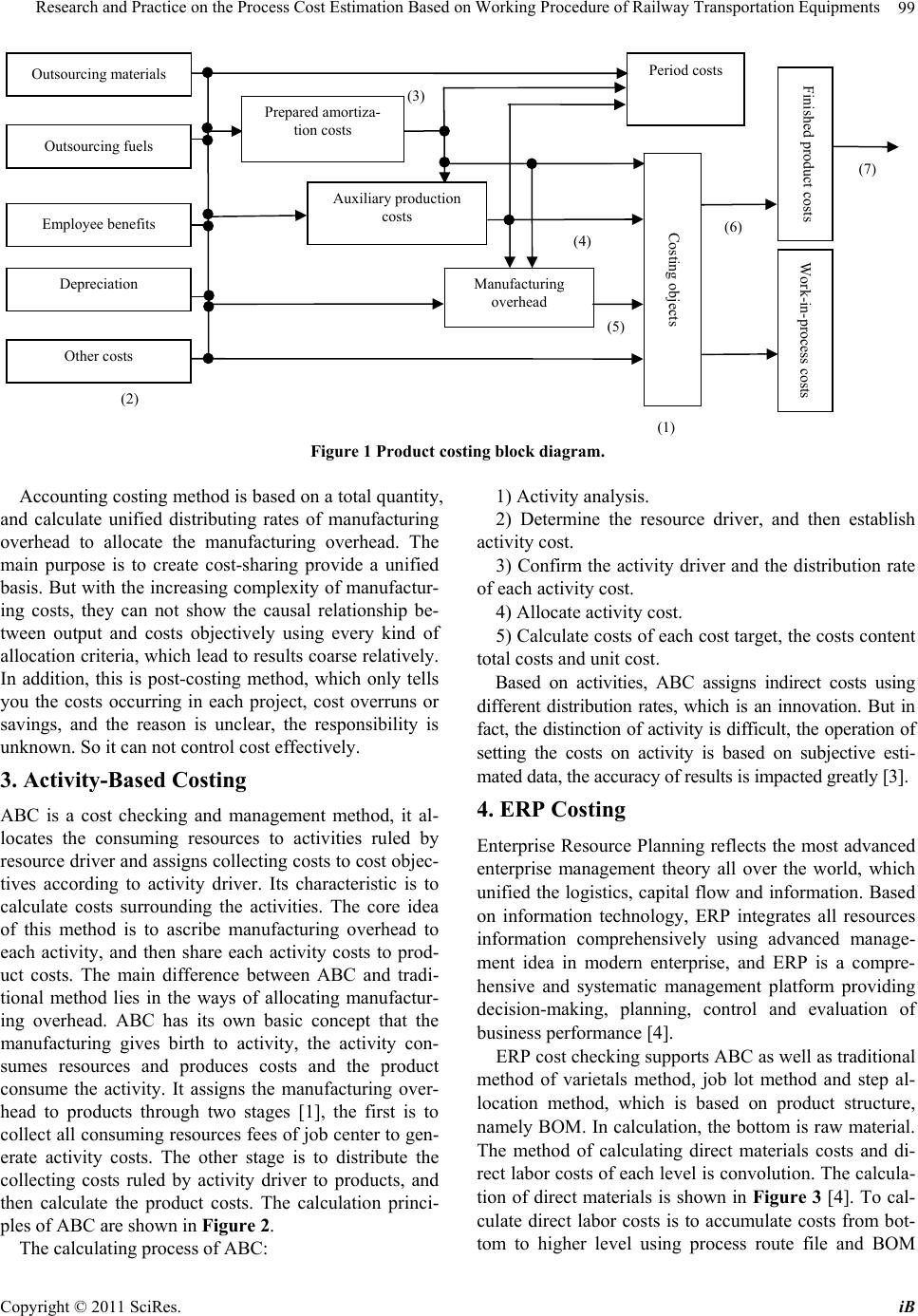

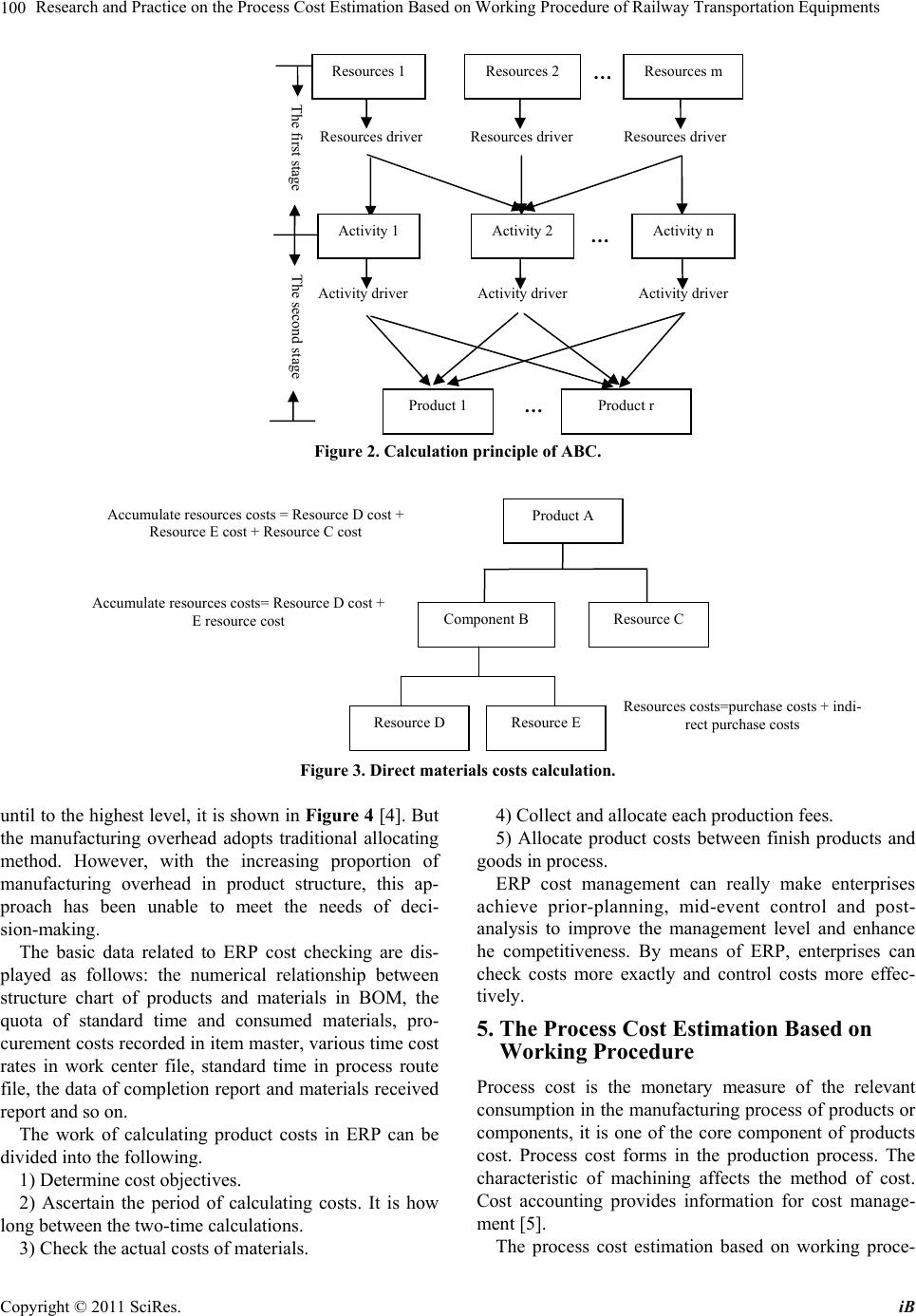

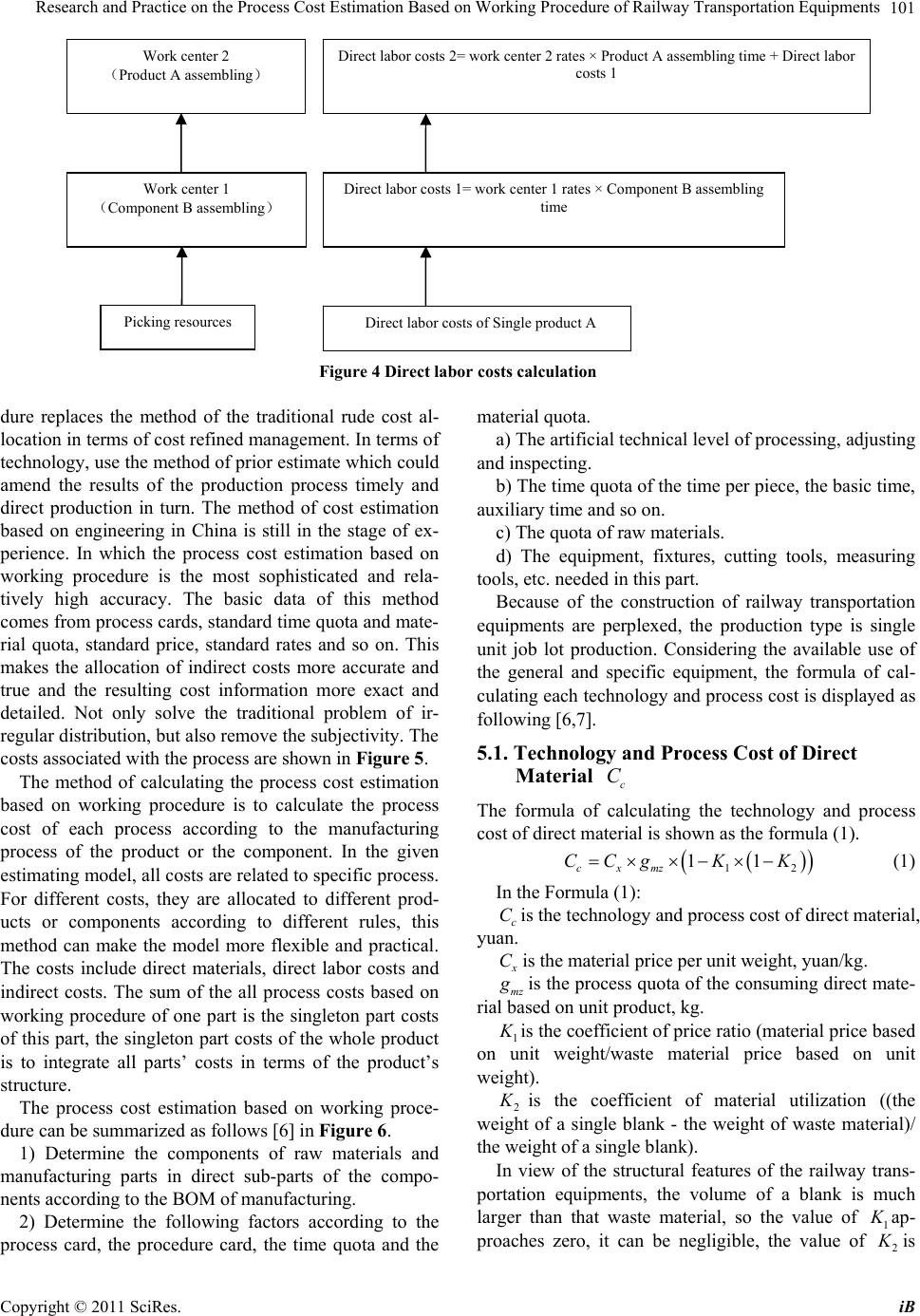

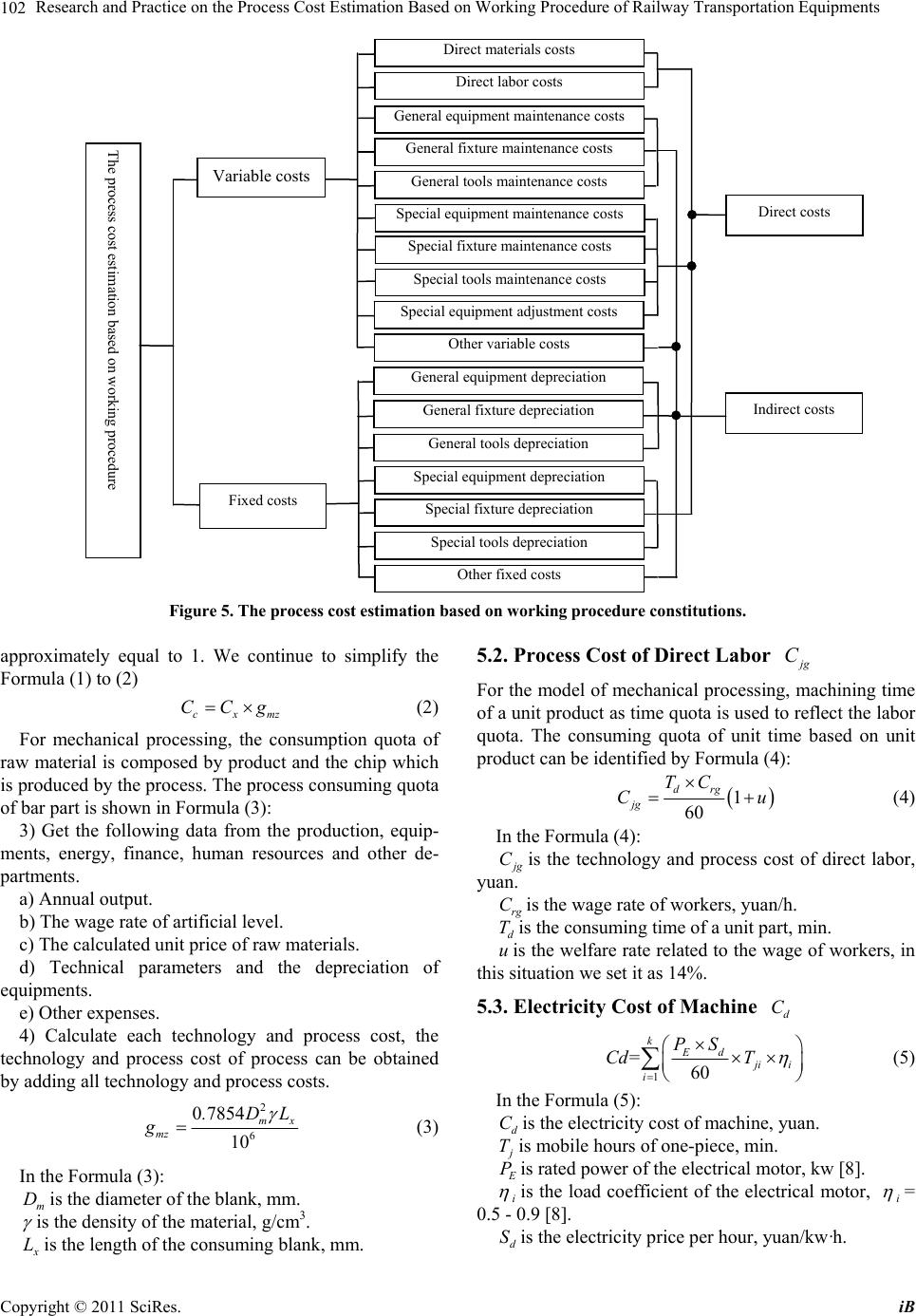

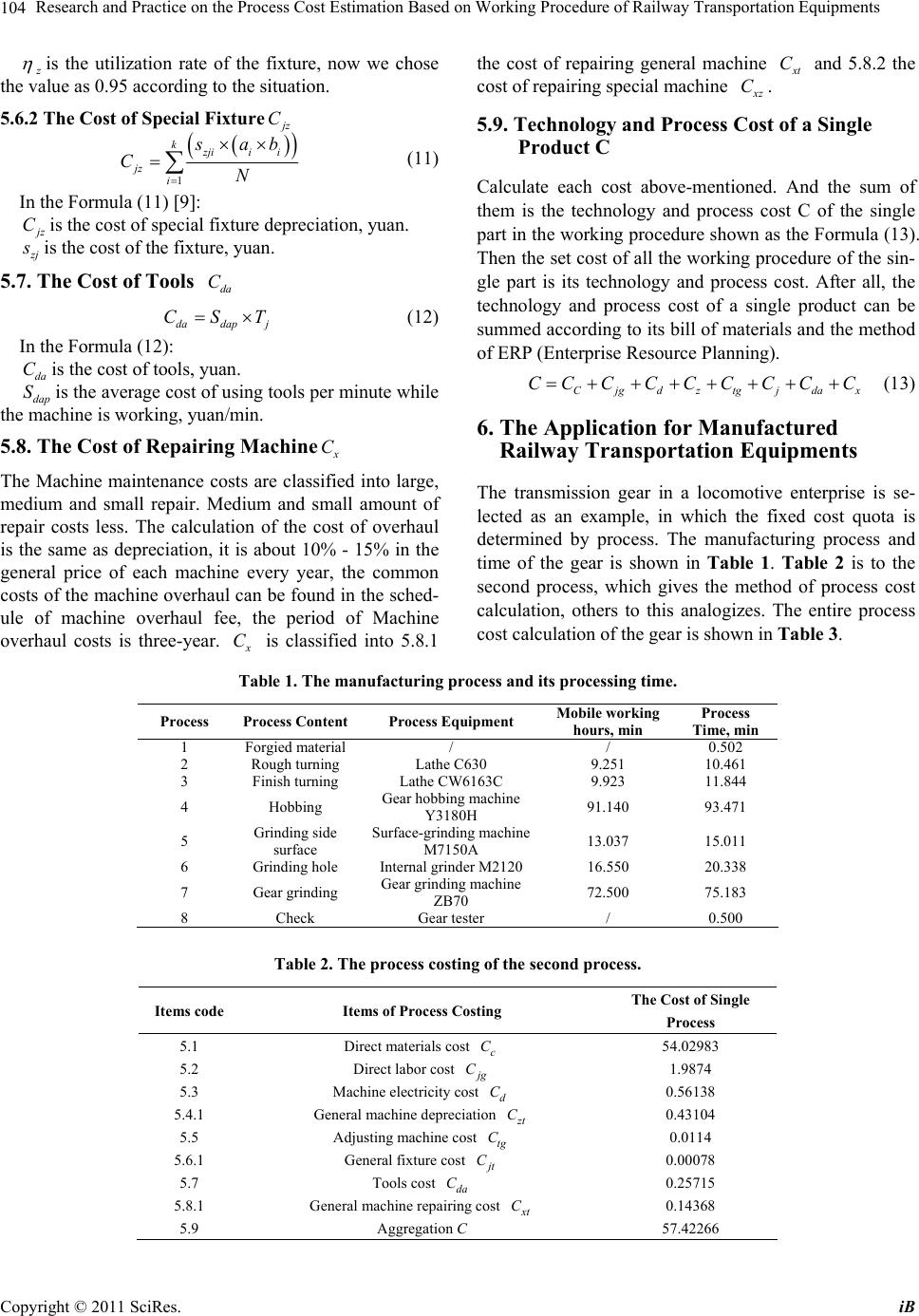

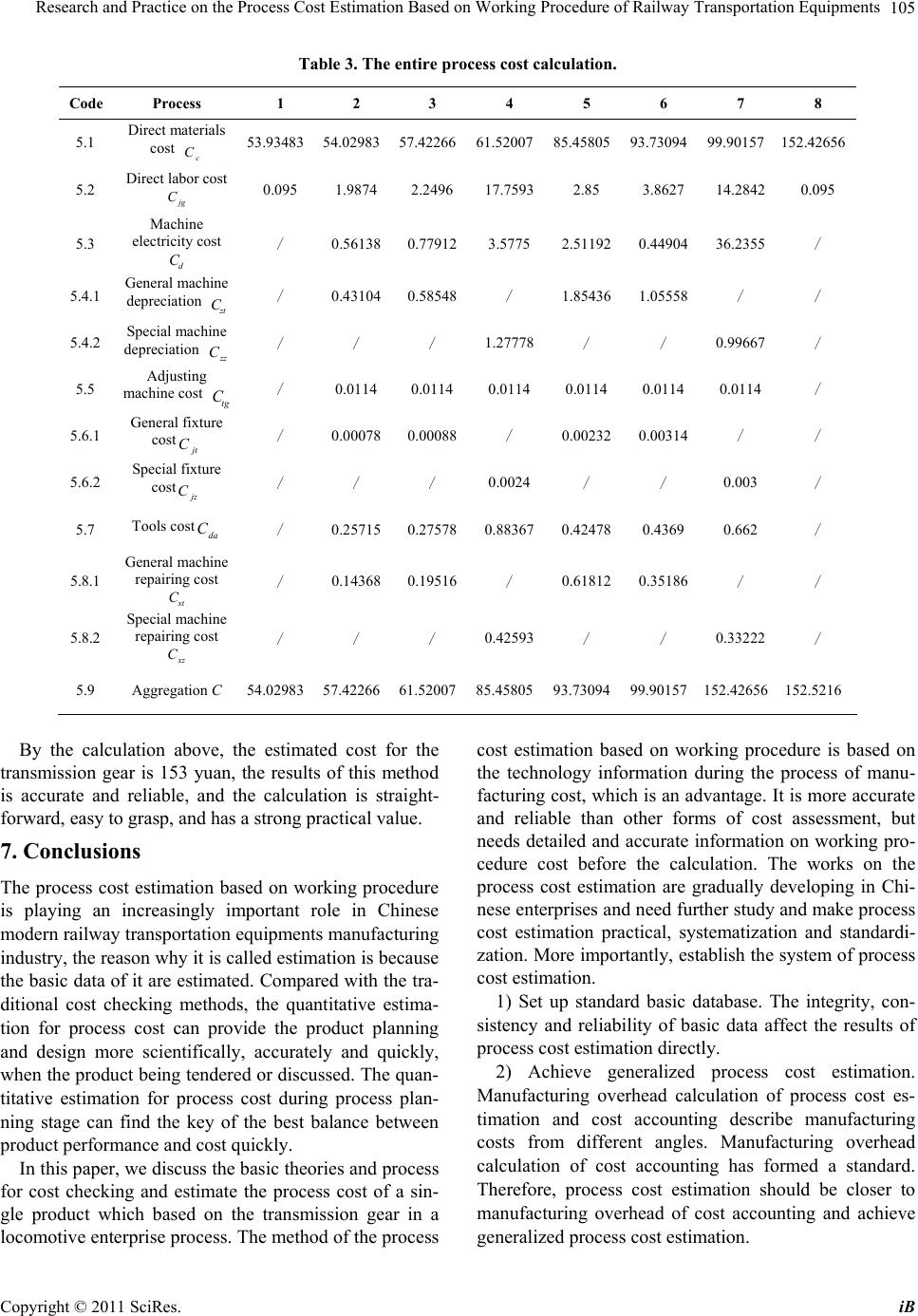

Research and Practice on the Process Cost Estimation Based on Working Procedure of Railway Transportation Equipments

98

2. Accounting Cost Calculation

2.1. Accounting Cost Estimation

There are some methods of accounting cost estimation in

common use. The high-low method of cost estimation is

direct way to determine the variable cost and fixed cost.

Its main idea is to confirm unit variable cost to the cost

variance of the highest point and the lowest point cost of

