Paper Menu >>

Journal Menu >>

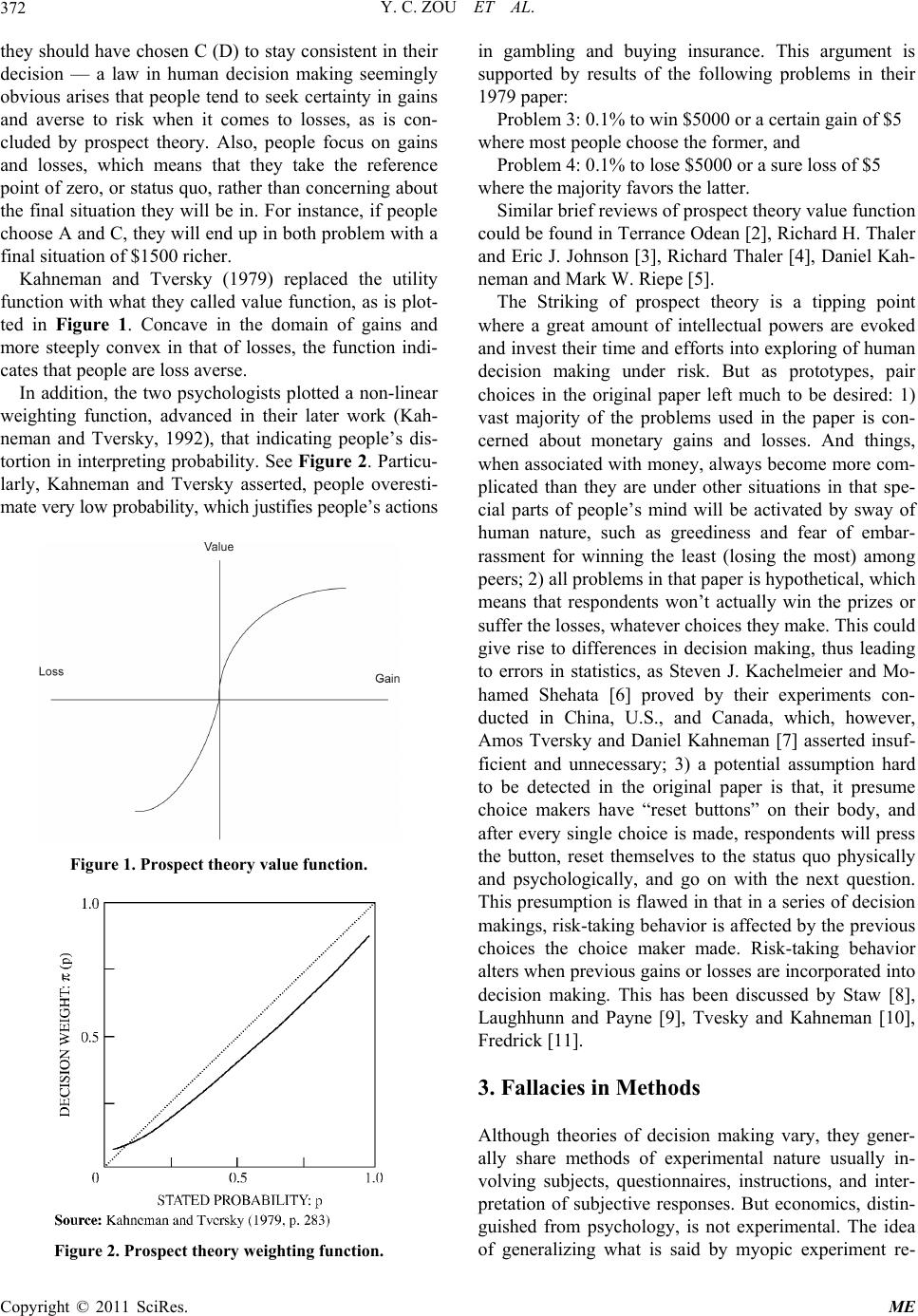

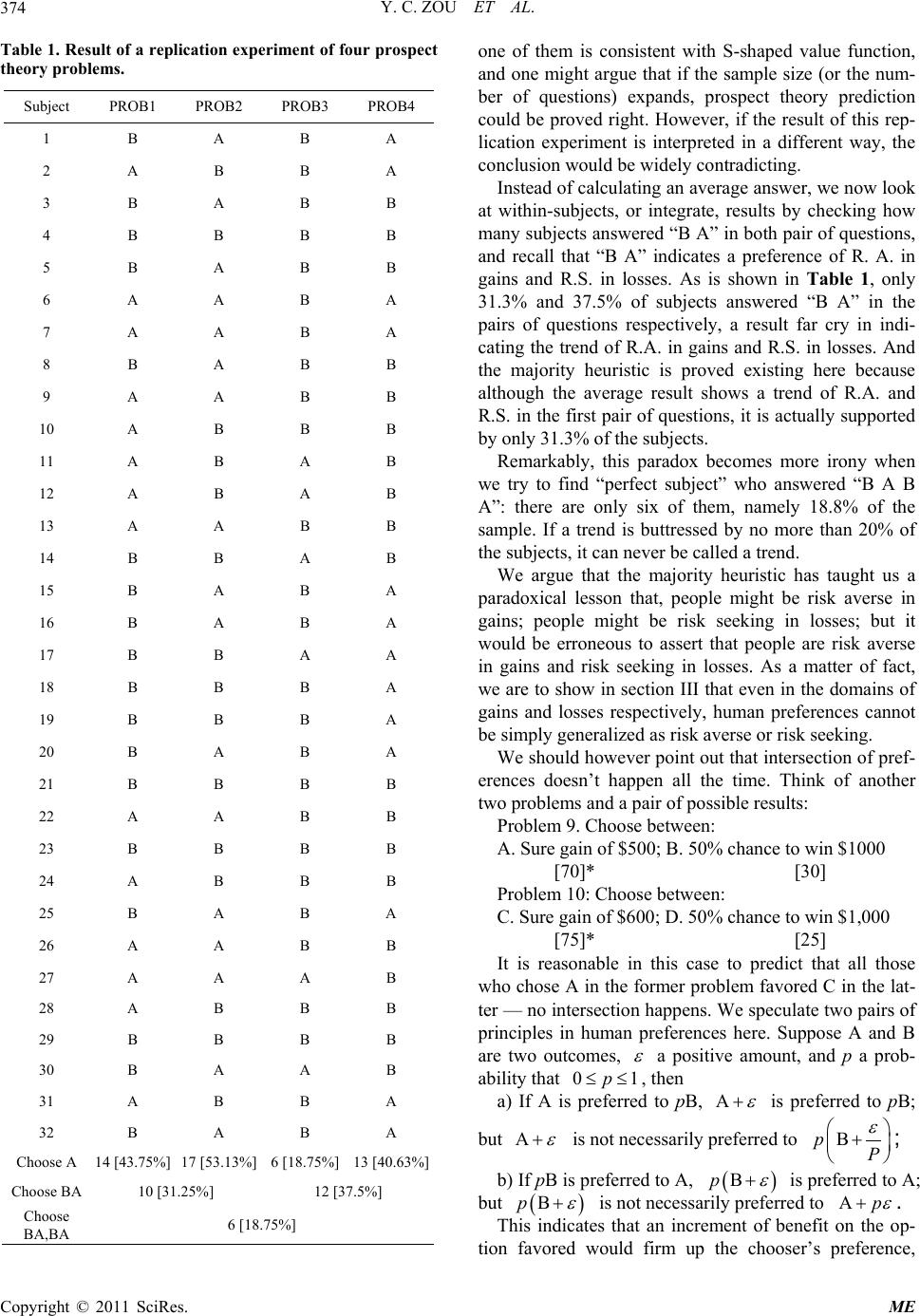

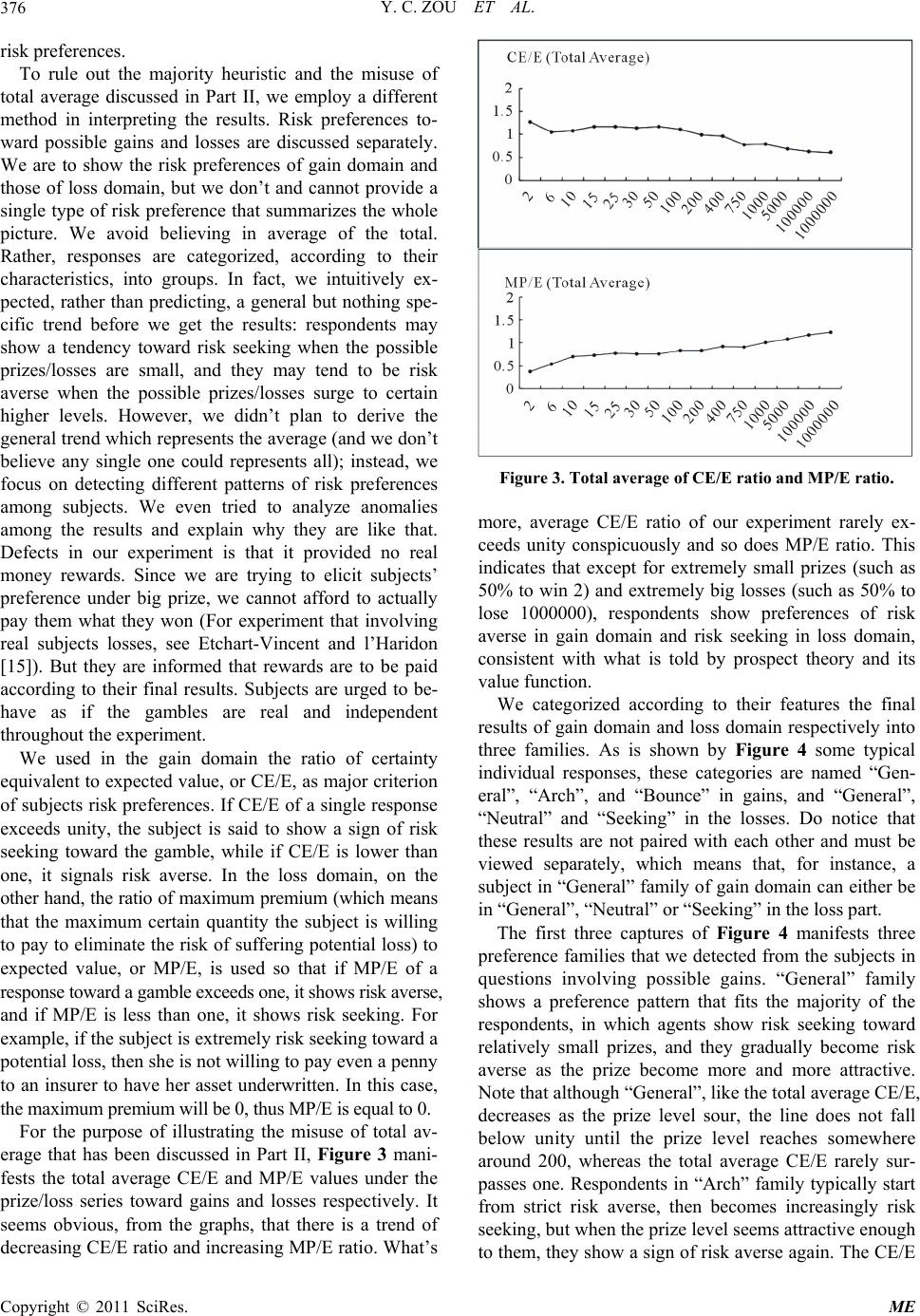

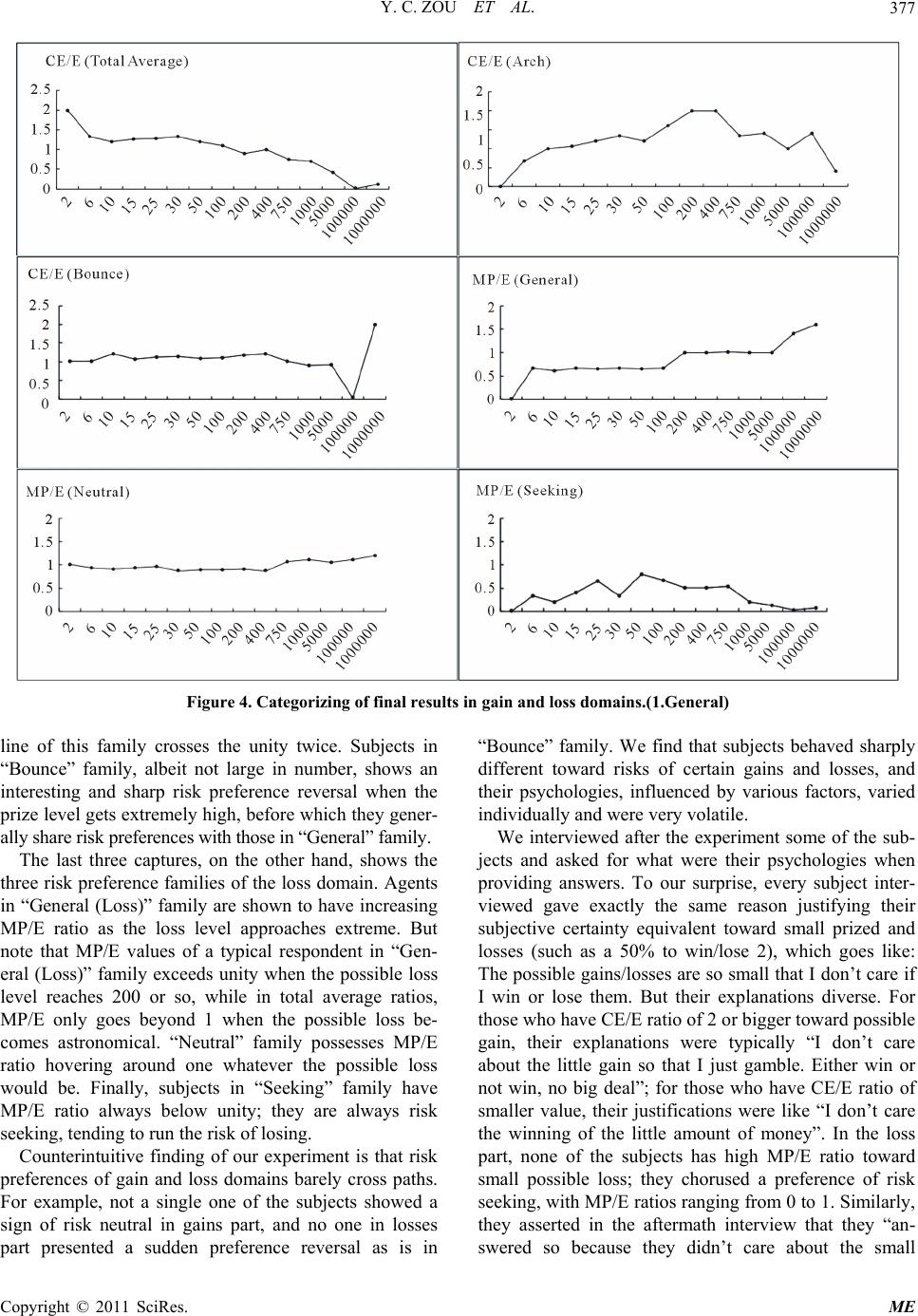

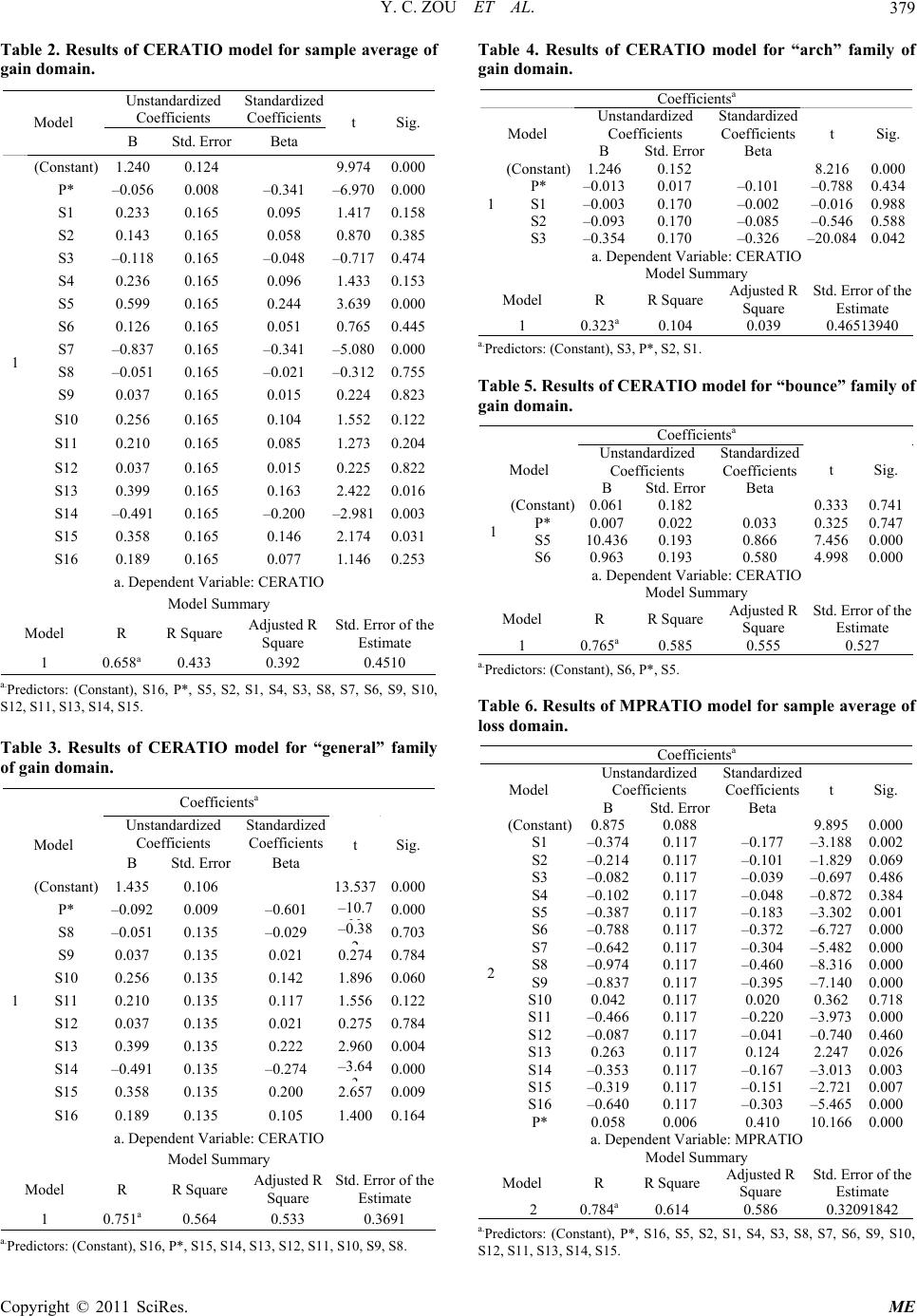

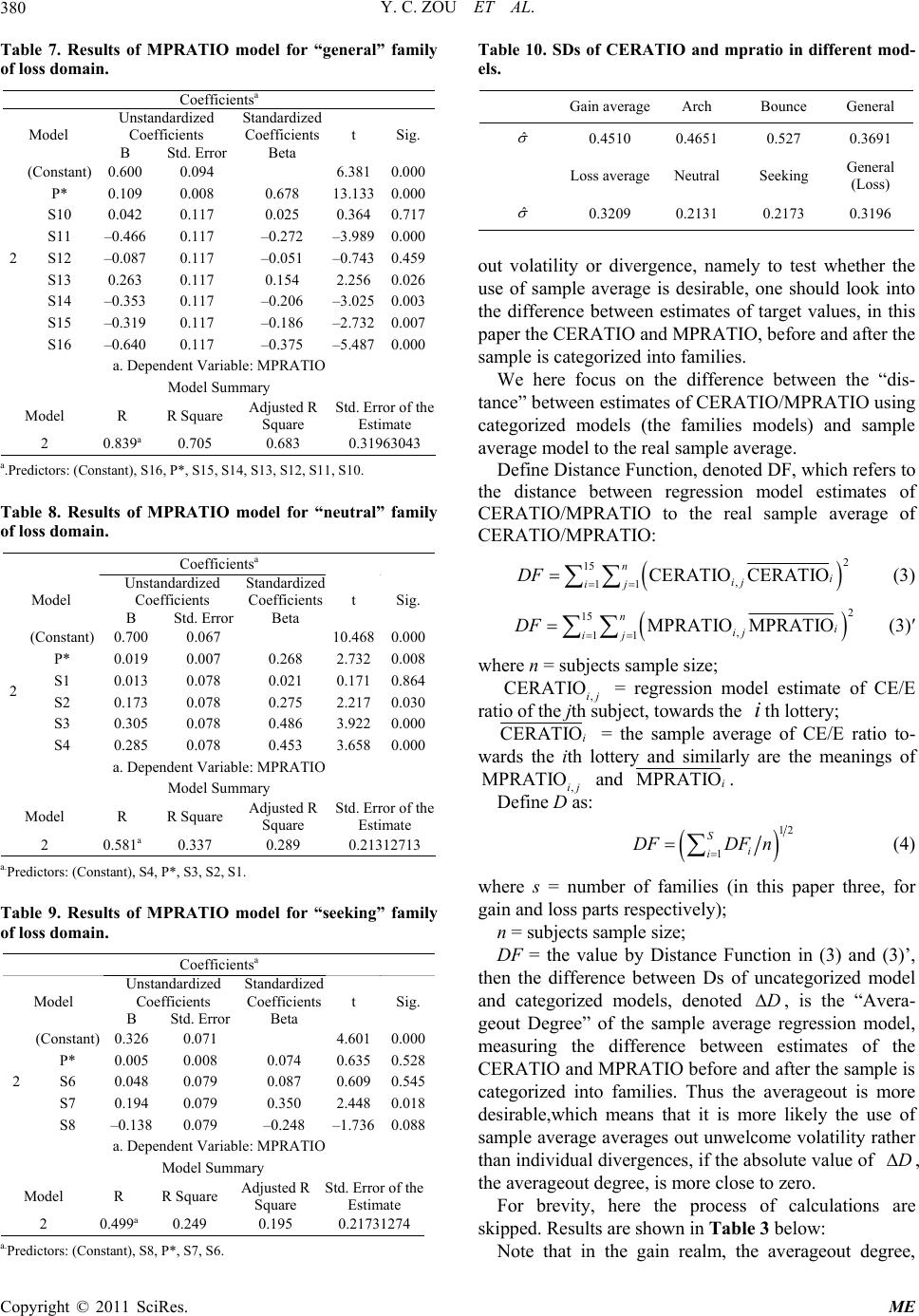

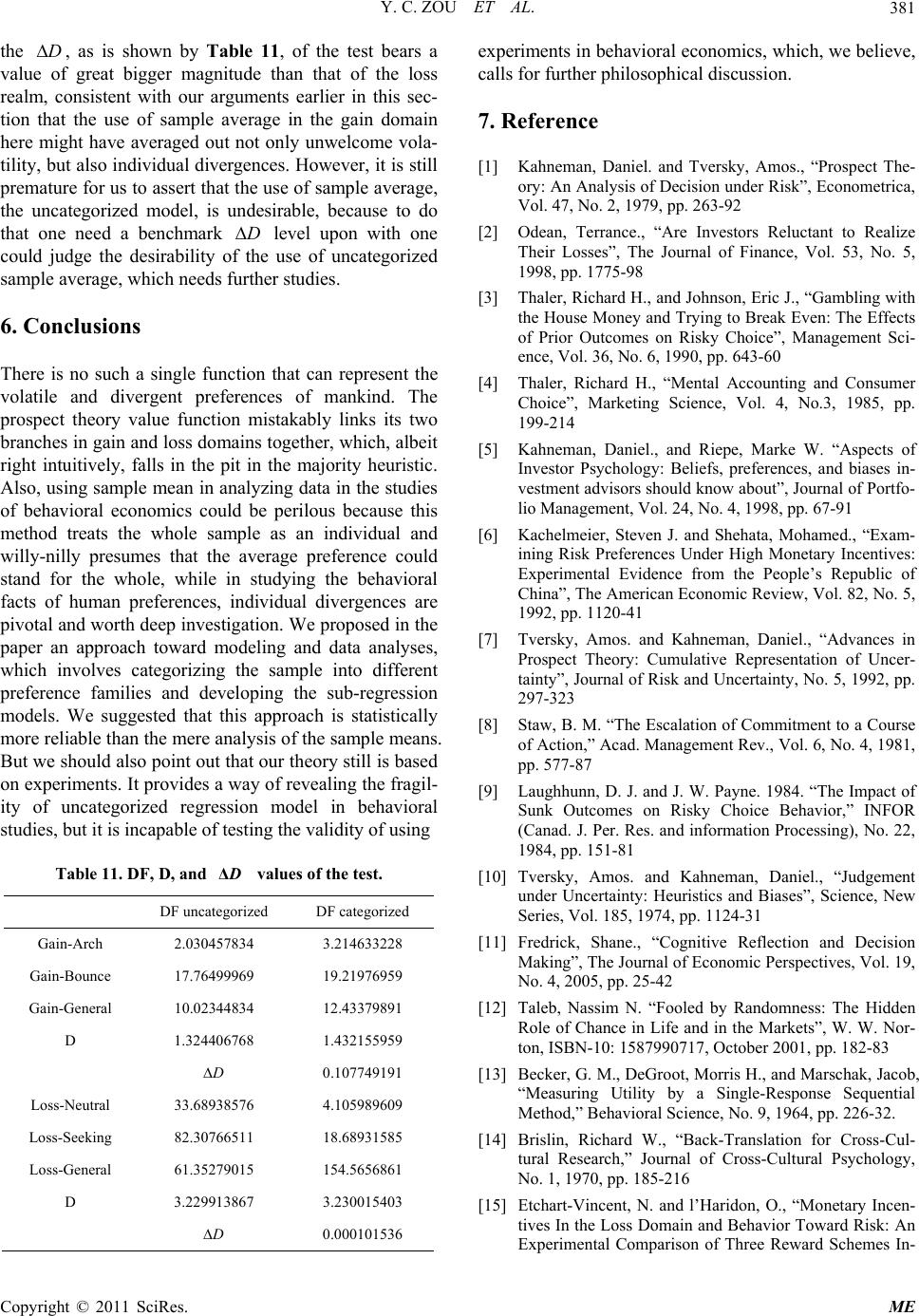

Modern Economy, 2011, 2, 371-382 doi:10.4236/me.2011.23040 Published Online July 2011 (http://www.SciRP.org/journal/me) Copyright © 2011 SciRes. ME Testing Validity of Using Sample Mean in Studies of Behavioral Facts Yongchen Zou, Runqi Hu School of Finance and St at i stics, East China Normal University, Shanghai, China E-mail: rustyzou@gmail.com, rqhu712@gmail.com Received Janarury18, 2011; revised April 15, 2011; accepted April 28, 2011 Abstract In this paper we argue that a couple of taken-for-granted methods employed in studying behavioral facts of human risk preference are mistakable. We call for within-subjects experiment design and propose a simple statistical method that might be used to test the validity of using sample mean in interpreting as well as gen- eralizing risk preferences. Keywords: Risk Preferences, Behavioral Economics, Prospect Theory, Heuristics 1. Introduction Decision making under uncertainty involves monetary decision between a certain amount of gain/loss and a gamble which gives you a certain chance to win the prize /lose the money, taking the form of “Choose between a sure gain/loss of x or a p chance to win/lose y”, where y is always of greater magnitude a number than x. An enormous amount of efforts have been invested into this field by a great many behavioral economists and psy- chologists, who produced various views and theories on the mechanics of mankind’s decision making under un- certainty. Pioneering problems of this kind were first presented by two psychologists, Daniel Kahneman and Amos Tversky [1] in their renowned work of prospect theory, revealing that people are generally loss averse and gain certainty-seeking. Challenging the Subjective Expected Utility (SEU) theory, prospect theory replaced the utility function with the S-shaped value function, probability with the weighting function. This critical step forward in economics received enormous attentions. Although theories on decision making under uncer- tainty varies, they generally share methods such as through questionnaires responses provided by agents. Despite the many insightful views on how people make decisions, little attention has been placed on the validity of methods. We find that the ways in which data is ana- lyzed in studies of this field are imperfect. The main purpose of this paper is to aware of defects lurking in the methods used in studies of decision mak- ing under uncertainty, especially the misuse of sample means, and introduce an approach of experiment data analysis. The remainder of this paper is organized as follows: Section 2 provides a review of decision making under uncertainty. Section 3 points out two major fallacies exist in the studies of this field. Section 4 presents our ex- periment on human risk preferences toward possible gains and losses and introduces a new approach in ana- lyzing data that circumvents the fallacies. Section 5 pro- poses a theory of testing validity of use of sample aver- age in deriving regression models. Section 6 is a conclu- sion. 2. Decision under Risk Precursors in studies of human decisions under risk, Kahneman and Tversky concocted series of questions, and through responds from the agents they found an in- clined pattern in which people make monetary decision under uncertainty. Typical problems presented by pros- pect theory are as follows: Problem 1: Imagine you are now $1000 richer. Choose between: A. Sure gain of $500; B. 50% chance to win $1000 Problem 2: Imagine you are now $2000 richer. Choose between: C. Sure loss of $500; D. 50% to lose $1000 For the matter that the majority of respondents chose A and D, and that A and C (as well as B and D) are in fact technically identical-namely if people choose A (B),  Y. C. ZOU ET AL. 372 they should have chosen C (D) to stay consistent in their decision — a law in human decision making seemingly obvious arises that people tend to seek certainty in gains and averse to risk when it comes to losses, as is con- cluded by prospect theory. Also, people focus on gains and losses, which means that they take the reference point of zero, or status quo, rather than concerning about the final situation they will be in. For instance, if people choose A and C, they will end up in both problem with a final situation of $1500 richer. Kahneman and Tversky (1979) replaced the utility function with what they called value function, as is plot- ted in Figure 1. Concave in the domain of gains and more steeply convex in that of losses, the function indi- cates that people are loss averse. In addition, the two psychologists plotted a non-linear weighting function, advanced in their later work (Kah- neman and Tversky, 1992), that indicating people’s dis- tortion in interpreting probability. See Figure 2. Particu- larly, Kahneman and Tversky asserted, people overesti- mate very low probability, which justifies people’s actions Figure 1. Prospect theory value function. Figure 2. Prospect theory weighting function. in gambling and buying insurance. This argument is supported by results of the following problems in their 1979 paper: Problem 3: 0.1% to win $5000 or a certain gain of $5 where most people choose the former, and Problem 4: 0.1% to lose $5000 or a sure loss of $5 where the majority favors the latter. Similar brief reviews of prospect theory value function could be found in Terrance Odean [2], Richard H. Thaler and Eric J. Johnson [3], Richard Thaler [4], Daniel Kah- neman and Mark W. Riepe [5]. The Striking of prospect theory is a tipping point where a great amount of intellectual