Paper Menu >>

Journal Menu >>

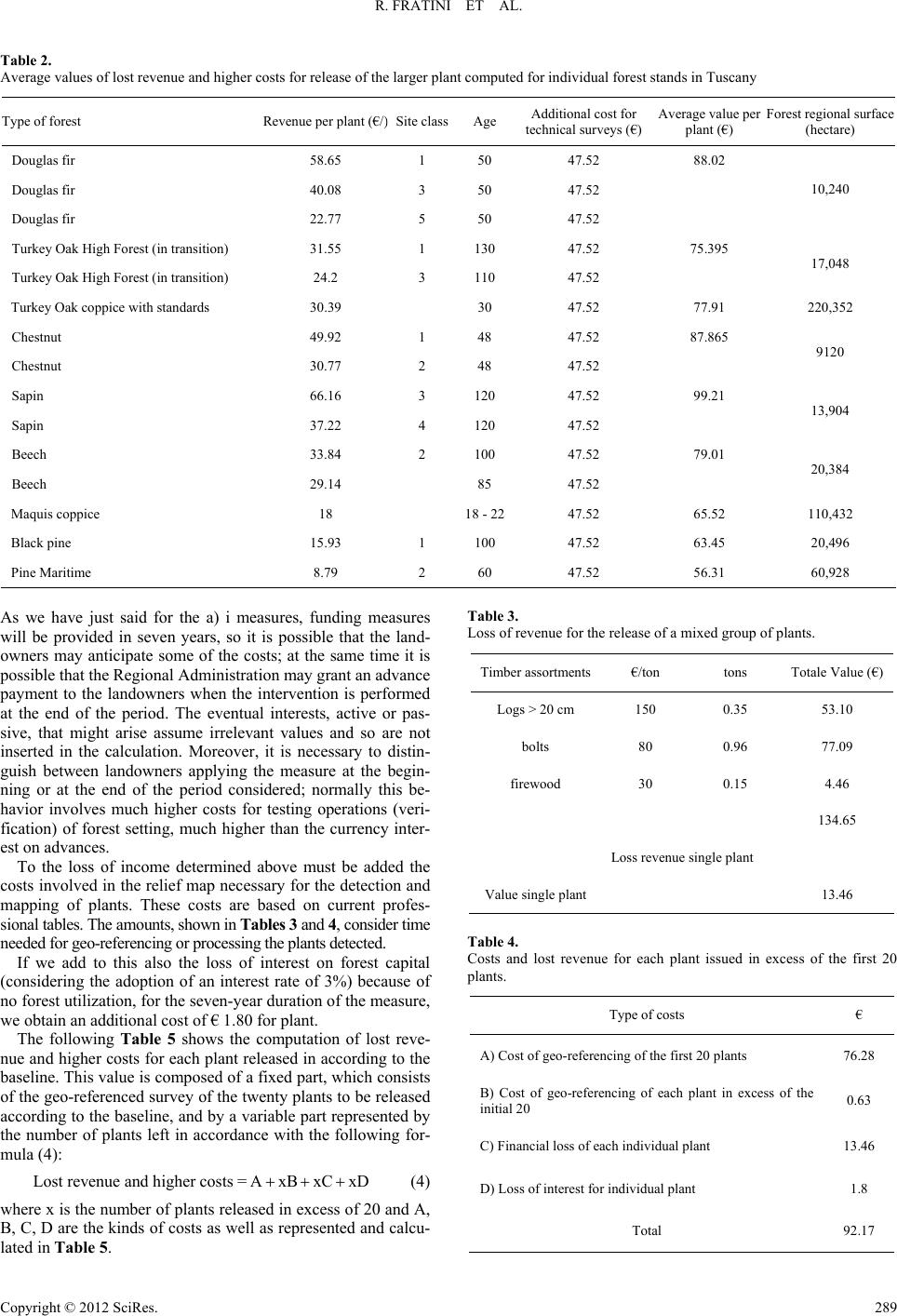

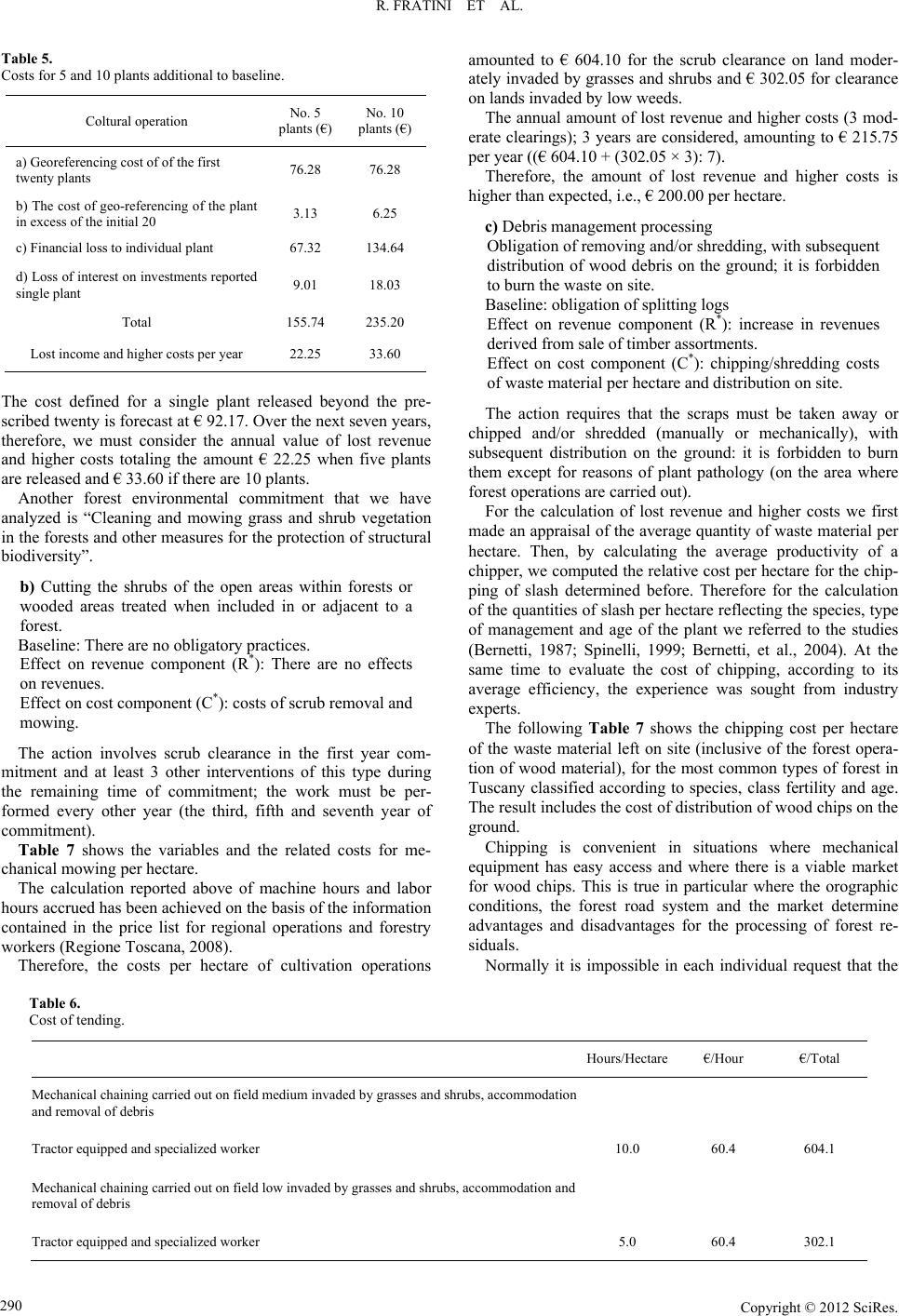

Open Journal of Forestry 2012. Vol.2, No.4, 286-292 Published Online October 2012 in SciRes (http://www.SciRP.org/journal/ojf) http://dx.doi.org/10.4236/ojf.2012.24036 Copyright © 2012 SciRes. 286 Appraisal of Aids as Provided by Rule 225 (Council Regulation (EC) No. 1698/2005) in Tuscany Region—Methodology, Procedures and Results*# Roberto Fratini, Enrico Marone, Gabriele Scozzafava Department of Agricultural and Fore st E conomics, Engineering, Sciences and Technologies, University of Florence, Florence, Italy Email: roberto.fratini@unifi.it, enrico.marone@unifi.it, gabriele.scozzafava@unifi.it Received July 31st, 2012; Revised September 5th, 2012; Accepted September 20th, 2012 The purpose of this paper is to illustrate a methodology to determine the lost revenue and increased costs resulting from the assumption of forest-environment commitments, as provided by rule 225 (Council Regulation (EC) No. 1698/2005) of the measure defined by the Tuscany Region. The aim is therefore to determine the appropriateness of the payments provided by European Community measures. Regulation (EC) No. 1698/2005 regards mainly land management and contributes to sustainable development by en- couraging farmers and forest holders to employ methods of land use compatible with the need to preserve the natural environment and landscape and protect and improve natural resources. This Rule covers sup- port for non-productive investments linked to the achievement of agro or forest-environmental commit- ments or the achievement of other agri-environmental objectives, as well as measures aimed at improving forestry resources with an environmental objective (support for the first forestation of agricultural land, establishment of agroforestry systems or restoring forestry potential and preventing natural disasters). We have worked by analyzing each of the commitments required by individual actions and checking their impact on forest regional management; we have calculated the additional costs and the lost revenue re- sulting from the assumption of commitments. Keywords: Forest Policy; Utilization Forest Costs; Financial Analysis Introduction The purpose of this paper is to illustrate a methodology to determine the lost revenue and increased costs resulting from the assumption of forest-environment commitments, as pro- vided by rule 225 (Council Regulation (EC) No. 1698/2005) of the measure defined by the Region of Tuscany. The aim is therefore to determine the appropriateness of the payments stipulated by European Community measures. Regulation (EC) No. 1698/2005 regards mainly land man- agement and contributes to sustainable development by en- couraging farmers and forest holders to employ methods of land use compatible with the need to preserve the natural envi- ronment and landscape and protect and improve natural re- sources. This regulation covers support for non-productive investments linked to the achievement of agro- or forest-envi- ronmental commitments or the achievement of other agro-en- vironmental objectives, as well as measures aimed at improving forestry resources with an environmental objective (support for the first forestation of agricultural land, establishment of agro- forestry systems or restoring forestry potential and preventing natural disasters) (OECD, 2011). Adopted Methodology We have worked by analyzing each of the commitments re- quired by individual actions and through a check of their impact on forest regional management; we have calculated the addi- tional costs and the lost revenue resulting from the assumption of these commitments. In any case we have the adoption vol- untary of practices that go beyond the normal standards of management, or beyond the obligations set by existing envi- ronmental rules and constraints and for this, there is no quanti- tative evidence in ordinary forest management for resulting in a difficult to quantify the economic cost. All calculations have been reported to the additional opera- tions provided by Measure 225 compared to a state of well- defined