R. BANSAL, A. KHANNA

Table 4.

Results of null hypothesis @ 5% significance level (z = ± 1.96).

S. No. Variable z-StatNull

hypothesis H0 Relation with

underpricing

1 LOGISSUESIZE −3.98Rejected Negative

2 LOGINDP 0.18Accepted No relation

3 LOP

LOP

SUN

P No relation

OFFER TIMING

N

N

GINDNON0.54Accepted No relation

4 GNONINSTNON0.78Accepted No relation

5 LOG NO OF

SHARES 1.99Rejected Positive

6 LOGAGE −0.70Accepted No relation

7 LOGMKTCAP 2.04Rejected Positive

8 BB 2.67Rejected Positive

9 BSCRIPTIO6.00Rejected Positive

10 RIVATE FIRM’S0.40Accepted

11 1.99Rejected Positive

12 Y2000 −1.14 Accepted o relation

13 Y2001 −0.48 Accepted No relation

14 Y2002 −0.62 Accepted o relation

15 Y2003 −0.61 Accepted No relation

16 Y2004 −0.37 Accepted No relation

17 Y2005 −1.50 Accepted No relation

18 Y2006 −1.99Rejected Negative

19 Y2007 −0.65 Accepted No relation

20 Y2009 −1.99Rejected Negative

21 Y2010 −0.48 Accepted No relation

22 Y2011 1.99Rejected Positive

Co ion

ing intot all fihiche pe

of marke Stock Enge y fo

1999 until 2011, this study examines the evidence on the short-

run under-pricing of IP an average underpric-

ing level within the range 50% is found based on the first day.

U

prospective investors should pursue the strategy of buying the

th

)90060-3

nclus

Tak accounrms w have gonublic on th

ficialt of thexchaof Bombar the period

Os. In particular,

sing a regression approach, the degree of underpricing is ex-

plained by the ex-ante uncertainty hypothesis and the owner-

ship structure hypothesis. However, there is limited support for

the signaling hypothesis. In particular, the results show that the

ex-ante information and has a significant positive impact on the

initial returns while the ownership structure has no relevant

negative effect on short-run underpricing. Conversely, the re-

sults show that there is no statistically significant relationship

with other explanatory factors such as return on firm’s age, and

IPO years, ownership structure and the level of underpricing.