powers are evoked and invest their time and efforts into exploring of human decision making under risk. But as prototypes, pair choices in the original paper left much to be desired: 1) vast majority of the problems used in the paper is con- cerned about monetary gains and losses. And things, when associated with money, always become more com- plicated than they are under other situations in that spe- cial parts of people’s mind will be activated by sway of human nature, such as greediness and fear of embar- rassment for winning the least (losing the most) among peers; 2) all problems in that paper is hypothetical, which means that respondents won’t actually win the prizes or suffer the losses, whatever choices they make. This could give rise to differences in decision making, thus leading to errors in statistics, as Steven J. Kachelmeier and Mo- hamed Shehata [6] proved by their experiments con- ducted in China, U.S., and Canada, which, however, Amos Tversky and Daniel Kahneman [7] asserted insuf- ficient and unnecessary; 3) a potential assumption hard to be detected in the original paper is that, it presume choice makers have “reset buttons” on their body, and after every single choice is made, respondents will press the button, reset themselves to the status quo physically and psychologically, and go on with the next question. This presumption is flawed in that in a series of decision makings, risk-taking behavior is affected by the previous choices the choice maker made. Risk-taking behavior alters when previous gains or losses are incorporated into decision making. This has been discussed by Staw [8], Laughhunn and Payne [9], Tvesky and Kahneman [10], Fredrick [11]. 3. Fallacies in Methods Although theories of decision making vary, they gener- ally share methods of experimental nature usually in- volving subjects, questionnaires, instructions, and inter- pretation of subjective responses. But economics, distin- guished from psychology, is not experimental. The idea of generalizing what is said by myopic experiment re- Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL.373 sults into a theory of distant future has itself suffered from cognitive biases. We find that discussion of ex- periments results in studies of behavioral economics were long done under a couple of major assumptions, both have much to do with the use of sample mean, which require justification. 3.1. Majority Heuristic Consider the process in which prospect theory value function is plotted: problem sets were concocted, choices were made by the subjects, and an S-shaped function was plotted in accordance with the majority’s risk preferences. What are majority’s preferences? In studies of decision making such as prospect theory, they generally refer to the options favored by most people. But we should be careful in deriving quantitative conclusion, such as the value function, because it is constituted with two parts of gain and loss domains. We argue that the intuitively natural approach of connecting two branches up needs reconsideration. To illustrate the issue, we suppose the following two problems and the results of them, mimicking the birth of value function. Note that the case is intensely simplified. Problem 7. Imagine you are now $2000 richer. Choose between: A. Sure gain of $500; B. 50% chance to win $1000 [70]* [30] Problem 8: Imagine you are now $3000 richer. Choose between: C. Sure loss of $500; D. 50% to lose $1000 [35] [65]* Assume that 100 subjects are involved in this study. Note that the numbers in parentheses indicate the per- centage of the subjects’ responses (e.g. of the re- spondents choose A over B). Now responses of Problem 7 shows a sign of risk aversion, while those of Problem 8 indicates loss aversion. A function concave in the do- main of gains and convex in the domain of losses is therefore produced, as is shown in Figure 1, representing the preference of the majority. 70% Here the fallacy emerges. It has long been overconfi- dently assumed that those who constitute the majority in Problem 7 stay the majority in Problem 8. That is, ex- perimenters mistakingly think that most, if not all, of the 70 subjects who chose in Problem 7 chose in Problem 8, which is obviously erroneous for there exists intersection in choices among different options. It is rea- sonable to call this logic fallacy majority heuristic, and somehow evade cognitive guard. A D Consider an extreme case of the responses of Problem 7 and 8: of the 70 subjects who chose in Problem 7, only 35 D in Problem 8; and all 30 subjects who chose B in Problem 7 favored D in Problem 8. This means that the majority in Problem 8 is constituted by 35 MAJOR subjects and 30 MINOR subjects in Problem 7 whose responses were against the “trend”. Similarly, of 70 sub- jects who chose A, 35 of them had chose C in Problem 8. A We maintain that studies in this field could change for the better if results are interpreted in an innovative and more statistically reliable way such that choices made are documented, rather than marginally, in an integrate way. For instance, of a problem set constituted by Problem 7 and Problem 8, instead of merely recording the percent- ages of subjects who chose A, B, C, and D, more precise preferences of every individual are documented as the percentages of subjects choosing AC, AD, BC and BD. Note that in the extreme case mentioned, the percentages were 35% for AD, 35% for AC, 30% for BD, and 0% for BC. To prove that the majority heuristic matters, we draw four typical problems (see Appendix) in the Kahneman and Tversky’s 1979 paper and replicated the experiment in which 32 subjects are involved. Rather than merely analyzing the average preference, we recorded the result individually, and compare each of them to the average outcome. Percentages in the parentheses shows the ratio of num- ber of subject who made the corresponding