and fixed baseline. In addition, the calculation has been made by reference to Tuscan Forest Inventory, which clearly outlines the regional composition of the stands. We also made an appraisal of the value of timber production through the weighted means of tim- ber assortments and of mean annual increment. For the assessment of costs incurred by the forest owner, and thus the subsequent justification for the subsidies, we started from the consideration that the commitments in most cases represent an evident loss of wood and in an increase of costs related to longer time management and organization of the forest site and above all in a higher cost of logging. For the determination of aids on the basis of standard as- sumptions, we have distinguished three ways of calculating the adequacy of the premium considering the scale of production and related charges between ordinary forest management and another burdened with additional commitments: *This research was sponsored by Tuscan Region. #A synthesi s of th is paper was pres ented t o the I UFRO co nference, Vi terb o, Italy, 19-2 1 May 2011.  R. FRATINI ET AL. 1) The commitments act on production costs (processing) only. 2) The commitments act on revenues only. 3) The commitments act on both costs and revenues. For greater reliability in the calculation of lost revenue and higher costs, however, it is appropriate to justify the aid in proportion to the actual costs incurred and documented indi- vidually. In this case we must, in principle however, distinguish between the expenses that have a direct impact and those that are deferred to the end of cycle. For additional commitments with direct effects and for as- sessing the sufficiency of the contributions provided, we will mainly relate to the costs for the implementation of foreseen activities. As for the lost revenue related to “forest-environ- ment” activities which directly affect aspects, they must be considered strictly related to the loss in value of the techno- logical production of the timber. Therefore, for any type of forest-environment commitments, whether those that have direct effects on the costs or those that impact deferred income at the end cycle, the stumpage value (SV) will be influenced, directly or indirectly. It must be made clear that, as with the value of stumpage, which is codified by forest appraisal theory and widely adopted in forest practice (starting price for the sale of timber); it repre- sents, in fact, a transformation value of the forest production. In practice, stumpage value is calculated as the present value of the difference between the probable revenues from the sale of wood and the costs required for its use. In the case we would assume the stumpage value (SV) as a proxy of the Gross Margin we should assess SV without con- sidering fixed costs; in order to comply with EU guidelines economic factors/income attributable to fixed costs should not be included in the calculation. Gross margin per unit to be used in the calculation of ade- quacy of the premium must therefore consider only the costs attributable to production (specific costs), excluding all those cost items re lated to t he st ructure and busi ness orga nization (fixe d costs). The exclusion of these last items of expenditure fully cor- responds to the technical services of the European Commission (Article 53, paragraph 2 - e) of Regulation (EC) 2006/1974. The asset of budget of the production process is defined as gross output (GO), obtained as a sum of sales value (quantity sold multiplied by the market price of wood), the value of sec- ondary production and the value of products reutilized in other production processes (reinvestment). The value of these prod- ucts is determined by applying the unit value that coincides with probable market value made by the same assortment. Stumpage value means the value of standing trees, and therefore represents the economic results obtained (in terms of “ordinariness” or additional commitments to the ordinary), from the partial budget of forest utilization, comparing the pro- ceeds from the sale of wood products (active) with the costs for forest