample of 1273 nonfinancial firms in shanghai and Shenzhen Stock Exchange in 2010. 2. Prior Research on Internal Control Information Disclosure Listed companies’ internal control information disclosure is mostly voluntary before 2002, but few companies are willing to do so. Since Sarbanes-Oxley (SOX) Act is enforced, many listed companies are forced to disclose their information of internal control, which providing more material and information to scholars who study listed companies’ internal control. Researches on internal control information disclosure are mainly concentrated on the following four aspects: 1) The current situation and solutions of internal con- trol information disclosure. *Fund: operation expenses for Hohai university’s basic scientific re- search of central authorities “Research of internal control Information Disclosure in Chinese listed companies” (2009B23514). There are lots of researches on the current situation of internal control information disclosure, Mc. Mullen, Ra-  J. F. LENG ET AL. 894 gahunandan and Rama [1] studied 4154 companies dur- ing 1989-1993, suggesting that only 26.5% companies are willing to disclose their internal control information, and that only 10.5% provide their internal control report among those companies with deficiencies on their finan- cial reports. It shows that the proportion of companies voluntarily disclosing their internal control information is little, and that the companies with deficient financial report are more unwilling to provide the internal control self-assessment report. Hermanson [2] also did corre- sponding empirical research on listed company’s internal control information disclosure and got the same conclu- sion. Minghui Li [3] and Dongmei Qin [4] made related researches on the current situation of internal control information disclosure. They believed that current listed companies’ enthusiasm of disclosing internal control in- formation is not strong, and much internal control infor- mation was not substantial but formal. Minghui Li [3] also drawn on the experiences of the United States in internal control information disclosure, and provided a series of suggestions and measures of improving internal control information disclosure. Hua Li, Lina Chen [5], Xiaofeng Dai and Jun Pan [6] analyzed the current situa- tion of internal control information disclosure with in- ternal control theories, and pointed out the problems and put forward the corresponding solution. Xinhua Dai and Qiang Zhang [7] mainly did the research on listed banks’ internal control information disclosure, finding that our listed banks’ system of internal control information dis- closure is not standardized and sufficient. They inter- preted the corresponding requirements of the US internal control information disclosure set by “Sarbanes-Oxley Act”, suggesting China to promote the improvement of listed banks’ internal control information step by step. According to relevant provisions of internal control in- formation disclosure required by “Shanghai Stock Ex- change Guidelines” and “The Notice on Listed Compa- nies’ Annual Report in 2006”, Youhong Yang and Wei Wang [8] analyzed the internal control information dis- closure of listed companies on Shanghai Stock Exchange in 2006 with descriptive statistics, and found many problems. 2) Impact factors of internal control information dis- closure. Bronson, carcello, Raghunandan [9] and Doyle, Ge, McVay [10] suggested that there is a correlation between corporate identity and internal control information dis- closure. Company size, the proportion of institutional investor holding, the number of audit committee and the speed of earnings growth have impact on internal control information disclosure. Many other experts did empirical study on such question. Ge and McVay [11] used a sur- vey method to analyze the sample, discovering that the disclosure of material defects is related to the complexity of the company but there is no direct correlation with company size and profitability. Jifu Cai [12] made a relevant empirical study of A-share listed companies to find impact factors of listed companies’ internal control information disclosure. The results showed that the com- panies with a better operating performance and higher reliability of financial report are more inclined to dis- close its internal control information, and