choice to the sample size. Note that prospect theory value function indicates two preferences of human decision making, namely risk averse in the domain of gains and risk seeking in losses. We note them R.A. in gains and R.S. in losses respec- tively. Now subjects are said to be R.A. in gains if they choose B in both PROB1 and PROB3, and R.S. in losses if A are preferred in both PROB2 and PROB4. Define a trend as existing if more than 50% of the subjects have it. A perfect subject whose preference is consistent with that is predicted by prospect theory will answer “B A B A” in the two pair of problems. Table 1 tabulates the result of this replication experi- ment. We first draw an average trend of the result by counting how many people chose A in the four questions and then divide the numbers by the sample size. It turns out that, as can be seen in the table, in the first pair of problems, nearly 43.8% subjects chose A in PROB1, which means 55.2% chose B, and 53% subjects chose A in PROB2. Thus the average trend is “B A”, indicating R.A. in gains and R.S. in losses. In the second pair of problems, 81.3% answered B in PROB3, and 40.6% an- swered A in PROB4. This, then, represents an average trend of “B B”, being R.A. in both gains and losses do- mains (note that this is a trend slightly disagree with prospect theory’s prediction). If we just look at the average trends, we see at least Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL. 374 Table 1. Result of a replication experiment of four prospect theory problems. Subject PROB1 PROB2 PROB3 PROB4 1 B A B A 2 A B B A 3 B A B B 4 B B B B 5 B A B B 6 A A B A 7 A A B A 8 B A B B 9 A A B B 10 A B B B 11 A B A B 12 A B A B 13 A A B B 14 B B A B 15 B A B A 16 B A B A 17 B B A A 18 B B B A 19 B B B A 20 B A B A 21 B B B B 22 A A B B 23 B B B B 24 A B B B 25 B A B A 26 A A B B 27 A A A B 28 A B B B 29 B B B B 30 B A A B 31 A B B A 32 B A B A Choose A 14 [43.75%] 17 [53.13%] 6 [18.75%] 13 [40.63%] Choose BA 10 [31.25%] 12 [37.5%] Choose BA,BA 6 [18.75%] one of them is consistent with S-shaped value function, and one might argue that if the sample size (or the num- ber of questions) expands, prospect theory prediction could be proved right. However, if the result of this rep- lication experiment is interpreted in a different way, the conclusion would be widely contradicting. Instead of calculating an average answer, we now look at within-subjects, or integrate, results by checking how many subjects answered “B A” in both pair of questions, and recall that “B A” indicates a preference of R. A. in gains and R.S. in losses. As is shown in Table 1, only 31.3% and 37.5% of subjects answered “B A” in the pairs of questions respectively, a result far cry in indi- cating the trend of R.A. in gains and R.S. in losses. And the majority heuristic is proved existing here because although the average result shows a trend of R.A. and R.S. in the first pair of questions, it is actually supported by only 31.3% of the subjects. Remarkably, this paradox becomes more irony when we try to find “perfect subject” who answered “B A B A”: there are only six of them, namely 18.8% of the sample. If a trend is buttressed by no more than 20% of the subjects, it can never be called a trend. We argue that the majority heuristic has taught us a paradoxical lesson that, people might be risk averse in gains; people might be risk seeking in losses; but it would be erroneous to assert that people are risk averse in gains and risk seeking in losses. As a matter of fact, we are to show in section III that even in the domains of gains and losses respectively, human preferences cannot be simply generalized as risk averse or risk seeking. We should however point out that intersection of pref- erences doesn’t happen all the time. Think of another two problems and a pair of possible results: Problem 9. Choose between: A. Sure gain of $500; B. 50% chance to win $1000 [70]* [30] Problem 10: Choose between: C. Sure gain of $600; D. 50% chance to win $1,000 [75]* [25] It is reasonable in this case to predict that all those who chose A in the former problem favored C in the lat- ter — no intersection happens. We speculate two pairs of principles in human preferences here. Suppose A and B are two outcomes, a positive amount, and p a prob- ability that 0p1 , then a) If A is preferred to pB, A is preferred to pB; but A is not necessarily preferred to BpP ; b) If pB is preferred to A, Bp is preferred to A; but Bp is not necessarily preferred to Ap . This indicates that an increment of benefit on the op- tion favored would firm up the chooser’s preference, Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL.375 while increments on both sides don’t. 3.2. Misuse of Sample Mean Studies that use statistical methods require appropriate understanding of statistics used. When we require sub- jective certainty equivalents for lotteries out of subjects, we must make sure that the subjects understand what mathematical expectation is because it would be unfair otherwise to use the statistic that subjects don’t under- stand later as a criterion testing subjects’ preferences. More importantly, we should sure that we experimenters ourselves fully understand the statistics we are using. However, there exists the logic leap from existence of statistic to apprehension of statistic. Just the fact that the statistics are invented doesn’t mean they could be fully understood. Typical example here is, we are of the opin- ion, the basic and long been misused statistic of average. Average, arithmetic or compound, is a basic statistic that is used everywhere as a estimator of general stan- dard. Broadly as it has long been used, human mind could hardly grasp what an average really is. When it is said that Class A bares an average score of 75 in a mid-term examination, it is interpreted immediately by human mind, or at