M. KALTALIOGLU ET AL.

Copyright © 2011 SciRes. ME

75

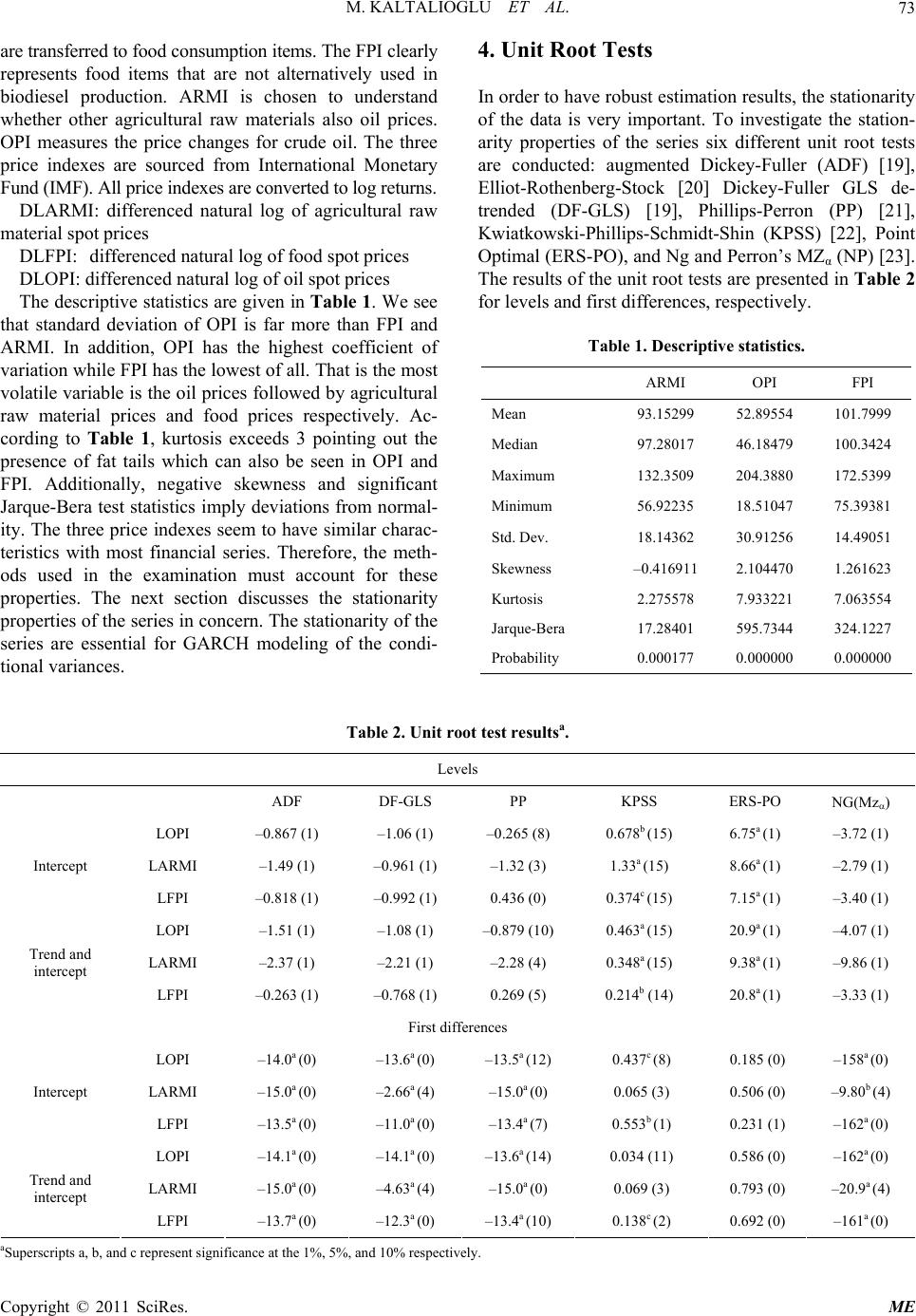

at lag 5 at the 5% significance level. There is also weak

evidence of Granger causality in variance from raw ma-

terials to food returns at lags 1 and 5. The results also

show that there is a contemporaneous link between oil

and agricultural raw material returns. This is not surpris-

ing since both are used as inputs in further production. At

the 5% significance level oil volatility leads agricultural

raw material volatility at lag 8. The CN procedure pro-

vides some evidence of a volatility spillover from oil to

food returns at lag 1. However, the result is weak since

the test statistic is very close to the 10% critical value of

1.28.