operations (passive). SVR C (1) where: SV = the stumpage value (€), R = revenues from sale of forest assortments, C = total costs (derived by forest utilization). In this case, we compare the stumpage value considered in an ordinary situation (i.e. the baseline) (SV) with stumpage value resulted fr o m the acti vities under each measure 225 (Vm*); is suffi- cient, for doing this comparison, to consider the individual effects on revenues and costs necessary to accomplish this activity. In fact, SV* differs from the SV as implementation of indi- vidual actions will cause a change in R and/or C according to the Formula (2): ** SVRRC C * (2) where R* and C* are the specific costs arising from the nth in- tervention Therefore, a comparison of the initial situation with that arising from application of individual actions foreseen by Measure 225 (SV – SV*) is solved considering only the effects ± R* and ± C* attributable to the other specific operations nec- essary to be in compliance with the guidelines. Given this, compared to the initial situation that derives from the application of the individual actions required by 225 (SV SV*), we should first define only the effects of ± R* and ± C*. *** SV SVRCRRCCRC ** (3) In this regard, Table 1 shows the effects on R* and C* arising from the adoption of individual actions. In the following we analyze in detail some of the most sig- nificant actions in order to improve the forest estate. Analysis and Results Calculation of lost revenue and of higher costs for individual measures adopted. a) i. Release, of one or more plants per hectare selected from among older species and/or of greater diameter and wood value, identified according to the criteria defined in Art. No. 12 of DPGR 2003/48 / Region of Tuscany. Baseline: on the occasion of forest cutting equal to or greater than one hectare, both in high forests and coppices, for every hectare of forest cut at least one plant per hectare must be left standing. The specimens to be released are those of the greatest diameter on the area to be cut, as indicated by the Forestry Regulations of Tuscany (DPGR No. 48/A of 08/08/2003, Arti- cle 12, paragraph 6. Effect on revenue component (R*): Loss of income de- rived from non-sale of timber assortments. Effect on cost component (C*) Increased costs for forest utilization and setting up of organization; loss of interest on invested capital (growing stock)1. For this determination we utilized yield tables relative to the stands that are typical in Tuscany (this criterion refers to the area forest inventory). We chose precisely those tables and classes of fertility which best reflect the production characteris- tics of these stands. The plant of the largest size was selected considering the customary rotation of the forest species in question; after we computed total yield by the average diameter and height of dominant plants and applied an appropriate dendrometric form factor. These parameters are normally set out with production tables (or Yield table). Then we considered the average stumpage price by reference to prices published in a specialized Journal (www.rivistasherwood.it/tecniko-pratiko/). When it was not possible to find the prices of wood products 1Technical operations chosen from among aged forest specimens and/o r those of greater diameter and/or greater wood value, with preference to those with nest cavities useful for bir d s . Copyright © 2012 SciRes. 287  R. FRATINI ET AL. Copyright © 2012 SciRes. 288 Tn of individual actions included in 225 measures. able 1. Examinatio Selection of forest species subject to utilization Effects on revenues Effect on costs 1) Release of one or more plants per hectare selected from those belong- ing specially older and/or greater diameter and/particularuy value, prefer- ring the eldest plant with cavity-nest for birds. Loss of income resulting from no timber use Increased of corgnization, ost for setting higher cost of forest utilization and for GPS marking 2) Release of at least 5 plants per hectare selected from those belonging to the species considered sporadic, and identified according to the criteria defined in 'article