least System 1, that almost every stu- dent in Class A got test results in the neighborhood of 75, which is obviously erroneous. And when the second news came that Class B has an average score of 82, again it is translated into a statement that almost every student in Class B got a better score than students in Class A. Ludicrous as it may sound, and despite almost everyone would deny these kinds of thoughts had ever come to them and they really understand what is an average, the very logical fallacy is repeated frequently in studies of human preferences, especially in those which experi- ments involving subjects are conducted. The common use of average is like this: conduct the experiment to the subjects, have their responses docu- mented, average the answers and analyze the average answer as a supposed individual who represents the whole sample. The basic idea of using average is to av- erage out unwelcome volatility and thus get a general trend. But this could be perilous in studying behavioral facts of human preferences, for in these kinds of studies, what we need is exactly the opposite: human preferences, such as risk preferences, are very volatile, to say nothing of the fact that an individual’s preference vary under arbitrary situations. And this very divergence in prefer- ences is exactly what worth investigating. This is not to say average should be abandoned in preferences analysis. As a matter of fact, one can never avoid using it because it would be invalid and unnecessary to focus on every individual. However, we can revise the sample mean method by dividing the whole sample into groups with obviously different characteristics, thus saving these di- vergences from being willy-nilly averaged out. We are to employ this method into our experiment in Part III. Failure of human minds’ apprehension of other statis- tics, such as expected value are entertainingly discussed by Taleb [12], where he asked readers to imagine a com- bination of pleasure of a vacation that will happen 85% in Paris and 15% in Caribbean. In fact, he asserted, that “[our] brain can properly handle one and only one state at once — unless [you] have personality troubles of a deeply pathological nature”. 4. Risk Preference Families So far we have shown that the linkage of the two branches of the value function and the use of total aver- age in studying human preferences are mistakable. And we claimed in Section II that not only risk preferences should be studied separately in gain and loss domain, even in the domains of gain or loss per se, they cannot be simply generalized as “risk averse” or “risk seeking”. Our experiment following is to test the different risk preferences under gambles of different prize level. 4.1. The Experiment and Results The process employed a two-stage method proved unbi- ased by Becker et al. [13]. But rather than eliciting sub- jective certainty equivalents under different probability to win, we require certainty equivalents under different prizes and losses at a same probability 50%. Prizes and losses provided in the experiment ranged from 2 to 1000000 (2, 6, 10, 15, 25, 30, 50, 100, 200, 400, 750, 1000, 5000, 100000, 1000000). The experimental in- structions are written in English. We assume this to be a semi-“back translation” (a concept put forward by Brislin [14]) for we, the designers, are Chinese). The reason why we didn’t divide the probability into smaller minor unity is that we fear that gradual increases in probability make people confused and thus inducing mindless answers. We assume that people get vague idea about the difference between chances of 30% and 40%, but they surely feel different among a half chance to win, less than a half to win, and more than a half to win. Hence we choose 50% as our constant probability, pre- suming that our subjects stay cognitively conscious dur- ing the test. Note that all subjects are students major in either sta- tistics, actuarial science, risk management, or financial engineering, hence it is reasonable to assume than they know quite well the concept of mathematical expectation, justifying our using it later as a criterion in discussing Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL. 376 risk preferences. To rule out the majority heuristic and the misuse of total average discussed in Part II, we employ a different method in interpreting the results. Risk preferences to- ward possible gains and losses are discussed separately. We are to show the risk preferences of gain domain and those of loss domain, but we don’t and cannot provide a single type of risk preference that summarizes the whole picture. We avoid believing in average of the total. Rather, responses are categorized, according to their characteristics, into groups. In fact, we intuitively ex- pected, rather than predicting, a general but nothing spe- cific trend before we get the results: respondents may show a tendency toward risk seeking when the possible prizes/losses are small, and they may tend to be risk averse when the possible prizes/losses surge to certain higher levels. However, we didn’t plan to derive the general trend which represents the average (and we don’t believe any single one could represents all); instead, we focus on detecting different patterns of risk preferences among subjects. We even tried to analyze anomalies among the results and explain why they are like that. Defects in our experiment is that it provided no real money rewards. Since we are trying to elicit subjects’ preference under big prize, we cannot afford to actually pay them what they won (For experiment that involving real subjects losses, see Etchart-Vincent and l’Haridon [15]). But they are informed that rewards are to be paid according to their final results. Subjects are urged to be- have as if the gambles are real and independent throughout the experiment. We used in the gain