vice versa. This indicates that the company’s operating performance and reliability of financial report affect the listed compa- nies’ internal control information disclosure. Adrew J. Lcone [13] selected listed companies who disclosed ma- terial defects of their internal control information in their annual reports as samples to study the impact factors of internal control information disclosure. The results show that the complexity of corporate structures, the changes in company structure and the inputs to internal control are all the impact factors of internal control information disclosure. Shaoqing Song and Yao Zhang [14] studied A-share listed companies on Shanghai and Shenzhen Stock Exchange from 2006 to 2007, finding that there is a correlation between corporate governance characteris- tics and internal control information disclosure. Audit committee, annual statistics, company size and the place of listing have a significant impact on internal control information disclosure. Bin Wang and Huanhuan Liang [15] studied 1884 listed companies on Shenzhen Stock Exchange between 2001 and 2004. They made use of their rating reports of information disclosure quality to examine the inherent relationship between listed compa- nies’ corporate governance characteristics, characteristics of operating condition and information disclosure quality, finding that corporate governance characteristics and characteristics of operating condition have a certain im- pact on internal control information disclosure. 3) The cost of internal control information disclosure. The studies on the cost of internal control information disclosure are not very much. J. Efrim, Boritz, Ping Zhang [16] thought that the costs of disclosing internal control information is enormous, and the management did not believe that the benefits of internal control in- formation disclosure would surpass the corresponding costs. Maria [17] analyzed the sample which discloses their internal control information in accordance with SEC requirements, primarily study the relationship be- tween the costs of disclosing internal control information and the effectiveness of the internal control system. It is found that the cost of disclosing deficiencies of internal control information is far more than that of defect-free. 4) Correlation between internal control and earnings quality. There are many researches on the correlation between Copyright © 2011 SciRes. ME  895 J. F. LENG ET AL. internal control and earnings quality. Doyle [11] studied the relationship between internal control and earnings quality, and found that internal control is a motivation of earnings quality. The studies of Chan [18] and Goh and Li [19] are similar. Chan [18] discovered that earnings management of those who disclose the material defects of internal control has a higher degree but the return on investment is very low. Goh and Li’s [19] also found that company’s earnings stability can be increased after im- proving the defects of internal control. Lobo and Zhou [20] made a comparison on companies’ discretionary accruals between before implementing “Sarbanes-Oxley Act” and after implementing it, finding that companies’ discretionary accruals decreased a lot after the imple- mentation of “Sarbanes-Oxley Act”. Doyle, Ge and Mcvay [10] divided the internal control defects into two aspects: corporate level and account level, finding that internal control defects on corporate level is influential to earnings quality, but there is no correlation between in- ternal control defects on account level and earnings qual- ity. Guoqing Zhang [21] selected non-financial A-share listed companies in 2007 as a research object to study the internal control quality on earnings quality. The results have shown that there is no close link between high qual- ity internal control and earnings quality, but company’s characteristics and corporate governance factors may affect internal control quality and earnings quality sys- tematically. Chunsheng Fang et al. [22] used question- naire survey to examine the relationship between internal control system and financial reporting quality, finding that financial reporting quality improved after imple- mentation of internal control system. Jun Zhang and Junzhi Wang [23] selected listed companies on Shanghai Stock Exchange in 2007 as sample, and used adjusted Jones