Although the CN procedure seems to have uncovered

links between the volatilities of the three indexes, the

evidence is not too strong and the fact that the spillover

occurs in 5 to 8 months indicate that the markets respond

with a lag to changes in the volatility in the other market.

The only link that can be easily interpreted is the con-

temporaneous adjustment of the agricultural raw material

and oil returns since they are closely linked to the pro-

duction processes. The neutrality between agricultural

raw material, food and oil returns is confirmed by the

volatility spillover test results.

6. Conclusions

The commodity markets are viewed as attractive invest-

ment areas as alternatives to financial markets. If they

are seen as alternative investment areas, then commodity

prices must respond to the same factors as financial asset

prices. One such factor is oil price shocks. The respon-

siveness of financial returns to oil price shocks has been

studied a lot in the literature. However, the commodity

market and energy market links are only recently attract-

ing attention. In the commodity price-energy price, food

and agricultural raw material prices is probably the least

studied.

Countries that rely on commodity trade are more vul-

nerable to risk and uncertainty in commodity prices. Price

instability affects producers, investors, financial inter-

mediaries and policy makers in addition to its negative

impact on growth and income distribution. Volatility has

been a major source of price instability and its impor-

tance has not diminished due to more liberalization, re-

duction of barriers to trade, and globalization. There is a

developed commodity derivatives market available for

hedging against the commodity price risk, but problems

still remain due to low accessibility of such markets,

spread between local and international prices, low liquid-

ity, lack of local reference prices, lack of derivative in-

struments for certain commodities [25]. The transfer of

volatility between commodity markets makes decisions

even harder for producers, traders and policy makers. If

there is no volatility spillover between alternative com-

modity markets, then market based approaches can be

used to diversify risk. However, if there is evidence of

risk transmission, traditional methods like regulations,

buffer stocks, buffer funds, and international agreements

[25] can be sought.

This paper investigates the volatility spillover between

world oil, food, and agricultural raw material price in-

dexes. We find that there is no volatility spillover from

the oil returns to the food returns. Overall our results

indicate only a contemporaneous link between oil and

agricultural raw materials. Since there is no relationship

between the three market returns studied, there are risk

reduction benefits from employing the three price in-

dexes in portfolio formation. Furthermore, policy makers

cannot use developments in the world oil market to im-

prove their forecasts of the food and agricultural raw

material prices and volatilities. Our results do not support

the claim that oil price hikes are causing the inflation in

food prices.

Further research examining the information transmis-

sion mechanisms between oil prices and individual prices

of different food items or different agricultural indexes

(i.e., wheat, corn, soybean etc.) may prove to be fruitful.

The price and volatility spillover from international

markets to local markets is also an area where further

research is needed. Since commodity markets are increas-

ingly viewed as assets, the dynamic relationship between

commodity prices and financial markets is also of inter-

est to producers, traders, policy makers and scholars.

7. References

[1] C. P. Timmer, “Causes of High Food Prices,” ADB Eco-

nomics Working Paper Series, Asian Development Bank,

Vol. 128, 2008.

[2] P. C. Abbott, C. Hurt and W. E. Tyner, “What’s Driving

Food Prices?” Farm Foundation Issue Reports, July 2008.

http://ageconsearch.umn.edu/bitstream/37951/2/FINAL%

20WDFP%20REPORT%207-28-08.pdf

[3] Agricultural Trade Policy Analysis, “High Prices on

Agricultural Commodity Markets: Situation and Pros-

pects: A Review of Causes of High Prices and Outlook for

World Agricultural Markets,” Review, European Com-

mission, Directorate-General for Agriculture and Rural

Development, Brussels, 2008.

[4] K. Collins, “The Role of Biofuels and Other Factors in

Increasing Farm and Food Prices: A Review of Recent

Development with a Focus on Feed Grain Markets and

Market Prospects,” Supporting Material for a Review

Conducted by Kraft Foods Global, Inc., 2008.

[5] W. Coyle, M. Gehlhar, T. Hertel, Z. Wnag and W. Yu,

“Understanding the Determinants of Structural Change in

World Food Markets,” American Journal of Agricultural

Economics, Vol. 80, No. 5, 1998, pp. 1051-1061.