J. E. HATCHER JR. ET AL.

communication, B. J. Keefer, 8 June 2012); Plum Creek’s ac-

quisition of 39,300 ha dispersed across the state from Geor-

gia-Pacific (personal communication, C. Hall, 7 June 2012);

and The Campbell Group’s acquisition of approximately 4050

ha of timberland from Georgia-Pacific and International Paper

(personal communication, J. Shore, 7 June 2012).

Numerous small private equity firms have also been involved

in the acquisition of industrial timberlands over the last decade.

Crescent Resources, a real estate development group based out

of Charlotte, NC, acquired 3000 ha in the Piedmont and North-

ern Coastal Plain from Bowater (personal communication, J.

Short, 5 June 2012) and American Timberlands Company ac-

quisition 8100 ha in Horry County from International Paper

(American Timberlands Company, 2012).

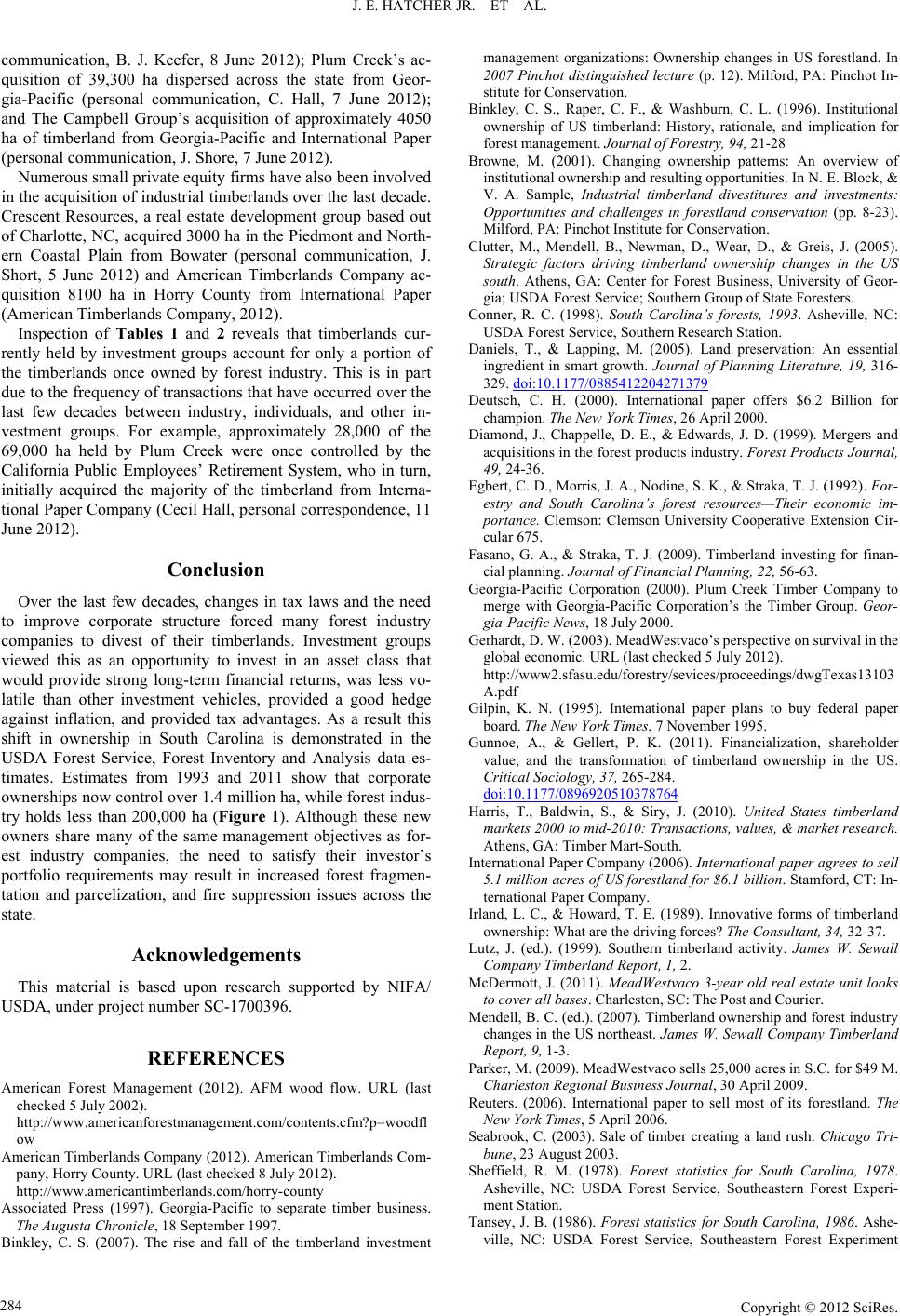

Inspection of Tables 1 and 2 reveals that timberlands cur-

rently held by investment groups account for only a portion of

the timberlands once owned by forest industry. This is in part

due to the frequency of transactions that have occurred over the

last few decades between industry, individuals, and other in-

vestment groups. For example, approximately 28,000 of the

69,000 ha held by Plum Creek were once controlled by the

California Public Employees’ Retirement System, who in turn,

initially acquired the majority of the timberland from Interna-

tional Paper Company (Cecil Hall, personal correspondence, 11

June 2012).