model to calculate discretionary accruals and found that discretionary accruals significantly reduced after the review of internal control. Shengwen Xie and Wenhai Lai [24] selected A-share listed companies on Shanghai Stock Exchange in 2007 and 2008 as samples. They analyzed the relationship between internal control deficiencies and earnings quality by using a paired study, and found that listed companies’ internal control infor- mation disclosure had an effect on earnings quality. Based on the above studies, we can see that internal control gets more attention after the promulgation of “Sarbanes-Oxley Act”. Current researches centralize on the defects of existing laws and regulations, the current situations of listed companies’ internal control informa- tion disclosure, the relationship between listed compa- nies’ internal control information disclosure and their operating conditions, financial report quality and earn- ings quality. Among the current studies, most have fo- cused on descriptive statistics and the relationship be- tween internal control quality and earnings quality, while there is no study use earnings quality as explanatory variable to reflect its effect on internal control informa- tion disclosure. Therefore, this article uses earnings qual- ity as main explanatory variable and disclosure of inter- nal control as the dependent variable to do empirical study, which compensate for the lack of current research to some extent. 3. Method 3.1. Hypothesis Hypothesis: the better the quality of earnings is, the higher the level of internal control information disclosure will be. According to agency theory and signaling theory, corporate trustee has obligation to report relevant infor- mation to the corporate capital owners, which give help to the operation of business. In the process of reporting, corresponding information is to pass the corporate rele- vant signal to the capital market. The signal can make the operator affect the flow of resources in capital market in a certain extent to improve the enterprise’s interests. There is the mutually reinforcing relationship between internal control information disclosure and the quality of earnings. A company that can fully disclose its informa- tion of internal control means that its managers have a good description of ethics. Meanwhile, a company that can take the initiative to show its internal control infor- mation in detail indicates that its company has a higher self-confidence, which will attract more capital market resources, increase its cash flow, enhance the quality of earnings, and improve management capabilities. Con- versely, companies with good earnings quality will choose to voluntarily disclose their information of inter- nal control in detail. They can distinguish themselves to the companies with inferior earnings quality and get more favor from investors. 3.2. Variable Selection and Definitions 3.2.1. Depe ndent Variable In this paper, we use internal control index to substitute internal control information disclosure (ICD) to test the full of detail of internal control information disclosure. The selection criteria of internal control information dis- closure item are “listed company’s internal control guide- lines on Shanghai Stock Exchange” and “listed com- pany’s internal control guidelines on Shanghai Stock Exchange”. The eight items of information disclosure are: internal environment, risk assessment, control activists, information and communication, internal oversight, in- Copyright © 2011 SciRes. ME  J. F. LENG ET AL. Copyright © 2011 SciRes. ME 896 Model. come and the last year’s main business income in com- pany i. ternal control deficiencies, internal evaluation and exter- nal evaluation. The eight items cover almost all major information that stakeholders needed and reflect the real situation of internal control by a large margin, which can accurately reflect the level of companies’ internal control information disclosure. The specific method of operation is scoring method, that is, make scores to the eight items. Disclose one item gets one point, otherwise gets zero, then the sum of the eight items is the internal control information disclosure index. ,it REC : the margin of the current accounts receiv- able balance and the last year’s accounts receivable bal- ance in company i. ,it : residuals, controllable profits