M. JEDRZEJCZYK 781

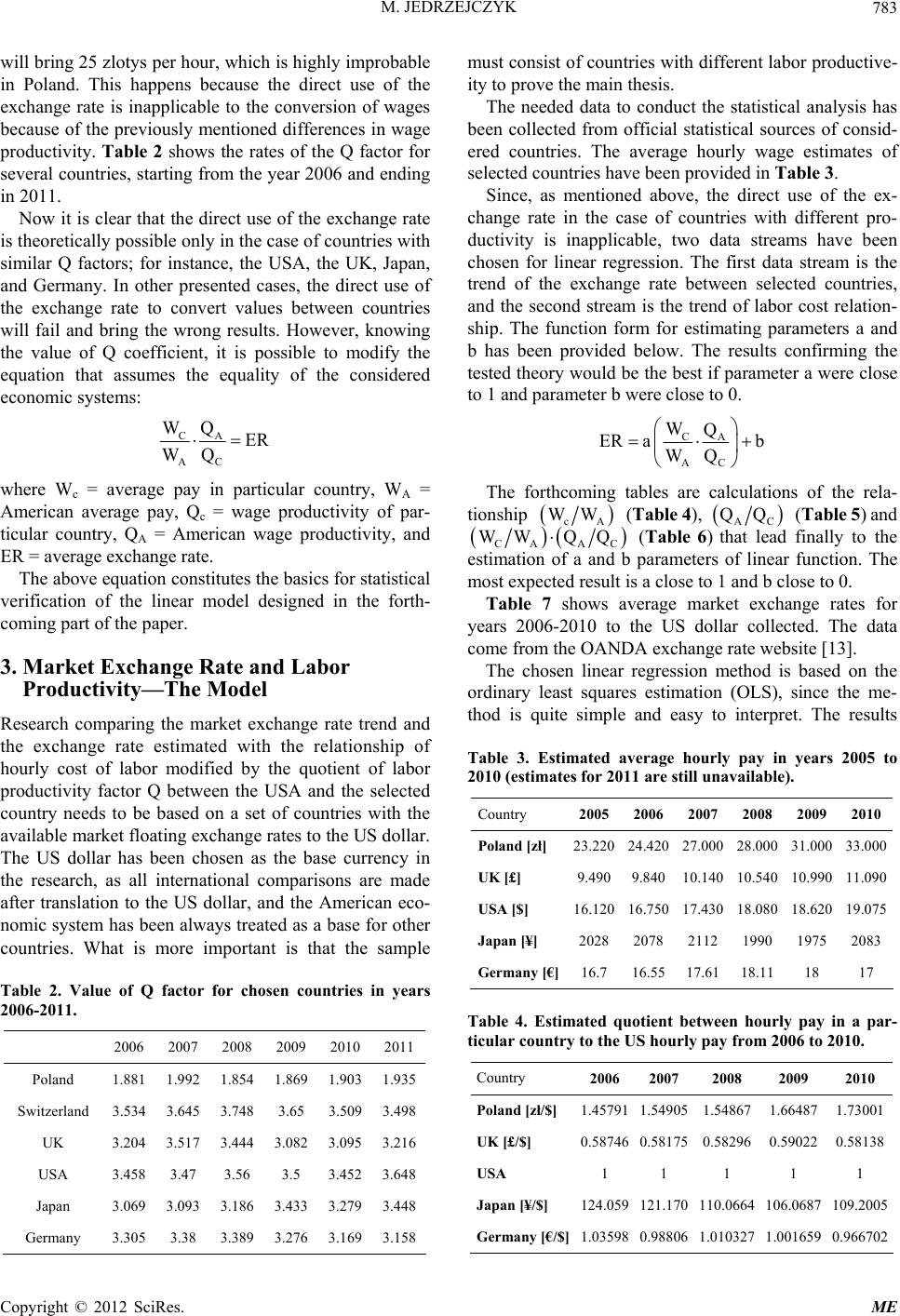

Table 1. Comparative analysis of the 1.5 kW engines manu-

factured in Poland and the USA.

