Applied Mathematics

Vol.4 No.5(2013), Article ID:31445,5 pages DOI:10.4236/am.2013.45108

An Evaluation for the Probability Density of the First Hitting Time

1Department of Mathematics, National Cheng-Kung University, Tainan, Chinese Taipei

2Department of Finance, National Dong Hwa University, Hualien County, Chinese Taipei

Email: *shen@mail.ncku.edu.tw

Copyright © 2013 Shih-Yu Shen, Yi-Long Hsiao. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Received March 7, 2013; revised April 7, 2013; accepted April 14, 2013

Keywords: Brownian Motion; First Hitting Time; Heat Equation; Boundary Value Problem

ABSTRACT

Let  be a smooth function,

be a smooth function,  a standard Brownian motion and

a standard Brownian motion and  the first hitting time. In this paper, new formulations are derived to evaluate the probability density of the first hitting time. If

the first hitting time. In this paper, new formulations are derived to evaluate the probability density of the first hitting time. If  denotes the density function of

denotes the density function of  for

for , then

, then  and

and . Moreover, the hitting time density

. Moreover, the hitting time density  is

is . Applying some partial differential equation techniques, we derive a simple integral equation for

. Applying some partial differential equation techniques, we derive a simple integral equation for . Two examples are demonstrated in this article.

. Two examples are demonstrated in this article.

1. Introduction

Since the publication of Black and Scholes’ [1], and Merton’s [2] papers in 1973, a stock price following a geometric Brownian motion becomes the standard model for the dynamics of a stock price. Therefore, the calculations for the first hitting time get important in the field of finance recently [3].

Let  be a smooth function for

be a smooth function for , and

, and

a standard Brownian motion. The first hitting time

a standard Brownian motion. The first hitting time  is defined as

is defined as . It is known that

. It is known that  has a continuous density [4]. Sometime we call the function

has a continuous density [4]. Sometime we call the function  or the curve

or the curve  the barrier. For a constant barrier, the result has been wellknown for a long time. In this case, the density is

the barrier. For a constant barrier, the result has been wellknown for a long time. In this case, the density is

([5], Chapter 9). The distribution of the hitting time for non-constant barrier was considered by many authors; for example in [6-9]. In [6], Cuzick developed an asymptotic estimate for the first hitting density with a general barrier. In [7,8], the authors’ formulas contain an expected value of a Brownian function. The formulations in [7] are hard to see how the density for a general barrier is evaluated. Although the expected value in [8] can be evaluated by solving a partial differential equation, using a numerical method to compute the value is still not easy. In [9], the density function for parabolic barriers was expressed analytically in terms of Airy functions. In this article, we derive new exact formulations for the hitting density with a general barrier. Thus, partial differential equation (PDE) techniques may be applied to evaluate the density function of the first hitting time. Let

([5], Chapter 9). The distribution of the hitting time for non-constant barrier was considered by many authors; for example in [6-9]. In [6], Cuzick developed an asymptotic estimate for the first hitting density with a general barrier. In [7,8], the authors’ formulas contain an expected value of a Brownian function. The formulations in [7] are hard to see how the density for a general barrier is evaluated. Although the expected value in [8] can be evaluated by solving a partial differential equation, using a numerical method to compute the value is still not easy. In [9], the density function for parabolic barriers was expressed analytically in terms of Airy functions. In this article, we derive new exact formulations for the hitting density with a general barrier. Thus, partial differential equation (PDE) techniques may be applied to evaluate the density function of the first hitting time. Let  be the probability density of

be the probability density of ;

;

i.e. . It will be shown that

. It will be shown that  is the solution of an initialboundary value problem of a heat equation, and the hitting density is

is the solution of an initialboundary value problem of a heat equation, and the hitting density is . Our derivation results a simple integral equation for the density function.

. Our derivation results a simple integral equation for the density function.

In Section 2, we show that the density function of the first hitting time can be evaluated though solving an initial-boundary value problem of the heat equation. Then, the density function will be the solution of a simple integral equation. In Section 3, a couple of examples are solved by PDE techniques to demonstrate the justification of the new method. The last section is the conclusion.