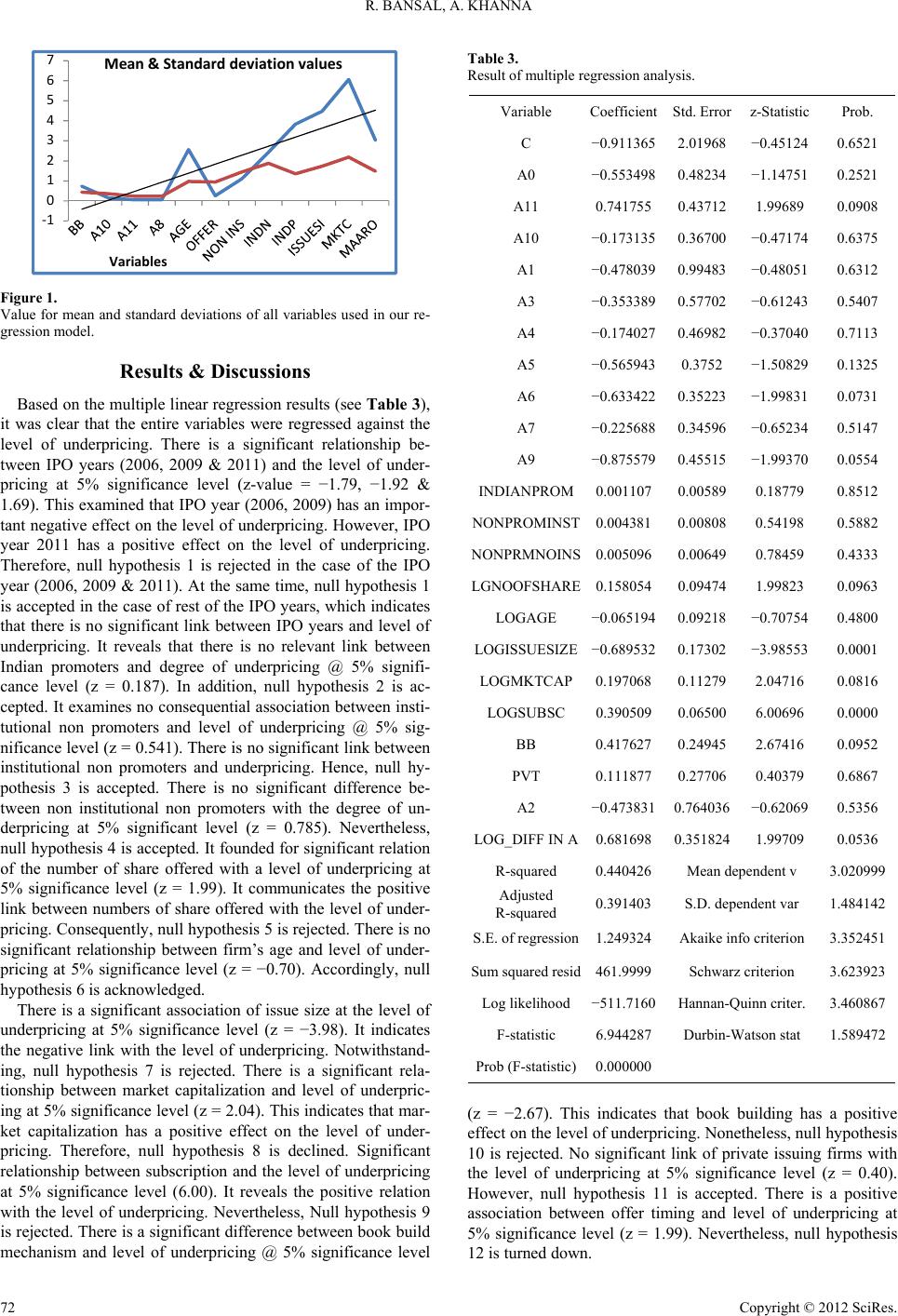

The results obtained from this study (see Table 4) show that

fresh issues on the BSE are subject to underpricing, consistent

with developed and other emerging markets. In this respect,

new issues at the offer and selling them immediately on the

initial day of trading. Notwithstanding, the study also reveals

at investors should not hold new issues very long as the high-

est component of the initial returns is found on the first day of

trading and that the average original returns turn negative on

the fourth day of trading.

REFERENCES

Allen, F., & Faulhaber, G. (1989). Signaling by under pricing in the

IPO market. Journal of Financial Economics, 23, 303-323.

doi:10.1016/0304-405X(89

Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock mar-

ket. Journal of Economic P151.

doi:10.1257/jep.21.2.

erspectives, 21, 129-

129

Baron, D. P. (1982). A model of the demand for investment banking

advising and distribution services for new issues. The Journal of Fi-

nance, 37, 955-976. doi:10.1111/j.1540-6261.1982.tb03591.x

Bferential information and secu-

rity market equilibrium. Journal of Financial Quantitative Analysis,

20, 407-422.

arry, C. B., & Brown, S. (1985). Dif

doi:10.2307/2330758

ansal, R., & Khanna, A. (B2012). Pricing mechanism and explaining

underpricing of IPOs, evidence from Bombay stock exchange India.

International Journal of Research in Finance and Marketing, 2, 205-

216.

Bansal R., & Khanna, R. (2012). Post Indian stock market’s crisis and

its impact on IPOs underpricing: Evidence from 2008-2011. Asian

Journal of Management Research, 3, 1-11.

Bansal R., & Khanna, R. (2012). IPOs underpricing and money “left on

the table” in Indian market. International Journal of Research in

Management, Economics and Commerce, 2, 106-120.

Bansal R., & Khanna, R. (2012). Share holding’s pattern and its impact

on IPO Underpricing: After Indian stock market crisis in 2008. Asian

Journal of Research in Business, Economics and Management, 2,

159-174.

Bansal R., & Khanna, R. (2012). Does ownership structure affecting

IPO underpricing: A case of Indian stock market. International Jour-

nal of Business Economics and Management Research, 3, 39-51.

Bansal R., & Khanna, R. (2012). IPO underpricing cloud or rain: Event

commencing from Bombay stock exchange. International Journal of

Management and Behavioural Science, 1, 154-179.

ansal R., &B Khanna, R. (2012). Analysis of IPO underpricing: Evi-

dence from Bombay stock Exchange. International Journal of Re-

search in Commerce, It & Management, 2, 1-6.

enveniste, L. M., & Spindt, P. A. (1989). How investment bankBers

determine the offer price and allocation of new issues. Journal of

Financial Economics, 2 4, 343-361.

doi:10.1016/0304-405X(89)90051-2

Dolvin, S. D., & Jordan, B. D. (2008). Underpricing, overhang, and the

cost of going public to pre-exiting shareholders. Journal of Business

Finance and Accounting, 35, 434-458.

doi:10.1111/j.1468-5957.2008.02087.x

inblatt, M., & Hwang, C. Y. (1989). Signaling and the pricing of new

issues. Journal of Finance, 44, 393-42

oughran, T., & Ritter, J. R. (1994). Initial

Gr

0

L pubic offerings: Interna-

tional insights. Pacific Basin Finance Journal, 2, 165-199.

doi:10.1016/0927-538X(94)90016-7

eite, T. (2007). Adverse selection, public

ing in IPOs. Journal of Corp orate Finan

Linformation, and underpric-

ce, 13, 813-903.

doi:10.1016/j.jcorpfin.2007.04.010

cDonald, J. G., & Fisher, A. K. (1972).M New issues stock price be-

havior. Journal of Finance, 27, 97-102.

doi:10.1111/j.1540-6261.1972.tb00624.x

egginson, W. L., & Weiss, K. A. (199M1). Venture capitalist certifica-

tion in initial public offerings. Journ al of Finance, 46, 879-903.

doi:10.1111/j.1540-6261.1991.tb03770.x

uscarella, C. J., & Vetsuypens, M. R. (M1989). A simple test of Ba-

ron’s model of IPO underpricing. Journal of Financial Economics,

24, 125-135. doi:10.1016/0304-405X(89)90074-3

Copyright © 2012 SciRes. 73