No 12 of DPGR 48/R; 08/08/2003. Loss of income resulting from no timber use Increased of cost for setting orgnization, higher cost of forest utilization and for GPS marking 3) Exploitation in coppice and high forest of different species of pine (Maritime pine and Black pine, etc.) and of coniferous trees all dried up without commercial value and high-flammability; Additional cost fo r cutting, haul a nd disposal of woo dy material Cleaning and mowing grass and shrub vegetation in the forests and other measures for the protection of biodiversity structure. Effects on revenues Effect on costs Cutting the shrubs in open areas within forests or wooded areas treated or adjacent to a forest. Cost of slashing Management of waste processing forest utilization Effects on revenues Effect on costs Obligation to remove or, alternatively, the obligation to chipping and/or chopping, resulting in distribution on the ground, of the residues from forest operations; ban on burning of waste wood. Sale of wood chip in larg e sacks Cost of chipping, chopping, or distributing of slash on the ground irectly, the analytical calculation of the costs of forest utiliza- page price we multiplied it ent of lost revenues and higher co r di selected from th fied according to the criteria defined in article No. 12 of DPGR orest species listed in paragraph 1 of article N operations for wh minimum, defined in A sa ention, we computed the stumpage value of a single pl d tion was carried out, at the same time utilizing the evaluations of wood prices from other appraisals. After determining the average stum by the percentage of timber assortments gotten from the plant released in order to estimate the loss of income; to this value we added an additional share needed for identification and geo- referencing of plants as previously explained. Funding meas- ures will be provided in seven years, so it is possible that the landowners might anticipate some of the costs, at the same time it is possible that the Regional Administration may grant an advance payment to the landowners because the intervention is performed at the end of the period. The eventual interests, ac- tive or passive, that might arise are assumed to be irrelevant and so they were not considered in the calculation. Moreover, it is necessary to distinguish between landowners applying the measure at the beginning or at the end of the period considered; normally this behavior involves much higher costs for testing operations (verification) of forest setting, much higher than the currency interest on advances. For a more completed assessm sts of this action we have considered the economic character- istics of main stands of Tuscany and principally the values of different wood assortments. In conclusion, the stumpage value is calculated for each plant identified in the forest (the average value is considered for forests that have different classes of fertility). The values identified are weighed according to the surface distribution of the different stands in the region (source: Forest Inventory of the Region of Tuscany, 1986), obtaining a weighted average value representative of Tuscan forest land. The action does not provide for a financial contribution fo fferent forest types, but a weighted average value; in this case, considering the different stands and surfaces, as highlighted in Table 2, corresponds to €76.96 per plant. The lost revenue and higher costs calculated for this intervention, therefore, will amount to €10.99 per plant per year (€ 76.96:7). a) ii. Release of at least 5 plants per hectare ose belonging to the species considered sporadic, and identi- 48/R ; 08/08/2003. Baseline: When cutting in coppice and high forest the iso- lated plants of the f o.12 of Forestry Regulations of Tuscany must be preserved, i.e., when the density of plants is less than twenty plants per hectare for each species, and having a diameter greater than 8 cm; subject to paragraphs 2 through 5 of that article. Effect on revenue component (R*): Loss of income de- rived from non-sale of timber assortments. Effect on cost component (C*) Loss of interest on invested capital (growing