2. The Boundary Value Problem

Let Bt,  , a standard Brownian motion,

, a standard Brownian motion,  be a smooth function and

be a smooth function and  the first hitting time. We consider

the first hitting time. We consider  first. Let

first. Let  denote the probability

denote the probability , and

, and  denote the density function

denote the density function . Surely,

. Surely,  fulfills the heat equation,

fulfills the heat equation,  ([10], p. 352). Nevertheless, in this section, it will be proven with another way. To derive the formulations for

([10], p. 352). Nevertheless, in this section, it will be proven with another way. To derive the formulations for , we consider the hitting problem at discrete times

, we consider the hitting problem at discrete times , where

, where

. Let

. Let  denote

denote

and

and  denote

denote . Therefore,

. Therefore,

(1)

(1)

where  and

and . Taking the limit, we have

. Taking the limit, we have

(2)

(2)

and

(3)

(3)

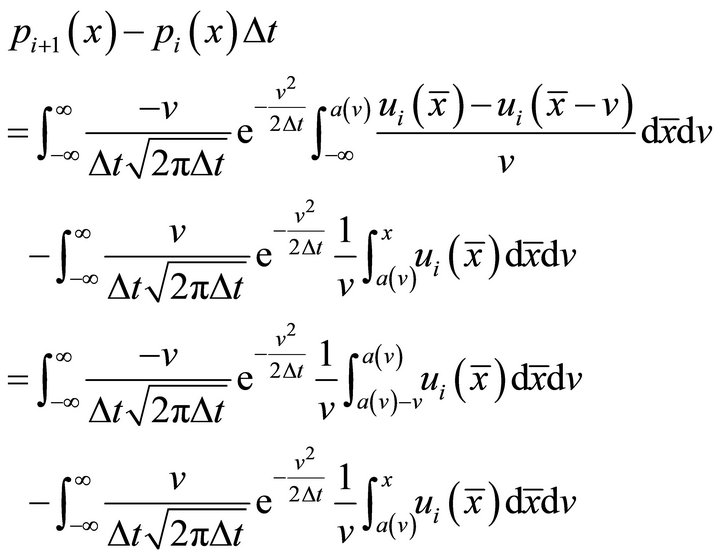

We will show that  satisfies the heat equation. Integrating Equation (1), we have

satisfies the heat equation. Integrating Equation (1), we have

(4)

(4)

for . The probability difference between two steps is

. The probability difference between two steps is

(5)

(5)

Using a substitution,  , we have

, we have

where

Consequently,

(6)

(6)

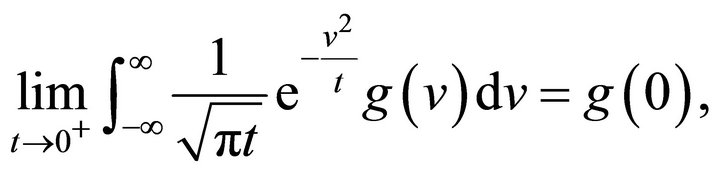

Note that, if  is continuous and bounded

is continuous and bounded

([11], p. 9) and, therefore, if

Let

The function  is continuous and bounded. Moreover,

is continuous and bounded. Moreover,  is differentiable, since

is differentiable, since

Thus, when  approaches 0, the first term of the right-hand side of Equation (6) is

approaches 0, the first term of the right-hand side of Equation (6) is . The second term is 0, because

. The second term is 0, because  and, therefore,

and, therefore,  when

when  is small. Letting

is small. Letting  approach 0, we have

approach 0, we have

(7)

(7)

Since , differentiating both sides of Equation (7) with respect to

, differentiating both sides of Equation (7) with respect to , we have the partial differential equation

, we have the partial differential equation

(8)

(8)

The barrier  is assumed to be differentiable, and, therefore, there exists an positive number

is assumed to be differentiable, and, therefore, there exists an positive number  not depending on

not depending on  such that

such that . Consider the probability density near the boundary

. Consider the probability density near the boundary

(9)

(9)

where . Note that

. Note that

When ,

,

Consequently,

We have the boundary condition

(10)

(10)

Therefore, we have a proposition as follows:

Proposition 1

The density function  is subject to the initialboundary value problem:

is subject to the initialboundary value problem:

(11a)

(11a)

(11b)

(11b)

(11c)

(11c)