is its absolute value. PPE e : the current total fixed assets of company i. ,it 1 , 2 , 3 : general parameters, can be estimated by basic Jones model with the year’s data: , ,1 1,12, ,1 3,,1 1 it ititit it itit TA AAREVA PPE A 3.2.2. Independent Variables The company’s earnings quality is the company’s ac- counting earnings quality. Acruals quality is widely used as a proxy variable of earnings quality. Healy [25] di- vided accruals into discretionary accruals and non-discretionary accruals. Many scholars believe that the level of discretionary accruals could measure the level of earnings quality. This article makes discretionary accruals as an alternative to earnings quality to be esti- mated in the modified cross-section Jones 3.2.3. Cont rol Variables ,,11 ,1 2, ,, 3,,1, 1 it itit itit it it itit TA AA REVREC A PPE Ae 1 , In addition to the study of the earnings quality on inter- nal control information disclosure, there is a lot of re- searches about the impact factors of internal control in- formation disclosure. Disclosure of internal control in- formation can’t be completely attributed to earnings quality. Many other factors should be taken into consid- eration as well. Bronson, Carcello, Raghunandan [9] and Doyle, Ge, McVay [10] thought that company’s charac- teristics are related to internal control information dis- closure. Company size, the stake holding proportion of institutional investors, the number of attending meeting of audit committee and the income growth all affect the internal control information disclosure. Shaoqing Song and Yao Zhang [14] also discovered that there is correla- tion between corporate governance characteristics and internal control information disclosure. Therefore, this article selects controlling variable from the basic charac- teristics of company, company performance and corpo- rate governance characteristics. The selected control va- riables are classified in Table 1. ,it TA : the current total accruals of company i, ,,it itit TARET CFO ( means the current net profits of company i, ,it means the current cash flow from operating ac- tivities of company i). ,it RET CFO ,1it : the total assets of company i at the end of last year. ,it REV: the margin of the current main business in- Table 1. Variables and their measurement method. Nature of Variables Name of Variables Measurement of Variables Symbols of Variables Dependent Variables Internal Control Information DisclosureScore each item of internal control information disclosure, and then sum them ICD Independent Variables Earnings Quality Calculate operational accruals by using Modified Jones Model EQ Return on Equity Net profits/[(Balance of Shareholders’ Equity at the End of Period + Balance of Shareholders’ Equity at the End of Period/2] × 100% ROE The debt-to-asset ratio Total Liabilities/Total Assets × 100% DTA Earnings Per Share Net Income after Tax/All Ordinary Shares EPS Board Size Number of Board Directors BS The Proportion of Independent DirectorsNumber of Independent Director/Total Number of Board Directors ID Ownership Concentration Proportion of the top five shareholders OC Controlling Variables Internal Audit Agency Dummy Variable, Establishment = 1; 0 Otherwise IAC  897 J. F. LENG ET AL. 1) Return on Equity (ROE): ROE is rate of return on common stockholders’ equity. ROE reflects the income of company’s net assets and the company’s profitability. The level of ROE reflects the level of strength of corporate profitability. Jifu Cai [12] believed that listed companies with good operating per- formance tend to disclose their internal control informa- tion. 2) The Debt-to-Asset Ratio (DTA). DTA is the reflection of the comprehensive ability. The level of the DTA reflects the strength of company’s predictive power. Hossain [26] studied the impact factors of internal control information disclosure twice, He found that debt ratio were positively correlated with the level of disclosure. Thus this article chooses DTA as one of control variables. 3) Earnings per Share (EPS). It is an important indicator of measuring corporation’s operating performance. Lang and Lundholm’s [27] study showed that the better the company’s operating per- formance is, the higher level of internal control informa- tion disclosure will be. Thus this article chooses EPS as one of control variables. 