stock; costs for technical identification of individual plants) that consist of plant identification by GPS geo-referencing. The operation requires that the forest thinning or final cutting, en the density of the forest exceeds the rticle 12 Forestry Regulations of Tuscany, leaving from a minimum of 5 to a maximum of 10 plants per hectare in addi- tion to the baseline Tuscan Forestry Regulations. The plants left must be chosen from among the sporadic species (cited in the article) and identified according to the criteria defined therein. Since it is not possible to make a prediction for each species considered in order to determine the lost revenue due to the lost le of sporadic plants left in the forest, we proceeded to esti- mate the possible value. After the choice of 10 plants with a prevalence of the most representative species of Tuscan sylvi- colture, we calculated the volume in cubic meters) using a dou- ble entry yield table. Finally, after creating the scale of plants considered we computed the average stumpage value of timber assortments: saw logs, pulp logs, firewood, etc. utilizing timber prices published in the specialized literature (Tecniko Pratiko, 2009). To quantify the lost revenue and increased costs related to this interv ant, referring to average stumpage values of ten plants of different species and different age, height and diameter, broad- leaf in predominance.  R. FRATINI ET AL. Table 2. Average values of lost revenue and higher costs for r elease of the larger plant computed fo r individual forest stands in Tuscany Type of forest Revenue p er plant (€/)Site classAge Additional cost for Average value per technical surveys (€)Forest r egional surface plant (€) (hectare) Douglas fir 58.65 1 50 47.52 88.02 Douglas fir 40.08 3 50 47.52 Douglas fir 22.77 5 50 47.52 10,240 Turkey Oak High Forest (in tra nsition) 31.55 1 130 47.52 75.395 Turkey Oak High Forest (in tra nsition) 24.2 3 110 47.52 17,048 Turkey Oak coppice with standards 30.39 30 47.52 77.1 9220,352 Chestnut 49.92 1 48 47.52 87.865 Chestnut 30.77 2 48 47.52 9120 Sapin 66.16 3 120 47.52 99.1 2 Sapin 37.22 4 120 47.52 13,904 Beech 33.84 2 100 47.52 79.1 0 Beech 29.14 85 47.52 20,384 coppice 18 Maquis 18 - 2247.52 65.2 5110,432 Black pine 15.93 1 100 47.52 63.45 20,496 Pine Maritime 8.79 2 60 47.52 56.31 60,928 Ast said for the a) i measures, easur ill be provided in seven years, so it is possible that the land- e relief map necessary for the detection and m se of no cording to the ba whe in excess of 2 B, C, as represented a Table 3. Loss of revenue fo r the release of a mixed group of plants. s we have jufunding mes w owners may anticipate some of the costs; at the same time it is possible that the Regional Administration may grant an advance payment to the landowners when the intervention is performed at the end of the period. The eventual interests, active or pas- sive, that might arise assume irrelevant values and so are not inserted in the calculation. Moreover, it is necessary to distin- guish between landowners applying the measure at the begin- ning or at the end of the period considered; normally this be- havior involves much higher costs for testing operations (veri- fication) of forest setting, much higher than the currency inter- est on advances. To the loss of income determined above must be added the costs involved in th apping of plants. These costs are based on current profes- sional tables. The amounts , show n in Tab les 3 an d 4, consider time needed for geo-referencing or processing the plants detected. If we add to this also the loss of interest on forest capital (considering the adoption of an interest rate of 3%) becau forest utilization, for the seven-year duration of the measure, we obtain an additional cost of € 1.80 for plant. The following Table 5 shows the computation of lost reve- nue and higher costs for each plant released in ac seline. This value is composed of a fixed part, which consists of the geo-referenced survey of the twenty plants to be released according to the baseline, and by a variable part represented by the number of plants left in accordance with the following for- mula (4): Lost revenue and higher costs =AxBxCxD (4) re x is the number of plants released0 and A, D are the kinds of costs as wellnd calcu- lated in Table 5. Timbe r assor tment s€/ton tons Totale Value ( € ) Logs > 20 cm 150 0.35 53.10 bolts 80 0.96 77.09 firewood 30 0.15 4.46 134.65 Losnue singles reve plant 13.46 Value single plant Table 4. Costs and lost revor each plant issued in excess ofirst 20 pla enue f nts. the f Type of costs € A) Cost of geo-re ferencing of the first 20 plants 76.28 B) Cost of geo-referelant in excess of the ncing of each p0. 