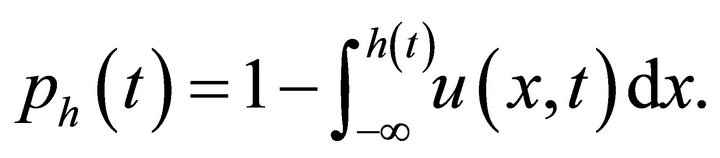

where  is the Dirac delta function. The initialboundary value problem is mathematically well-post. The hitting probability

is the Dirac delta function. The initialboundary value problem is mathematically well-post. The hitting probability ,

,

(12)

(12)

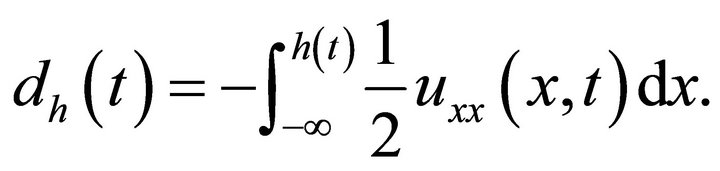

Then, the hitting density

(13)

(13)

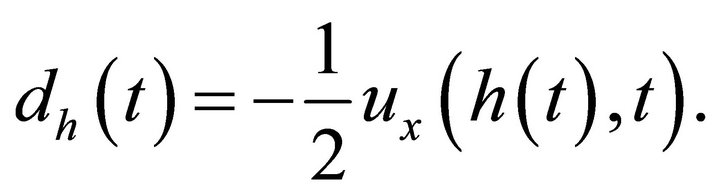

Substituting Equations (8) and (10) into Equation (13), we have

Using integration by parts, we have

(14)

(14)

Similarly, if , the hitting density will be

, the hitting density will be

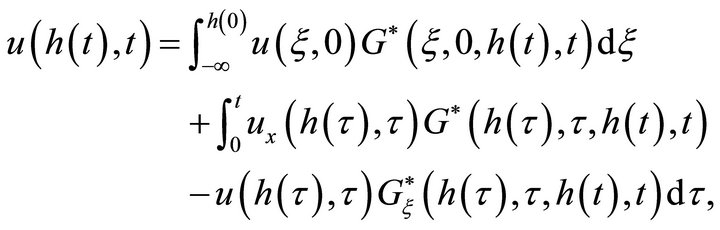

. There is an integral equation for the boundary values of a heat equation ([12], p. 219).

. There is an integral equation for the boundary values of a heat equation ([12], p. 219).

(15)

(15)

where  and

and

is the Heaviside step function. For problem (11), the integral equation becomes

is the Heaviside step function. For problem (11), the integral equation becomes

or

(16)

(16)

Equation (16) can be solved by a numerical method easily.