domain the ratio of certainty equivalent to expected value, or CE/E, as major criterion of subjects risk preferences. If CE/E of a single response exceeds unity, the subject is said to show a sign of risk seeking toward the gamble, while if CE/E is lower than one, it signals risk averse. In the loss domain, on the other hand, the ratio of maximum premium (which means that the maximum certain quantity the subject is willing to pay to eliminate the risk of suffering potential loss) to expected value, or MP/E, is used so that if MP/E of a response toward a gamble exceeds one, it shows risk averse, and if MP/E is less than one, it shows risk seeking. For example, if the subject is extremely risk seeking toward a potential loss, then she is not willing to pay even a penny to an insurer to have her asset underwritten. In this case, the maximum premium will be 0, thus MP/E is equal to 0. For the purpose of illustrating the misuse of total av- erage that has been discussed in Part II, Figure 3 mani- fests the total average CE/E and MP/E values under the prize/loss series toward gains and losses respectively. It seems obvious, from the graphs, that there is a trend of decreasing CE/E ratio and increasing MP/E ratio. What’s Figure 3. Total average of CE/E ratio and MP/E ratio. more, average CE/E ratio of our experiment rarely ex- ceeds unity conspicuously and so does MP/E ratio. This indicates that except for extremely small prizes (such as 50% to win 2) and extremely big losses (such as 50% to lose 1000000), respondents show preferences of risk averse in gain domain and risk seeking in loss domain, consistent with what is told by prospect theory and its value function. We categorized according to their features the final results of gain domain and loss domain respectively into three families. As is shown by Figure 4 some typical individual responses, these categories are named “Gen- eral”, “Arch”, and “Bounce” in gains, and “General”, “Neutral” and “Seeking” in the losses. Do notice that these results are not paired with each other and must be viewed separately, which means that, for instance, a subject in “General” family of gain domain can either be in “General”, “Neutral” or “Seeking” in the loss part. The first three captures of Figure 4 manifests three preference families that we detected from the subjects in questions involving possible gains. “General” family shows a preference pattern that fits the majority of the respondents, in which agents show risk seeking toward relatively small prizes, and they gradually become risk averse as the prize become more and more attractive. Note that although “General”, like the total average CE/E, decreases as the prize level sour, the line does not fall below unity until the prize level reaches somewhere around 200, whereas the total average CE/E rarely sur- passes one. Respondents in “Arch” family typically start from strict risk averse, then becomes increasingly risk seeking, but when the prize level seems attractive enough to them, they show a sign of risk averse again. The CE/E Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL. Copyright © 2011 SciRes. ME 377 Figure 4. Categorizing of final results in gain and loss domains.(1.General) line of this family crosses the unity twice. Subjects in “Bounce” family, albeit not large in number, shows an interesting and sharp risk preference reversal when the prize level gets extremely high, before which they gener- ally share risk preferences with those in “General” family. The last three captures, on the other hand, shows the three risk preference families of the loss domain. Agents in “General (Loss)” family are shown to have increasing MP/E ratio as the loss level approaches extreme. But note that MP/E values of a typical respondent in “Gen- eral (Loss)” family exceeds unity when the possible loss level reaches 200 or so, while in total average ratios, MP/E only goes beyond 1 when the possible loss be- comes astronomical. “Neutral” family possesses MP/E ratio hovering around one whatever the possible loss would be. Finally, subjects in “Seeking” family have MP/E ratio always below unity; they are always risk seeking, tending to run the risk of losing. Counterintuitive finding of our experiment is that risk preferences of gain and loss domains barely cross paths. For example, not a single one of the subjects showed a sign of risk neutral in gains part, and no one in losses part presented a sudden preference reversal as is in “Bounce” family. We find that subjects behaved sharply different toward risks of certain gains and losses, and their psychologies, influenced by various factors, varied individually and were very volatile. We interviewed after the experiment some of the sub- jects and asked for what were their psychologies when providing answers. To our surprise, every subject inter- viewed gave exactly the same reason justifying their subjective certainty equivalent toward small prized and losses (such as a 50% to win/lose 2), which goes like: The possible gains/losses are so small that I don’t care if I win or lose them. But their explanations diverse. For those who have CE/E ratio of 2 or bigger toward possible gain, their explanations were typically “I don’t care about the little gain so that I just gamble. Either win or not win, no big deal”; for those who have CE/E ratio of smaller value, their justifications were like “I don’t care the winning of the little amount of money”. In the loss part, none of the subjects has high MP/E ratio toward small possible loss; they chorused a preference of risk seeking, with MP/E ratios ranging from 0 to 1. Similarly, they asserted in the aftermath interview that they “an- swered so because they didn’t care about the small  Y. C. ZOU ET AL. 378 losses”. Rationally speaking, if subjects “don’t care” whether they gamble or not, namely they think them- selves indifferent