63 initial 20 C) Financial loss of each individual plant 13.46 D) Loss of interest for individual plant 1.8 Total 92.17 Copyright © 2012 SciRes. 289  R. FRATINI ET AL. Table 5. Caseline. osts for 5 and 10 plants additional to b Coltural operation No. 5 plants (€) No. 10 plants (€) a) Georeferencing cost of of the first twenty plants 76.28 76.28 b) The cost f the plant of geo-referencing o in excess of the initial 20 3.13 6.25 c) Financial loss to individual plant 67.32 134.64 d) Loss of interest on investments reported single plant 9.01 18.03 Total 155.74 235.20 Lost income and higher costs per year 22.25 33.60 The cost defined for a single plant releyonre- scribed twenty is forecast at € 92.17. Over tht seven therual vf losue nd higher costs totaling the amount € 22.25 when five plants e are no obligatory practices. - mleast 3 other interventions of this type during th r- fother year (the third, fifth and seventh year of co am enue and higher costs (3 mod- er e and higher costs is hi ding, with subsequent tting logs increase in revenues /shredding costs ay or ch nue and higher costs we first m wing Table 7 shows the chipping cost per hectare of is convenient in situations where mechanical eq lly it is impossible in each individual request that the ased be e nexd the p years, efore, we must consider the annalue ot reven a are released and € 33.60 if there are 10 plants. Another forest environmental commitment that we have analyzed is “Cleaning and mowing grass and shrub vegetation in the forests and other measures for the protection of structural biodiversity”. b) Cutting the shrubs of the open areas within forests or wooded areas treated when included in or adjacent to a forest. Baseline: Ther Effect on revenue component (R*): There are no effects on revenues. Effect on cost component (C*): costs of scrub removal and mowing. The action involves scrub clearance in the first year com itment and at e remaining time of commitment; the work must be pe rmed every o mmitment). Table 7 shows the variables and the related costs for me- chanical mowing per hectare. The calculation reported above of machine hours and labor hours accrued has been achieved on the basis of the information contained in the price list for regional operations and forestry workers (Regione Toscana, 2008). Therefore, the costs per hectare of cultivation operations Table 6. Cost of tending. ounted to € 604.10 for the scrub clearance on land moder- ately invaded by grasses and shrubs and € 302.05 for clearance on lands invaded by low weeds. The annual amount of lost rev ate clearings); 3 years are considered, amounting to € 215.75 per year ((€ 604.10 + (302.05 × 3): 7). Therefore, the amount of lost revenu gher than expected, i.e., € 200.00 per hectare. c) Debris management processing Obligation of removing and/or shred distribution of wood debris on the ground; it is forbidden to burn the waste on site. Baseline: obligation of spli Effect on revenue component (R*): derived from sale of timber assortments. Effect on cost component (C*): chipping of waste material per hectare and distribution on site. The action requires that the scraps must be taken aw ipped and/or shredded (manually or mechanically), with subsequent distribution on the ground: it is forbidden to burn them except for reasons of plant pathology (on the area where forest operations are carried out). For the calculation of lost reve ade an appraisal of the average quantity of waste material per hectare. Then, by calculating the average productivity of a chipper, we computed the relative cost per hectare for the chip- ping