3. Examples

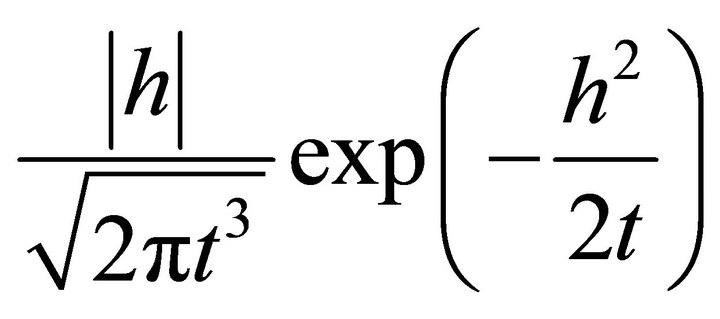

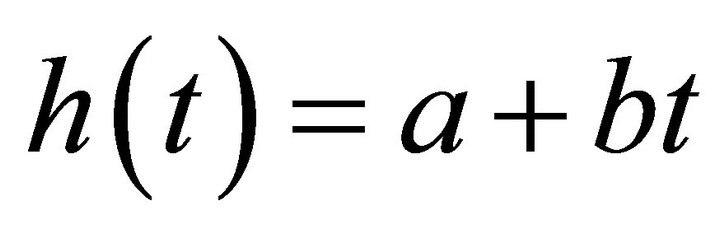

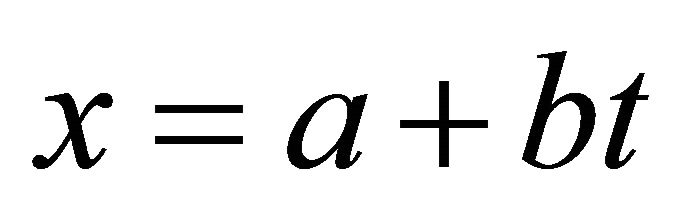

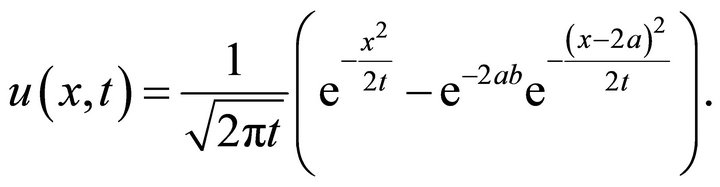

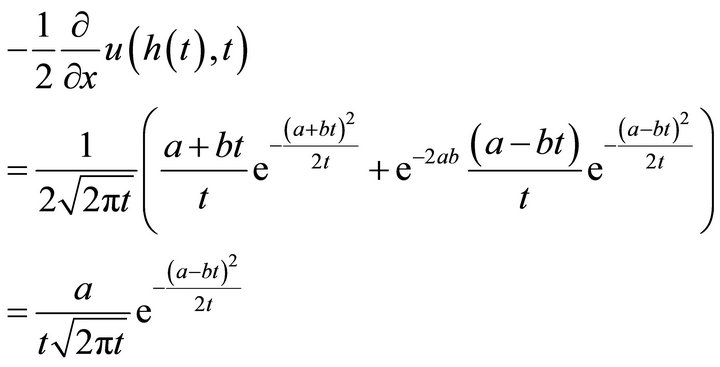

Example 1: Linear boundaries.

Let  with

with . The initial-boundary value problem (11) has a close-form solution. The solution, which is a Green’s function for the boundary

. The initial-boundary value problem (11) has a close-form solution. The solution, which is a Green’s function for the boundary , is

, is

Thus, the hitting density  is

is

consistent with that in [8].

Example 2: First-passage time probability in an interval.

Let  and

and  be the density function for

be the density function for . In this example, we evaluate the probability density of the first passage time

. In this example, we evaluate the probability density of the first passage time .

.

Let  and

and

be the density of . Using

. Using  and

and  to denote the probability density

to denote the probability density

for

for  and

and  respectively, we have an initial-boundary value problem for both functions,

respectively, we have an initial-boundary value problem for both functions,  and

and . From the proposition,

. From the proposition,  and

and  fulfill the equations

fulfill the equations

and

The solutions are

and

The density function is

Thus

The density of  has to be

has to be

(17)

(17)

where  is the density function of

is the density function of ; i.e.

; i.e.

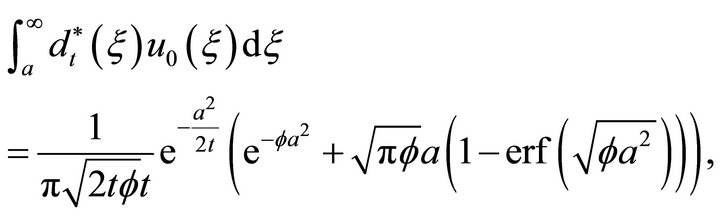

The integral in Equation (17) can be calculated.

where  and

and . Similarly,

. Similarly,

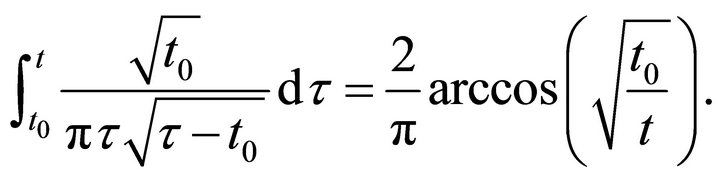

Therefore, the hitting rate

In the special case of ,

,

The probability of that the Brownian motion process takes on the value 0 at least once in the interval  is

is

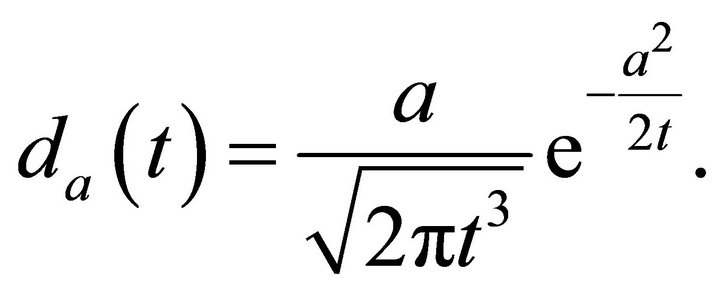

This result is the same as in ([13], p. 191). In a simple case of ,

,

This is the well-known result of the density of the first hitting time for a constant barrier.