TAMEL (Poland) BALDOR ELECTRIC (USA)

Power 1.5 kW

Sg 90 L-4

B3

400 V

50 Hz

Insulation class F

1200 rpm

Power 1.5 kW

4 Pole

B3 Mounting

460 V

50 Hz

Insulation class F

1140 rpm

SALE PRICE:

424.00 zł $ 637

AFTER TRANSLATION (CONVERSION):

$193 1399.2 zł

duced in the USA by Baldor Electric Co. The end cus-

tomer use of the above-mentioned engines may be con-

sidered the same in spite of the slight differences in pa-

rameters. Table 1 presents the technical specifications of

the engines and selling prices on the domestic markets.

The exchange rate was assumed at the market level of

3.3 zloty per one dollar, according to the conducted

market observation1. If we try to compute the value of

the engine in Polish zloty, we will discover a huge dif-

ference in the resulting amounts. The American price for

the product and the exchange rate between the US dollar

and the Polish zloty gives us a total of 1399.2 zł. There-

fore, preliminary analysis shows great inconsistencies

with the law of one price, which states that the price of

the same or almost the same goods in the different mar-

kets should be equal. We might add that the law of one

price is applied in every methodology specifying conver-

sion rules, but is not necessarily a written law. Using the

exchange rate, which fluctuates but still remains on a

similar level, we can say that the law of one price does

not work in this case at all. This means that the values on

the international scale are incomparable. This was con-

firmed as well by Pakko and Pollard in 1996 on the

BigMac example [3].

It should also be stressed that the US Financial Ac-

counting Standards Board believes that “for an enterprise

operating in multiple currency environments, a true sin-

gle unit of measure does not, as a factual matter, exist”

[4]. In the passage that follows, we read, “the temporal

method obscures the fact of multiple units by requiring

all transactions to be measured as if the transactions oc-

curred in dollars.” The above mentioned method seems

to be treated as the best of all known algorithms. “The

most relevant information about the performance and

financial position of foreign entities is provided by the

functional currency financial statements of those entities.

Using the current exchange rate to restate those func-

tional currency financial statements in terms of their cur-

rent dollar equivalent preserves that most relevant infor-

mation” [4]. These quotes lead one to conclude that the

one and only method of translation in the consolidated

financial statements is based on the exchange rate.

In many published papers, for example W. Kołodko

and others, there is a noticeable tendency to avoid the

exchange rate in international comparisons [5]. Instead of

using the exchange rate, the authors use the so-called

Purchasing Power Standard (PPS), which represents the

equal bundle of goods and services in each country that

underlies the comparison. So, according to the above-

mentioned methodology, GDP is shown in one artificial

currency, which constitutes an attempt to avoid including

the exchange rate in the comparison.

However, there are many aspects of the translation

process, in which noticeable inconsistencies take place.

Therefore, the most important matter is to clarify the

essence of the money and monetary unit value and their

determinants in the international context. In the forth-

coming sections of the paper, labor productivity as the

determinant of the monetary unit value will be formally

presented.

2. Labor Productivity as a Determinant of

Money Value in the International Context

There are many theories describing the exchange rate

behavior. The fundamental assumption is Law of One

Price, formulated by English economist Keith Pilbeam,

stating that equal goods should have the same price on

different markets in the absence of transport costs and

barriers to trade [6]. So-called absolute Purchasing Po-

wer Parity (PPP) is based directly on the Law of One

Price and estimates the exchange rate as the value rela-

tionship between two identical goods on different mar-

kets. For instance, if the bundle of goods costs 200 zł in

Poland and $100 in the US, the exchange rate as defined

as zlotys per dollar should be 200 zł/$100 = 2 zł/$. Thus

the absolute version can be described with the following

simple formula:

P

A

q

ER q

,

where ER = exchange rate, qP = value on the Polish

market, and qA = value on the American market.

The relative PPP argues that the exchange rate adjusts

for inflation differences between two countries:

%∆S = %∆P – %∆P*,

where %∆S = percentage change of the exchange rate,

%∆P = domestic inflation rate, and %∆P* = the foreign

exchange rate. The long-run testing of the relative PPP

had shown many inconsistencies and finally has not been

1The exchange rate has oscillated around 3.3 zloty per one dollar in the

first half of 2012.

Copyright © 2012 SciRes. ME