of slash determined before. Therefore for the calculation of the quantities of slash per hectare reflecting the species, type of management and age of the plant we referred to the studies (Bernetti, 1987; Spinelli, 1999; Bernetti, et al., 2004). At the same time to evaluate the cost of chipping, according to its average efficiency, the experience was sought from industry experts. The follo the waste material left on site (inclusive of the forest opera- tion of wood material), for the most common types of forest in Tuscany classified according to species, class fertility and age. The result includes the cost of distribution of wood chips on the ground. Chipping uipment has easy access and where there is a viable market for wood chips. This is true in particular where the orographic conditions, the forest road system and the market determine advantages and disadvantages for the processing of forest re- siduals. Norma Hours/Hectare €/Hour €/Total Mechanical chaining carried out on field medium invaded by grasses and shrubs, accommodation and removal of debris Tractor equipped and specialized worker 10.0 60.4 604.1 Mechanical chaining carried out on field low invaded by grasses a nd sh rubs, accommoda ti on and removal o f d ebris Tractor equipped and specialized worker 5.0 60.4 302.1 Copyright © 2012 SciRes. 290  R. FRATINI ET AL. Table 7. Cost of collection, chipping and spreading of slash. ID Species Cost of chpping per hectare (€/hecCosts chipping and split of slash Costs spreading Sale c tare) left on the ground per €/hectareper hectare (€) hips Cs net (€/hectare) osts chip revenue (€) 1 Maritime pine 1317 1129 270 1981 735 2 Maritime pine 785 673 270 1180 548 3 Ma ritime pine943 808 270 1418 603 4 Douglas fir 2131 1826 270 3204 1023 5 Black pine 997 855 270 1500 622 6 Black pine 777 666 270 1168 545 7 Black pine 521 446 270 783 454 8 Black pine 1334 1143 270 2005 742 9 Black pine 1070 917 270 1609 648 10 B lack pine 877 752 270 1319 580 11 B lack pine 919 788 270 1382 595 12 B lack pine 778 667 270 1170 545 13 B lack pine 635 544 270 955 494 Table 8. Suary tavenue and hiosts calculated. mmble of lost regher c €/her Kind of forest-e nvironommitments ment cectare p Year 1) Selection of species subject to utilization. a) Releas e of one or more plants per hectare selected among older species and/ or greater d iameter and wood value, identified € 10.39 per plant according to the criteria defined in Art. No 12 of DPGR 2003/48/Tuscan Region. b) Releas e of at least 5 plants per he ctare seiameter an d wood value , identifi ed accord-lected amo ng older spec i es and/or greater d ing to the criteria defined in Art. No 12 of DP€ 2r 5 2.25 pe GR 2003/48 /Tuscan Region. plats n c) Removal, in conifer and broadleaved stands of plants of aleppo pine, maritime pine and black pine and others conifer especially if dried up, with disease and without commercial value and high flash : from 5 to 20 plants per hectare; € 29.55 from 20 to 40 plants per hectare; € 59.76 more than 40 plants. € 75.70 2) Cub vegetation in the fore s ts and other measures for the prot ection of biodiversity structural. leaning and mowing grass a nd shr Cutting the shrubs in the open areas within forests or wooded areas treated when covered by or neighbouring t o a forest. € 200.0 3) Waste forest managem ent processing. Duty of removal or, alt ernatively, exist the obligation to chipping and/or shredding, with subsequent distribution of wood debris on the ground; it is also for bi dden to burn the debris on the gro und the groun d. € 89.54 4) Impact of forest utiliza tion on soil, shrubbery, on the regeneration a nd wildlife. Use for yarding and hauling by pack animals, crane cable and chute instead of mechanical means. € 104.10 addition n To this end, in determining the entity of lower revenues and higher costs, an analysis of the Tuscan territory was made hich took into account the variables described above. The result of this analysis allowed us to identify an area representa- al cost of chipping be in regulation, when this would ot result as profitable because its costs are not compensated. w Copyright © 2012 SciRes. 