4) Board Size (BS). BD is an important feature of corporate governance. The size of board may also affect the disclosure of inter- nal control information. Yermack [28] used the data of 500 listed companies in US published on “Forbes” ma- gazine between 1981 and 1991. They made a conclusion that the larger the BD is, the worse the corporate per- formance will be, so it can’t play a good role in the dis- closure of information outside. 5) The Proportion of Independent Directors (ID). Independent directors are always independent and generally the experts in economic, legal, accounting and others, they can express their authoritative opinions on the information listed company should disclosure by standing on the position of investors. They are more likely to affect decision-making of information disclo- sure and make them inclined to disclose internal control information. 6) Ownership Concentration (OC). Ownership concentration plays an important role in internal control information disclosure. Wei Zuo and Ye Qiao [29] believed that the higher the ownership concen- tration is, the greater the risk of major shareholders stealing the interests of minority shareholders will be. Then companies tend to disclose more detailed informa- tion to make users understand more about corporate business situations and to protect the interests of minor- ity shareholders. In addition, Hossain [26] found that there is a positive relationship between ownership con- centration and the level of the disclosure of internal con- trol information. Thus the ownership concentration should be one of controlling variables. 7) Internal Audit Agency (IAC). In general, the companies established IAC may attach more importance to the internal control information dis- closure and reduce various types of risk. 3.3. Sample Selection This article selects 1689 listed companies of A-share market main board in Shanghai and Shenzhen Stock Ex- change in 2010, to ensure the validity of data, removing 39 financial and insurance companies and 221 companies listed in the year and 61 companies of delisting and sus- pension of listing and 95 companies of missing data. The indicators data of sample are from Shanghai Stock Exchange (http://www.sse.com.cn), Shenzhen Stock Ex- change (http://www.szse.cn), Huge influx of information network (http://www.cninfo.com) and Ruisi Database (http://www.resset.cn). Data processing using statistic software spss 16.0. 3.4. Model Set This article chooses multiple linear regression models: 01 2345 67 8 CDEQROEDTA EPSBS IDOCIAC e 0 is constant term, (1,2,3,,8) ii is model re- gression coefficients, is residuals. e 4. Empirical Analysis 4.1. Internal Control Information Disclosure Index This article uses internal control information disclosure index to measure the listed company’s internal control information disclosure. According to “listed company’s internal control guidelines on Shanghai Stock Exchange” and “listed company’s internal control guidelines on Shanghai Stock Exchange”, the selected eight items are internal environment, risk assessment, control activists, information and communication, internal oversight, in- ternal control deficiencies, internal evaluation and exter- nal evaluation. The results of information disclosure are shown in Table 2. The statistic results shows that there are 468 compa- nies whose ICD equal and less than 4, accounting for 36.76%, and 805 listed companies equal and more than 5, accounting for 63.24%. This indicates that most compa- nies strictly perform internal control information disclo- Copyright © 2011 SciRes. ME  J. F. LENG ET AL. 898 Table 2. Internal control information disclosure index. ICD Number of Companies Proportion (%) ≤4 468 36.76 ≥5 805 63.24 sure. But we can’t ignore the companies that can’t exe- cute their internal control information disclosure. 