4. Conclusions

The proposition proposed in Section 2 may offer a simple way to evaluate the density of the hitting time with a general barrier by solving an initial-boundary value problem of the heat equation. The density function  locally satisfies the heat equation is well-known [10]. The main contribution of this paper is the derivation of the boundary condition (10). This result makes progress in the evaluation of hitting time density. Two examples with exact solutions are demonstrated in Section 3. Even though the examples may be solved by other method, the new formulations in this paper can be applied to evaluate the hitting time distribution with any smooth barrier numerically by using the integral Equation (16).

locally satisfies the heat equation is well-known [10]. The main contribution of this paper is the derivation of the boundary condition (10). This result makes progress in the evaluation of hitting time density. Two examples with exact solutions are demonstrated in Section 3. Even though the examples may be solved by other method, the new formulations in this paper can be applied to evaluate the hitting time distribution with any smooth barrier numerically by using the integral Equation (16).

A similar result for two-dimensional problems may be expected. Let  and

and  be two standard Brownian motion,

be two standard Brownian motion,  a smooth surface and

a smooth surface and

the first hitting time. If  presents the probability density of

presents the probability density of  for

for , the two-dimensional formulations may be as follows,

, the two-dimensional formulations may be as follows,

(18a)

(18a)

(18b)

(18b)

(18c)

(18c)

As long as Equation (18) is established, the probability density of the first hitting time for two-dimensional Brownian motion may be evaluated by an analytical or numerical method.

REFERENCES

- F. Black and M. Scholes, “The Pricing of Options and Corporate Liabilities,” Journal of Political Economy, Vol. 81, No. 3, 1973, pp. 637-659. doi:10.1086/260062

- R. C. Merton, “Theory of Rational Option Pricing,” Bell Journal of Economics and Management Science, Vol. 4, No. 1, 1973, pp. 141-183. doi:10.2307/3003143

- C. Profeta, B. Roynette and M. Yor, “Option Prices as Probabilities,” Springer, New York, 2010. doi:10.1007/978-3-642-10395-7

- B. Ferebee, “The Tangent Approximation to One-Sided Brownian Exit Densities,” Z. Wahrscheinlichkeitsth, Vol. 61, No. 3, 1982, pp. 309-326. doi:10.1007/BF00539832

- G. R. Grimmett and D. R. Stirzaker, “Probability and Random Processes,” Oxford University Press, New York, 1982.

- J. Cuzick, “Boundary Crossing Probabilities for Stationary Gaussian Processes and Brownian Motion,” Transactions of the American Mathematical Society, Vol. 263, No. 2, 1981, pp. 469-492. doi:10.1090/S0002-9947-1981-0594420-5

- J. Durbin, “The First-Passage Density of a Continuous Gaussian Process to a General Boundary,” Journal of Applied Probability, Vol. 22, No. 1, 1985, pp. 99-122. doi:10.2307/3213751

- P. Salminen, “On the First Hitting Time and the Last Exit Time for a Brownian Motion to/from a Moving Boundary,” Advances in Applied Probability, Vol. 20, No. 2, 1988, pp. 411-426. doi:10.2307/1427397

- A. Martin-Löf, “The Final Size of a Nearly Critical Epidemic and the First Passage Time of a Wiener Process to a Parabolic Barrier,” Journal of Applied Probability, Vol. 35, No. 3, 1998, pp. 671-682. doi:10.1239/jap/1032265215

- L. Breiman, “Probability,” SIAM, Philadelphia, 1992. doi:10.1137/1.9781611971286

- J. Kevorkian, “Partial Differential Equations: Analytical Solution Techniques,” Wadsworth, Belmont, 1990.

- F. John, “Partial Differential Equations,” 4th Edition, Springer-Verlag, New York, 1982.

- S. M. Ross, “Stochastic Processes,” John Wiley & Sons, New York, 1983.

NOTES

*Corresponding author.