volume of business history in relevant range. And fixed

cost can be got by subtracting variable cost from total

cost. Scatter diagram is a useful means of cost estimation

using graphic method. It is more efficient especially to-

gether with the use of other methods of cost estimation.

That method is to draw the historical cost data points on

the coordinate diagram and to determine the cost perti-

nence. Least-squares regression analysis is to develop the

observation data into a cost estimation formula using

mathematical methods. Its idea is to minimize the sum of

vertical variance between actual cost values and esti-

mated values of each observation point [1].

Accounting prior-cost estimation is generally based on

statistical result of historical cost data. It considers only

the factor of the volume of business generally, and lacks

of affirmatory conditions. So the estimated result is im-

precise.

2.2. Accounting Costing

Product costing makes product as the basic cell in calcu-

lating cost, such as particular product or batch of prod-

ucts, or a particular manufacturing process. The costing

method is called manufacturing costing method within

the range of manufacturing [2].

2.2.1. Cost Stru cture

The cost structure of manufacturing cost method includes

direct materials and direct labor and manufacturing

overhead.

Direct materials cost is the cost of main raw materials

applied to a particular product. It depends on the con-

sumption number of unit material. And it can be identi-

fied simply by multiplying the consumption number of

raw materials and its unit cost.

Direct labor cost is the cost of labor applied to a par-

ticular product. It can be got by multiplying the direct

labor time and wage rate.

Manufacturing overhead includes all manufacturing

cost besides direct materials and direct labor. It is used

directly for production, but it fails to be credited directly

to a particular product cost. Most elements of manufac-

turing overhead do not have direct relationship to proc-

essing of the product. In actual production costing, if the

workshop produces only a product, the manufacturing

costs can be reckoned directly in production cost of the

product, otherwise the manufacturing cost is reckoned in

various products respectively ruled by reasonable alloca-

tion method. There are a lot of methods to assign manu-

facturing cost. Some of them are commonly used, such as

proportion al distribution of the prod uction hours, propor-

tional distribution of worker’s wage, proportional distri-

bution of machine hours and proportional distribution of

annual planning.

2.2.2. Costing Methods

The manufacturing costing methods can be divided into

category costing method, job order costing method and

process costing method [2].

The category costing method is a calculating cost

method considering the assortment as cost objectives to

collect and allocate production costs. The costs are dis-

tributed between finished product and good in process.

This method is suitable for volume-produce of one step

produce and multi-step produce calculating costs ac-

cording to production steps on management.

The job order costing method is to collect production

costs in accordance with the batch or order form and

mainly used in single and small batch production. This

method seems each product or each batch as the cost

objective to calculate the costs. The calculating cycle of

cost consistent with its life cycle and the produ ction costs

are collected in different batches.