between gambling or not gambling, that should be interpreted as risk neutral thus their sub- jective certainty equivalent should be equal to the mathematical expectation, entailing a CE/E or MP/E ratio of 1. However, the data just showed that behavior of most subjects wasn’t consistent with this rationality. Thus we have reason to doubt that when CE/E or MP/E ratio does equal to unity, that doesn’t necessarily mean the subjects are risk neutral toward the gamble. The sudden CE/E ratio bounce back of subjects in “Bounce” family reflects gambler’s psychology. When respondents in the family were asked why they suddenly wanted to take risk in the high prize gamble, they typi- cally answer that when the prize level became extremely high, the lottery turns into a gamble. And a gamble is a gamble, either one win the big, or walk away with noth- ing. Most subjects in “Neutral” family of loss domain said they feel horrible on the thought of losing their money, be it the premium they pay or the money they lose if they choose to gamble. Rather than endless dithery, they sim- ply chose to stay indifferent: write down certainty equivalents entered around mathematical expectations, and whatever happens is destiny. Agents in “Seeking” family of loss domain usually assert that they would rather run the risk of losing the gamble than paying anything to eradicate the risk, so that their fortunes still have a good 50% chance to stay intact. Although we highly doubt that this kind of psychology is resulted partly from the fact that the possible losses in the experiment are hypothetical. 4.2. Models Kachelmeier and Shehata (1992) introduced a linear re- gression model that includes subject effects, incorporat- ing correlated errors entailed by individual differences in risk preferences. Our models bases essentially on the Kachelmeier and Shehata’s CERATIO model but a) we ignore the percent effects for lotteries in our experiment share the constant winning/losing chance of 50%, b) we used logarithm of prizes/losses in the model and c) we introduce a similar MPRATIO model for MP/E ratios with logarithm of prize factor replaced by logarithm of loss. Our regression models are shown as followed: 1 1 2 1 CERATIOlog Prize n jj jSubject (1) ** 1* 2 1 CERATIOlogLoss i n jj jSubject (2) where CERATIO and MPRATIO respectively means ratio of certainty equivalent to expected value and ratio of maximum premium to expected value; and * are intercepts of regressions; log(Prize) and log(Loss) are logarithm of Prizes and Losses series in the lotteries; j Su n bject refers to subjects factor, which equals 1 if the observation is from the j th observation, –1 if from the th observation, and 0 otherwise; is the disturbance. The regression coefficients and the results of tests are tabulated as follows. Where CONSTANT= the intercept parameter; i S * p = the j th subject = logarithm of Prize Advantage of categorizing risk preference into fami- lies, and thus deriving the categorized regression models, could be observed first in terms of the increase in both R square, namely the goodness of fit, and adjusted R square in both “General” families of gain and loss parts as is shown by Table 3 and Table 7, compared to that of the sample average data in Table 2 and Table 6. R square increases from 0.433 in sample average to 0.758 in “General” family of gain domain, and from 0.784 in sample average to 0.839 in “General” family of loss do- main. And the corresponding adjusted R square as well increase from 0.392 to 0.533 and from 0.586 to 0.683 respectively. Besides, estimates derived by OLS tech- nique in CERATIO and MPRATIO model show statisti- cal significance by and large, as can be seen particularly in Table 3, Table 5, Table 7, and Table 8. Table 4 and Table 9, corresponding to “Arch” family of Gain Do- main and “Seeking” Family of Loss Domain, show in- significance in estimates of parameters; we attribute this insignificance to the small sample size, and it can be that they are not representative to the population. Second, in most families, the variances of estimates of both CERATIO and MPRATIO drop from original vari- ances of estimates of CERATIO and MPRATIO in sam- ple average regression models, indicating better stability. See Table 10. 5. “D” for Testing Validity of Sample Average It is mentioned without evidence in Sec II.C that the use of total average in analyzing behavioral facts of human preferences is mistakable for it averages out not only unwelcome volatility of the data but also the divergence between subjects preferences which worth investigating. This is observable from Figure 3 and Figure 4, espe- cially in the gain part, for the three risk preference fami- lies, “General”, “Arch”, and “Bounce”, viz., of gain do- main bear sharply different shaped CE/E lines. To test whether the use of sample average averages Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL.379 Table 2. Results of CERATIO model for sample average of gain domain. Unstandardized Coefficients Standardized Coefficients Model B Std. ErrorBeta t Sig. (Constant) 1.240 0.124 9.974 0.000 P* –0.056 0.008 –0.341 –6.9700.000 S1 0.233 0.165 0.095 1.4170.158 S2 0.143 0.165 0.058 0.8700.385 S3 –0.118 0.165 –0.048 –0.7170.474 S4 0.236 0.165 0.096 1.4330.153 S5 0.599 0.165 0.244 3.6390.000 S6 0.126 0.165 0.051 0.7650.445 S7 –0.837 0.165 –0.341 –5.0800.000 S8 –0.051 0.165 –0.021 –0.3120.755 S9 0.037 0.165 0.015 0.2240.823 S10 0.256 0.165 0.104 1.5520.122 S11 0.210 0.165 0.085 1.2730.204 S12 0.037 0.165 0.015 0.2250.822 S13 0.399 0.165 0.163 2.4220.016 S14 –0.491 0.165 –0.200 –2.9810.003 S15 0.358 0.165 0.146 2.1740.031 1 S16 0.189 0.165 0.077 1.1460.253 a. Dependent Variable: CERATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 1 0.658a 0.433 0.392 0.4510 a.Predictors: (Constant), S16, P*, S5, S2, S1, S4, S3, S8, S7, S6, S9, S10, S12, S11, S13, S14, S15. Table 