4.2. Descriptive Statistical Analysis of Sample Using regression model to analyze each variable, the descriptive analysis results are shown in Table 3. The descriptive statistics results shows that the maxi- mum of ICD is 8, that is to say all eight items are dis- closed; the minimum ICD is 1, it reflects that it didn’t basically disclose the internal control information. The mean is 5.12, which shows that the level of the internal control information disclosure of listed companies is good overall and basically observe the two “Guidelines” requirements. The minimum and maximum value of earnings quality has a large gap. The minimum is 0 and the maximum is 12.62, and the mean is 0.4425. The standard value is 0.85258, which shows that different company differs greatly in earnings quality. ROE is from –991.2% to 1295 %. DTA is from 1% to 699.85%. EPS is from –2.48 to 5.35. These big gaps fully reflect the difference in listed companies’ performance. In the as- pect of corporate governance structure, the differences of all companies are not small. The mean of BS is 12, and the proportion of ID is about 34.689%. Different com- pany has different OC, the top five shareholders of some companies hold nearly 100% shares, which shows that the OC of these companies are very high. The mean of the proportion of top five shareholders is 49.17%, which indicates that the OC of the whole listed companies is very high. As for the establishment of IAC, some com- panies established and some didn’t, which is in the line with reality. 4.3. Correlation Analysis The correlation analysis of variables and the significance level are shown in Table 4. ICD is negatively related to listed company’s EQ and DTA at 1% significance level. The manageability of profit has a negative correlation with the level of internal control information disclosure, and that is to say there is a positive relationship between earnings quality and the level of internal control information disclosure. DTA is negatively related to internal control information disclo- sure, which is contrary to the findings of Hossain’s [26]. ICD is positively related to EPS, OC and the establish- ment of IAC. This shows that the higher the company’s EPS is, the better the company’s performance will be, and then the company is more inclined to disclose its internal control information. The major shareholders in the company with high OC are more likely to steal the interests of minority shareholders. The company is more willing to disclose its internal control information in de- tail. Furthermore, the establishment of IAC can reduce the company’s risk, and this also reflects the attention to internal control information disclosure. The ICD shows Table 3. Descriptive statistical analysis of variables. Variable’s NameMinimumMaximum Mean Standard Value ICD 1.00 8.0 5.1170 1.84108 EQ 0.00 12.62 0.4425 0.85258 ROE –991.201295.00 9.0455 51.73995 EPS –2.48 5.35 0.3427 0.50329 DTA 1.00 699.85 56.8180 38.15713 BS 5.00 34.00 12.7007 3.90804 ID 6.67 80.00 33.6891 8.57244 OC 0.00 0.99 0.4917 0.16806 IAC 0.00 1.00 0.6237 0.48464 Table 4. Correlation analysis of variables. ICD EQ ROE EPS DTA BS ID OC IAC ICD 1.00 EQ –0.163** 1.00 ROE 0.047 –0.047 1.00 EPS 0.118** –0.220** 0.199** 1.00 DTA –0.095** 0.350** –0.040 –0.115** 1.00 BS 0.058* 0.037 0.023 0.051 0.019 1.00 ID 0.028 –0.047 –0.009 0.009 –0.012 –0.284** 1.00 OC 0.082** –0.193** 0.063* 0.230** –0.047 0.041 0.076** 1.00 IAC 0.674** –0.120** 0.007 0.028 –0.100** 0.011 0.001 0.009 1.00 This table presents the results for correlation analysis of variables. **, *Denote significance at the 1% and 5% levels, respectively. Copyright © 2011 SciRes. ME  899 J. F. LENG ET AL. positive correlation with BS at the 5% significance level. That is to say the company with larger BS is more likely to disclose its internal control information. In addition, ICD also shows positive correlation with ROE and ID. A company with high ROE indicates its good corporate earnings, and then the company will disclose its positive information to attract more investors. Similarly, a com- pany with high proportion of ID can better stand in the position of investors to express its authoritative opinion of the information that listed company should disclose. They are more likely to affect the decision of information disclosure. From the perspective of multi-collinearity, collinearity doesn’t exist if the correlation coefficient is not greater than 0.8, according to the study of Hossain, Perera and Rahman [30]. From the results of the vari- ables’ correlation analysis, we can see that the correla- tion coefficient is essentially no more than 0.8. Therefore, we can conclude that there doesn’t exist multi-collinear- ity in the model of multiple regression. 4.4. Analysis of Multiple Regression Regress the selected sample with per-set model, and the results are shown in Table 5. 