The process costing method is to calculate product

costs based on production steps and species of goods to

collect and allocate production fees applying for con-

tinuous, large and multi-step producing industrial enter-

prises. In the light of different situation, it can be divided

into parallel step, the proportion of law equivalent units,

and gradually carried forward sub-step.

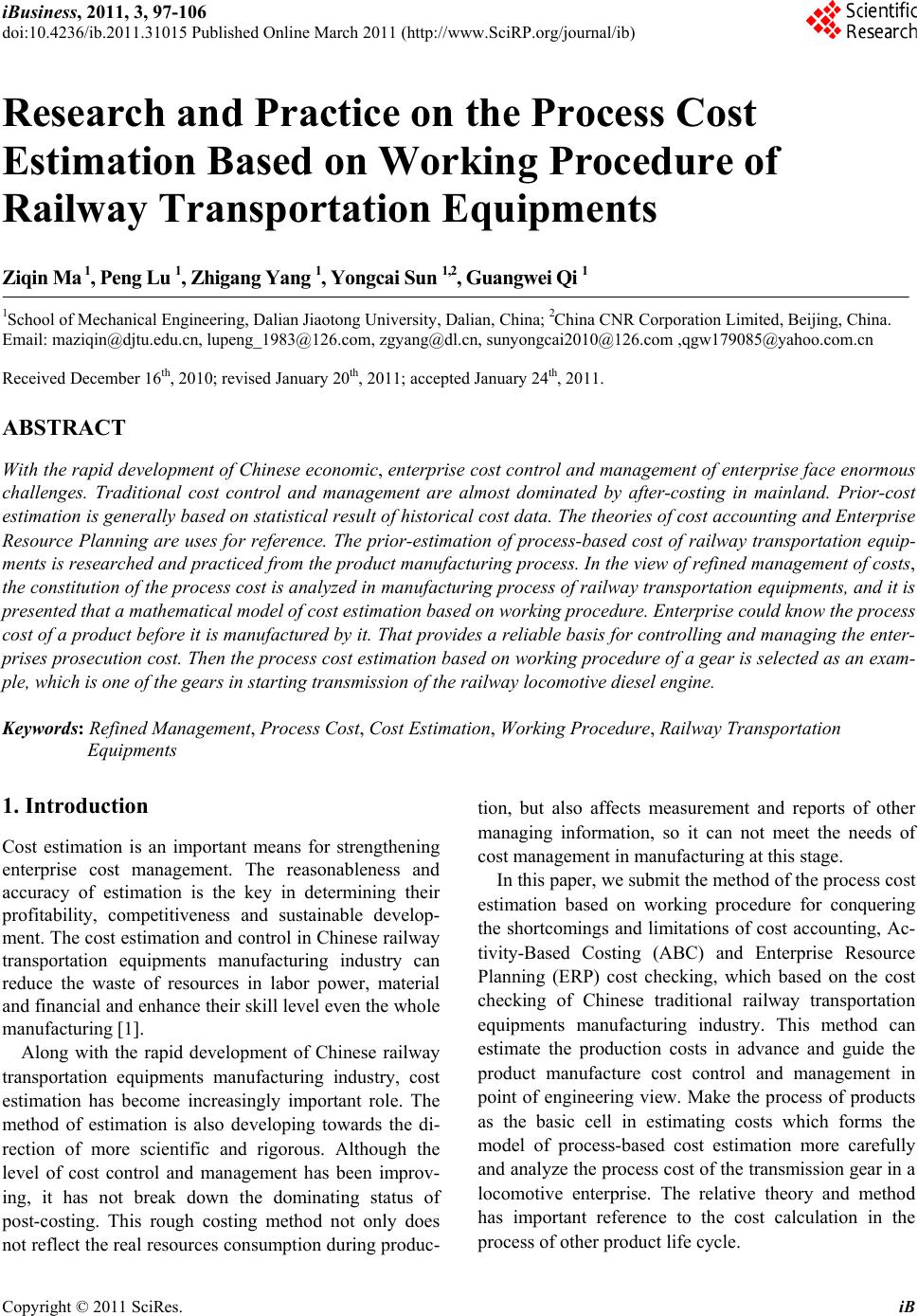

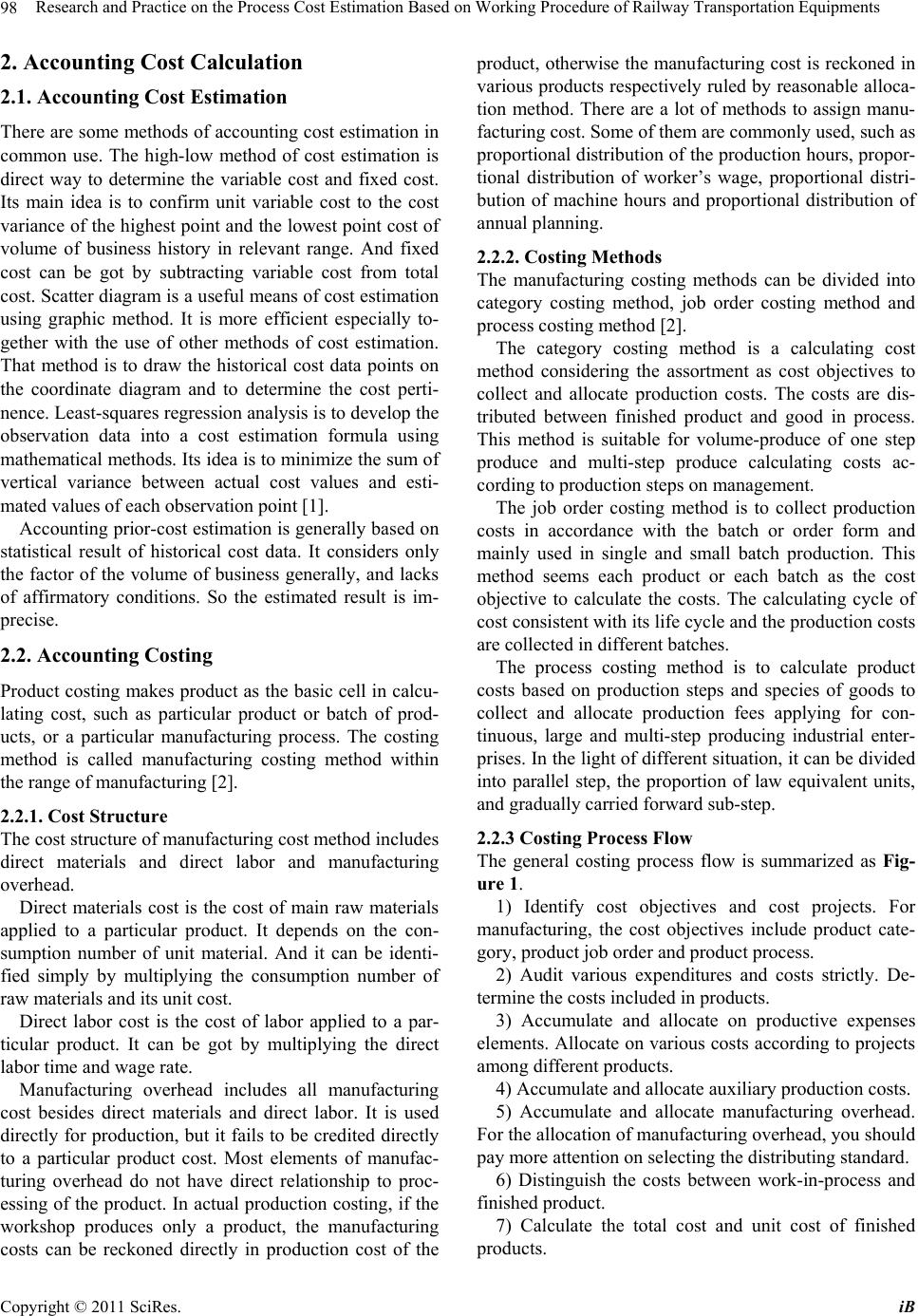

2.2.3 Costing Process Flow

The general costing process flow is summarized as Fig-

ure 1.

1) Identify cost objectives and cost projects. For

manufacturing, the cost objectives include product cate-

gory, product job order and product process.

2) Audit various expenditures and costs strictly. De-

termine the costs includ ed in products.

3) Accumulate and allocate on productive expenses

elements. Allocate on various costs according to projects

among different products.

4) Accumulate and allocate au xiliary production costs.

5) Accumulate and allocate manufacturing overhead.

For the allocation of manuf acturing overhead, you sh ould

pay more attention on selecting the distributing standard.

6) Distinguish the costs between work-in-process and

finished product.

7) Calculate the total cost and unit cost of finished

products.

Copyright © 2011 SciRes. iB