291  R. FRATINI ET AL. tive and externalities. Te of s financed by the Region of Tuss Nations Publications. Bernetti, G. (1987). I boschi della Toscana. Quaderni di Monti e Boschi, Giunta Regionale Tos Bernetti, I., Fagarazzi, C methodology to ana- sample of the context within which it is convenient to chip, ove the chips and sell 70% of these. the provision of public goods the single actionrem For the remaining 30% of the residual material, not easily transportable and therefore not sellable, there is expected a partially mechanical chipping and the subsequent homogeneous distribution on the ground; if work with the chipper is not pos- sible, the other part of this can be split into pieces of maximum length of 1 meter and maximum diameter of 5 cm. The average cost of chipping was considered to be equal to € 7 per cubic meter of timber used. The average cost of chipping and shred- ding is considered equal to € 14 per cubic meter of timber used. Despite the wide variability of costs shown in Table 8, giv- ing an average value per hectare is justified; in fact, applying the intervention for each specific situation does not seem war- ranted, considering that detection and control of costs is often greater than the premium paid. Furthermore, this variability reflects the characteristics of the ownership of the forests, often fragmented and scattered throughout the territory. It follows that the average amount of lost revenue and higher cost re- ceived by the individual beneficiary of the intervention is broadly appropriate to the forest structure, itself also quite va- riable. The average cost of the project is equal to €625.54 per hectare. The annual value of lost revenue and higher costs will, therefore, amount to €89.36 per hectare. At the conclusion of the detailed examination of some of the measures provided by Regulation 225 (Council Regulation (EC) No. 1698/2005 and adopted by the Region of Tuscany, we pre- sent in one table (Table 8) the amount of lost revenue and higher costs considering all the measures established by the Regulation. Conclusion Our study was limited to defining a methodology for deter- mining compensation that can completely cover the higher costs and lower revenues (as required by the EU). It would be extremely useful and interesting to complete this research by analyzing the impact and effectiveness of each single action on he choic cany follow more a political path then a technical one (problems in the deci- sion process at national scale). The constraint imposed by the European Community to pay only the higher costs and lower revenues (computed on the basis of market prices) undervalues the production of public goods and prevents their real devel- opment (problems in the political instruments adopted at Euro- pean scale). REFERENCES Bauer J., & Corredor, H. G. (2006). International forest sector institu- tions and policy instruments for Europe: A source book. UNECE- FAO: United cana: Edagricole. ., & Fratini, R. (2004) A lyze the potential development of biomass energy sector: An applica- tion in Tuscany. Forest Policy and Economics, 6, 415-432. doi:10.1016/j.forpol.2004.03.018 Ciancio, O., & Nocentini, S. (2004). Il bosco ceduo. Firenze: Acca- demia Italiana di Scienze Forestali. Hippoliti, G. (1997). Appunti di meccanizzazione forestale. Florence: Studio Editoriale Fiorentino. AFA (1987). Tavole stereometriche ed alsometriche dei boschi ita- liani. Trento. IS S Italian Ministry of Agriculture, Food and Forestry (2009). Policy and good forest management practices baseline measures for the imple- mentation of forestry and environmental. Rete Rurale Nazionale, T ask Force Foreste. Regione Toscana (2008). Modifiche ed integrazioni al prezzario re- gionale per interventi ed opere forestali di cui alla. Bollettino uffi- ciale della regione Toscana, 55. Sherwood (2012). www.rivistasherwood.it/tecniko-pratiko pinelli, R. (1999). Environmental and socio-economic impacts of using excavators and backhoe loaders as base machines in forest. In Proceedings from the first meeting of a concerted action FAIR—CT 98-3381 (pp. 109-116). Garpenber g, 13-17 December 1999. Copyright © 2012 SciRes. 292 |