1) Test of Goodness of Fit The model of goodness of fit is 0.472, which indicates that the explanatory power of regression equation is 47.2%. That is to say, EQ, ROE, EPS, DTA, BS, ID, OC and IAC can make 47.2% explanatory to the level of internal control information disclosure. Thus this model has a strong explanatory power. 2) Overall Significance Test of Model. The F-value of this model is 142.893, with 0.000 ac- companying probability less than 0.001. The value of Fα (8, 1264) is significantly less than 142.884 at the signify- cance level of 1%. This indicates that independent vari- ables have linear regression relationship with dependent variable. And the regression model is overall significant, which means various factors within model significantly affect internal control information disclosure. Table 5. Internal control information disclosure on the im- pact of earnings quality. Name of Variable B T Sig. Constant 2.671 10.320 0.000 EQ –0.135 –2.759 0.006 ROE 0.001 1.088 0.277 EPS 0.253 3.186 0.001 DTA 8.747E-5 0.083 0.934 BS 0.027 2.714 0.007 ID 0.008 1.641 0.101 OC 0.465 1.992 0.047 IAC 2.525 32.291 0.000 Adjusted R Square = 0.472 F Value = 142.884 Sig. = 0.000. 3) Significance Test of Single Regression Coefficient. EQ is through significance test, indicating that EQ of listed company has a significant impact on internal con- trol information disclosure, which means that the better the earnings quality is, the higher level of the internal control disclosure of information will be. So this article’s study hypothesis can be accepted. In the control variables, EPS, BS, the proportion of ID, OC and the establishment of IAC are all through significance test. All of them have significant impact on internal control information dis- closure, which consistent with a lot of previous re- searches. ROE and DTA don’t pass the significance test. It shows that the impact is no obvious. 5. Conclusions The result of the above study shows that EQ of listed company has significant impact on internal control in- formation disclosure. Therefore, if listed companies want to improve the level of their disclosure of internal control information, they should enhance the supervision and management of their EQ so that they can improve the quality of their earnings. A company’s EQ is related to not only the level of internal control information disclo- sure but also the ability of predicting company’s future business profitability and its cash flow. Therefore, listed companies must strengthen the supervision and man- agement to their managers, reduce the manipulation of their profits, improve the quality of earnings, and in- crease the level of internal control information disclosure. Then the incidence of financial fraud must be reduced. 6. References [1] D. A. McMullen, K. Raghunandan and D. V. Rama, “In- ternl Control Reports and Financial Reporting Problems,” Accounting Horizons, Vol. 10, No. 4, 1996, pp. 67-75. [2] H. M. Hermansonk, “An Analysis of the Demand for RePortingon Internal Control,” American Accounting Association Accounting Horizons, Vol. 14, No. 3, 2000, pp. 324-341. [3] M. H. Li, H. He and X. K. Ma, “The Analysis of Situa- tion of Internal Control Information Disclosure in Our Country’s Listed Companies,” Audit Research, Vol. 1, 2003, pp. 38-43. [4] D. M. Qin, “Discussion of Internal Control Information Disclosure in the Annual Financial Report s of Listed Companies,” Academic Edition of Accounting Communica- tions, Vol. 11, 2007, pp. 45-48. [5] H. Li and L. Chen, “Suggestions on Listed Companies’ Internal Control Information Disclosure,” Friends of Ac- counting, Vol. 4, No. 3, 2007, pp. 209-234. [6] X. F. Dai and J. Pan, “Current Status and Inspiration of Listed Companies’ Internal Control Information Disclosure Copyright © 2011 SciRes. ME  J. F. LENG ET AL. 900 in Our Country,” Economy of Special Region, Vol. 10, 2005, pp. 104-105. [7] X. H. Dai and Q. Zhang, “Sarbanes-Oxley Act and Listed Banks’ Internal Control Information Disclosure in Our Country,” Financial Accounting, Vol. 9, 2006, pp. 25-41. [8] Y. H. Yang and W. Wang, “The Study of Companies’ Internal Control Information Disclosure on Shanghai Stock Exchange in 2006,” Accounting Research, Vol. 3, 2008, pp.35-42. [9] S. N. Bronson, J. V. Carcello and K. Raghunandan, “Firm Characteristics and Voluntary Management Reports on Internal Control,” A Journal of Practice & Theory, Vol. 25, No. 2, 2006, pp. 