3. Results of CERATIO model for “general” family of gain domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. ErrorBeta t Sig. (Constant) 1.435 0.106 13.537 0.000 P* –0.092 0.009 –0.601 –10.7 32 0.000 S8 –0.051 0.135 –0.029 –0.38 2 0.703 S9 0.037 0.135 0.021 0.2740.784 S10 0.256 0.135 0.142 1.8960.060 S11 0.210 0.135 0.117 1.5560.122 S12 0.037 0.135 0.021 0.2750.784 S13 0.399 0.135 0.222 2.9600.004 S14 –0.491 0.135 –0.274 –3.64 3 0.000 S15 0.358 0.135 0.200 2.6570.009 1 S16 0.189 0.135 0.105 1.4000.164 a. Dependent Variable: CERATIO Model Summary Model R R SquareAdjusted R Square Std. Error of the Estimate 1 0.751a 0.564 0.533 0.3691 a.Predictors: (Constant), S16, P*, S15, S14, S13, S12, S11, S10, S9, S8. Table 4. Results of CERATIO model for “arch” family of gain domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. Error Beta t Sig. (Constant) 1.2460.152 8.216 0.000 P* –0.0130.017 –0.101 –0.7880.434 S1 –0.0030.170 –0.002 –0.0160.988 S2 –0.0930.170 –0.085 –0.5460.588 1 S3 –0.3540.170 –0.326 –20.0840.042 a. Dependent Variable: CERATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 1 0.323a 0.104 0.039 0.46513940 a.Predictors: (Constant), S3, P*, S2, S1. Table 5. Results of CERATIO model for “bounce” family of gain domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. Error Beta t Sig. (Constant) 0.0610.182 0.333 0.741 P* 0.0070.022 0.033 0.3250.747 S5 10.4360.193 0.866 7.4560.000 1 S6 0.9630.193 0.580 4.9980.000 a. Dependent Variable: CERATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 1 0.765a 0.585 0.555 0.527 a.Predictors: (Constant), S6, P*, S5. Table 6. Results of MPRATIO model for sample average of loss domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. Error Beta t Sig. (Constant) 0.8750.088 9.895 0.000 S1 –0.3740.117 –0.177 –3.1880.002 S2 –0.2140.117 –0.101 –1.8290.069 S3 –0.0820.117 –0.039 –0.6970.486 S4 –0.1020.117 –0.048 –0.8720.384 S5 –0.3870.117 –0.183 –3.3020.001 S6 –0.7880.117 –0.372 –6.7270.000 S7 –0.6420.117 –0.304 –5.4820.000 S8 –0.9740.117 –0.460 –8.3160.000 S9 –0.8370.117 –0.395 –7.1400.000 S10 0.0420.117 0.020 0.3620.718 S11 –0.4660.117 –0.220 –3.9730.000 S12 –0.0870.117 –0.041 –0.7400.460 S13 0.2630.117 0.124 2.2470.026 S14 –0.3530.117 –0.167 –3.0130.003 S15 –0.3190.117 –0.151 –2.7210.007 S16 –0.6400.117 –0.303 –5.4650.000 2 P* 0.0580.006 0.410 10.1660.000 a. Dependent Variable: MPRATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 2 0.784a 0.614 0.586 0.32091842 a.Predictors: (Constant), P*, S16, S5, S2, S1, S4, S3, S8, S7, S6, S9, S10, S12, S11, S13, S14, S15. Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL. 380 Table 7. Results of MPRATIO model for “general” family of loss domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. ErrorBeta t Sig. (Constant) 0.600 0.094 6.381 0.000 P* 0.109 0.008 0.678 13.1330.000 S10 0.042 0.117 0.025 0.3640.717 S11 –0.466 0.117 –0.272 –3.9890.000 S12 –0.087 0.117 –0.051 –0.7430.459 S13 0.263 0.117 0.154 2.2560.026 S14 –0.353 0.117 –0.206 –3.0250.003 S15 –0.319 0.117 –0.186 –2.7320.007 2 S16 –0.640 0.117 –0.375 –5.4870.000 a. Dependent Variable: MPRATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 2 0.839a 0.705 0.683 0.31963043 a.Predictors: (Constant), S16, P*, S15, S14, S13, S12, S11, S10. Table 8. Results of MPRATIO model for “neutral” family of loss domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. ErrorBeta t Sig. (Constant) 0.700 0.067 10.468 0.000 P* 0.019 0.007 0.268 2.7320.008 S1 0.013 0.078 0.021 0.1710.864 S2 0.173 0.078 0.275 2.2170.030 S3 0.305 0.078 0.486 3.9220.000 2 S4 0.285 0.078 0.453 3.6580.000 a. Dependent Variable: MPRATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 2 0.581a 0.337 0.289 0.21312713 a.Predictors: (Constant), S4, P*, S3, S2, S1. Table 9. Results of MPRATIO model for “seeking” family of loss domain. Coefficientsa Unstandardized Coefficients Standardized Coefficients Model B Std. ErrorBeta t Sig. (Constant) 0.326 0.071 4.601 0.000 P* 0.005 0.008 0.074 0.6350.528 S6 0.048 0.079 0.087 0.6090.545 S7 0.194 0.079 0.350 2.4480.018 2 S8 –0.138 0.079 –0.248 –1.7360.088 a. Dependent Variable: MPRATIO Model Summary Model R R Square Adjusted R Square Std. Error of the Estimate 2 0.499a 0.249 0.195 0.21731274 a.Predictors: (Constant), S8, P*, S7, S6. Table 10. SDs of CERATIO and mpratio in different mod- els. Gain averageArch Bounce General ˆ 0.4510 0.4651 0.527 0.3691 Loss averageNeutral Seeking General (Loss) ˆ 0.3209 0.2131 0.2173 0.3196 out volatility or divergence, namely to test whether the use of sample average is desirable, one should look into the difference between estimates of target values, in this paper the CERATIO and MPRATIO, before and after the sample is categorized into families. We here focus on the difference between the “dis- tance” between estimates of CERATIO/MPRATIO using categorized models (the families models) and sample average model to the real sample average. Define Distance Function, denoted DF, which refers to the distance between regression model estimates of CERATIO/MPRATIO to the real sample average of CERATIO/MPRATIO: 2 15 , 11 CERATIO CERATIO ni ij ij DF (3) 15 , 11 MPRATIO MPRATIO ni ij ij DF 2 (3)′ where n = subjects sample size; , = regression model estimate of CE/E ratio of the jth subject, towards the th lottery; CERATIOij i CERATIO MPRATIOij i = the sample average of CE/E ratio to- wards the ith lottery and similarly are the meanings of and ,MPRATIOi. Define D as: 12 1 S i i DFDF n (4) where s = number of families (in this paper three, for gain and loss parts respectively); n = subjects sample size; DF = the value by Distance Function in (3) and (3)’, then the difference between Ds of uncategorized model and categorized models, denoted , is the “Avera- geout Degree” of the sample average regression model, measuring the difference between estimates of the CERATIO and MPRATIO before and after the sample is categorized into families. Thus the averageout is more desirable,which means that it is more likely the use of sample average averages out unwelcome volatility rather than individual divergences, if the absolute value of D D , the averageout degree, is more close to zero. For brevity, here the process of calculations are skipped. Results are shown in Table 3 below: Note that in the gain realm, the averageout degree, Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL.381 the , as is shown by Table 11, of the test bears a value of great bigger magnitude than that of the loss realm, consistent with our arguments earlier in this sec- tion that the use of sample average in the gain domain here might have averaged out not only unwelcome vola- tility, but also individual divergences. However, it is still premature for us to assert that the use of sample average, the uncategorized model, is undesirable, because to do that one need a benchmark D D level upon with one could judge the desirability of the use of uncategorized sample average, which needs further studies. 6. Conclusions There is no such a single function that can represent the volatile and divergent preferences of mankind. The prospect theory value function mistakably links its two branches in gain and loss domains together, which, albeit right intuitively, falls in the pit in the majority heuristic. Also, using sample mean in analyzing data in the studies of behavioral economics could be perilous because this method treats the whole sample as an individual and willy-nilly presumes that the average preference could stand for the whole, while in studying the behavioral facts of human preferences, individual divergences are pivotal and worth deep investigation. We proposed in the paper an approach toward modeling and data analyses, which involves categorizing the sample into different preference families and developing the sub-regression models. We suggested that this approach is statistically more reliable than the mere analysis of the sample means. But we should also point out that our theory still is based on experiments. It provides a way of revealing the fragil- ity of uncategorized regression model in behavioral studies, but it is incapable of testing the validity of using Table 11. DF, D, and Δ D values of the test. DF uncategorized DF categorized Gain-Arch 2.030457834 3.214633228 Gain-Bounce 17.76499969 19.21976959 Gain-General 10.02344834 12.43379891 D 1.324406768 1.432155959 D 0.107749191 Loss-Neutral 33.68938576 4.105989609 Loss-Seeking 82.30766511 18.68931585 Loss-General 61.35279015 154.5656861 D 3.229913867 3.230015403 D 0.000101536 experiments in behavioral economics, which, we believe, calls for further philosophical discussion. 7. Reference [1] Kahneman, Daniel. and Tversky, Amos., “Prospect The- ory: An Analysis of Decision under Risk”, Econometrica, Vol. 47, No. 2, 1979, pp. 263-92 [2] Odean, Terrance., “Are Investors Reluctant to Realize Their Losses”, The Journal of Finance, Vol. 53, No. 5, 1998, pp. 1775-98 [3] Thaler, Richard H., and Johnson, Eric J., “Gambling with the House Money and Trying to Break Even: The Effects of Prior Outcomes on Risky Choice”, Management Sci- ence, Vol. 36, No. 6, 1990, pp. 643-60 [4] Thaler, Richard H., “Mental Accounting and Consumer Choice”, Marketing Science, Vol. 4, No.3, 1985, pp. 199-214 [5] Kahneman, Daniel., and Riepe, Marke W. “Aspects of Investor Psychology: Beliefs, preferences, and biases in- vestment advisors should know about”, Journal of Portfo- lio Management, Vol. 24, No. 4, 1998, pp. 67-91 [6] Kachelmeier, Steven J. and Shehata, Mohamed., “Exam- ining Risk Preferences Under High Monetary Incentives: Experimental Evidence from the People’s Republic of China”, The American Economic Review, Vol. 82, No. 5, 1992, pp. 1120-41 [7] Tversky, Amos. and Kahneman, Daniel., “Advances in Prospect Theory: Cumulative Representation of Uncer- tainty”, Journal of Risk and Uncertainty, No. 5, 1992, pp. 297-323 [8] Staw, B. M. “The Escalation of Commitment to a Course of Action,” Acad. Management Rev., Vol. 6, No. 4, 1981, pp. 577-87 [9] Laughhunn, D. J. and J. W. Payne. 1984. “The Impact of Sunk Outcomes on Risky Choice Behavior,” INFOR (Canad. J. Per. Res. and information Processing), No. 22, 1984, pp. 151-81 [10] Tversky, Amos. and Kahneman, Daniel., “Judgement under Uncertainty: Heuristics and Biases”, Science, New Series, Vol. 185, 1974, pp. 1124-31 [11] Fredrick, Shane., “Cognitive Reflection and Decision Making”, The Journal of Economic Perspectives, Vol. 19, No. 4, 2005, pp. 25-42 [12] Taleb, Nassim N. “Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets”, W. W. Nor- ton, ISBN-10: 1587990717, October 2001, pp. 182-83 [13] Becker, G. M., DeGroot, Morris H., and Marschak, Jacob, “Measuring Utility by a Single-Response Sequential Method,” Behavioral Science, No. 9, 1964, pp. 226-32. [14] Brislin, Richard W., “Back-Translation for Cross-Cul- tural Research,” Journal of Cross-Cultural Psychology, No. 1, 1970, pp. 185-216 [15] Etchart-Vincent, N. and l’Haridon, O., “Monetary Incen- tives In the Loss Domain and Behavior Toward Risk: An Experimental Comparison of Three Reward Schemes In- Copyright © 2011 SciRes. ME  Y. C. ZOU ET AL. Copyright © 2011 SciRes. ME 382 cluding Real Losses”, Journal of Risk and Uncertainty, No. 42, 2011, pp. 61-83 Appendix: Replication Experiment of Pros- pect Theory Problems PROB1: In addition to whatever you own, you have been given 1,000. You are now asked to choose between A: 50% chance to win 1,000 B: a sure gain of 500 PROB2: In addition to whatever you own, you have been given 2,000. You are now asked to choose between A: 50% chance to lose 1,000 B: a sure loss of 500 PROB3: Choose between: A: 25% to win 6,000 B: 25% to win 2,000 and another 25% to win 4,000 PROB4: Choose between: A: 25% to lose 6,000 B: 25% to win 2,000 and another 25% to lose 4,000 |