25-39. [10] J. Doyle, W. Ge and S. McVay, “Accruals Quality and Internal Control over Financial Reporting,” The Accounting Review, Vol. 82, No. 5, 2007, pp. 1141-1170. doi:10.2308/accr.2007.82.5.1141 [11] J. Doyle, W. Ge and S. McVay, “The Disclosure of Ma- terial Weaknesses in Internal Control after the Sarbanes- Oxley Act,” Accounting Horizons, Vol. 19, No. 3, 2005, pp. 137-158. doi:10.2308/acch.2005.19.3.137 [12] J. F. Cai, “The Empirical Study of Listed Companies’ Internal Control Information Disclosure in Our Country,” The Audit and Economic Research, Vol. 3, 2005, pp. 85- 88. [13] A. J. Lcone, “Factors Related to Internal Control Dislo- sure: A Discussion of Ashbaugh, Collins, and Kinney (2007) and Doyle, Ge and MeVay (2007),” Journal of Accounting and Economies, 2007, pp. 224-237. [14] S. Q. Song and Y. Zhang, “Impact Factors of Internal Control Information Disclosure from the Corporate Gov- ernance Perspective-Empirical Evidence form Chinese A-Share Market,” Academic Edition of Accounting Com- munications, Vol. 10, 2008, pp. 88-91. [15] B. Wang and H. H. Liang, “Corporate Governance, Fi- nacial Situation and the Quality of Information Disclo- sure-Study Evidence from Shenzhen Stock Exchange,” Accounting Research, Vol. 3, 2008, pp. 33-38. [16] J. E. Boritz and P. Zhang, “How does Disclosure of In- ternal Control Quality Affect Management’s Choice of that Quality,” CAAA 2006 Annual Conference Paper, 2006. [17] M. Ogneva, K. R. Subramanyam and K. Raghunandan, “Intemal Control Weaknesses and Cost of Equity: Evi- dence from SOX Section 404 Disclosures,” AAA 2006 Financial Accounting and Reporting Section (FARS) Meeting Paper, 2006. [18] K. C. Chan, B. R. Farrell and P. C. Li, “Earnings Man- agement and Return Earnings Association of Firms Re- porting Material Internal Control Weaknesses under sec- tion 404 of the Sarbanes-Oxley Act,” 2005. http://ssrn.com/abstract = 744806 [19] B. W. Goh and D. Li, “Internal Control Reporting and Accounting Conservation,” Working Paper, Singapore Management University, TsingHua University, Beijing, 2008. [20] G. J. Lobo and J. Zhou, “Did Conservation Financial Reporting Increase after the Sarbanes-Oxley Act,” Ac- counting Horizons, Vol. 20, No. 1, 2006, pp. 57-74. doi:10.2308/acch.2006.20.1.57 [21] G. Q. Zhang, “Internal Control and Earnings Quality-Based on the Empirical Evidence from A-Share Companies in 2007,” Economic Management, Vol. 23, 2008, pp. 112- 119. [22] C. S. Fang, L. Y. Wang, X. C. Lin, J. Y. Lin and B. Feng, “SOX Act, System of Internal Control and Reliability of Financial Information,” Audit Research, Vol. 1, 2008, pp. 45-52. [23] . Zhang and J. Z. Wang, “Audit of Internal Control and Manipulation of Accruals-Empirical Evidence from Shanghai Stock Exchange,” Learned Journal of Central University of Finance, Vol. 2, 2009, pp. 92-96. [24] S. W. Xie and W. H. Lai, “The Empirical Analysis on Internal Control Information Disclosure and Earnings Quality of Listed Companies in China,” MBA Dissertation, Jiangxi University of Finance and Economics, Nanchang, 2009. [25] P. M. Healy, “The Effect of Bonus Schemes on Accounting Secisions,” Journal of Accounting and Economics, Vol. 7, No. 1-3, 1985, pp. 85-107. doi:10.1016/0165-4101(85)90029-1 [26] M. Hossain, M. M. B. Perera and A. R. Rahman, “Vol- untary Disclosure in the Annual Reports of New Zealand Companies,” Journal of International Financial Man- agement and Accounting, Vol. 6, No. 1, 1995, pp. 69-87. doi:10.1111/j.1467-646X.1995.tb00050.x [27] M. Lang and R. Lundholm, “Crossectional Determinants of Analysts’ Ratings of Corporate Disclosures,” Journal of Accounting Research, Vol. 3, No. 1, 1993, pp. 246- 271. doi:10.2307/2491273 [28] D. Yermack, “Higher Marker Valuation of Companies with a Small Board of Directors,” Journal of Financial Economics, Vol. 23, No. 11, 1996, pp. 116-127. [29] W. Zuo and Y. Qiao, “Impact Factors of Internal Control Information Disclosure of Our Country’s Small and Me- dium Sized Private Listed Companies,” Learned Journal of Nanjing University of Aeronautics and Astronautics, Vol. 3, No. 1, 2009, pp. 32-38. [30] M. Hossain, M. Perera and A. R. Rahman, “Voluntary Disclosure in the Annual Reports of New Zealand Com- panies,” Joumal of International Financial Management and Accounting, Vol. 6, No. 1, 1995, pp. 69-87. doi:10.1111/j.1467-646X.1995.tb00050.x Copyright © 2011 SciRes. ME

|