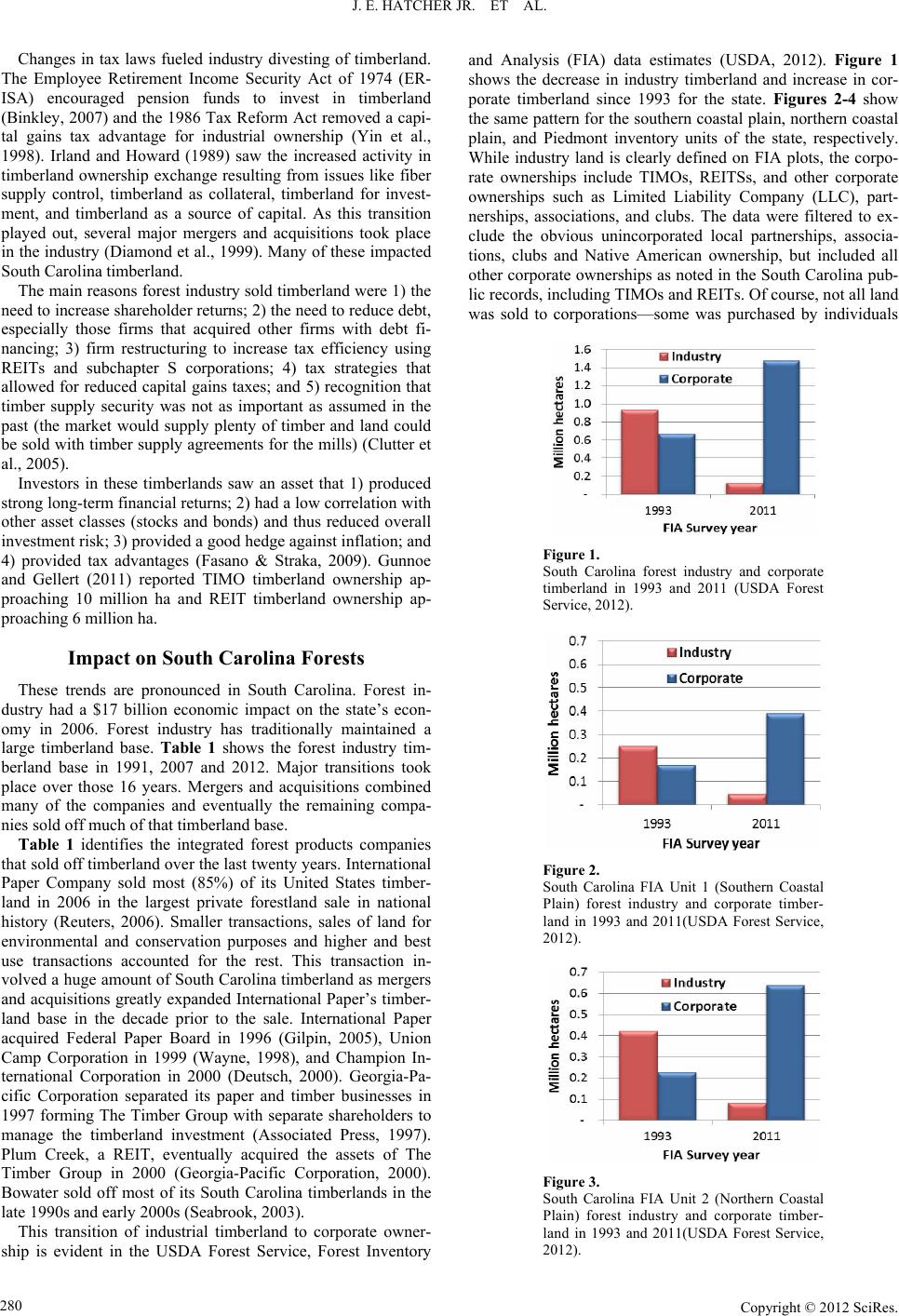

Conclusion

Over the last few decades, changes in tax laws and the need

to improve corporate structure forced many forest industry

companies to divest of their timberlands. Investment groups

viewed this as an opportunity to invest in an asset class that

would provide strong long-term financial returns, was less vo-

latile than other investment vehicles, provided a good hedge

against inflation, and provided tax advantages. As a result this

shift in ownership in South Carolina is demonstrated in the

USDA Forest Service, Forest Inventory and Analysis data es-

timates. Estimates from 1993 and 2011 show that corporate

ownerships now control over 1.4 million ha, while forest indus-

try holds less than 200,000 ha (Figure 1). Although these new

owners share many of the same management objectives as for-

est industry companies, the need to satisfy their investor’s

portfolio requirements may result in increased forest fragmen-

tation and parcelization, and fire suppression issues across the

state.

Acknowledgements

This material is based upon research supported by NIFA/

USDA, under project number SC-1700396.

REFERENCES

American Forest Management (2012). AFM wood flow. URL (last

checked 5 July 2002).

http://www.americanforestmanagement.com/contents.cfm?p=woodfl

ow

American Timberlands Company (2012). American Timberlands Com-

pany, Horry County. URL (last checked 8 July 2012).

http://www.americantimberlands.com/horry-county

Associated Press (1997). Georgia-Pacific to separate timber business.

The Augusta Chronicle, 18 September 1997.

Binkley, C. S. (2007). The rise and fall of the timberland investment

management organizations: Ownership changes in US forestland. In

2007 Pinchot distinguished lecture (p. 12). Milford, PA: Pinchot In-

stitute for Conservation.

Binkley, C. S., Raper, C. F., & Washburn, C. L. (1996). Institutional

ownership of US timberland: History, rationale, and implication for

forest management. Journal of Forestry, 94, 21-28

Browne, M. (2001). Changing ownership patterns: An overview of

institutional ownership and resulting opportunities. In N. E. Block, &

V. A. Sample, Industrial timberland divestitures and investments:

Opportunities and challenges in forestland conservation (pp. 8-23).

Milford, PA: Pinchot Institute for Conservation.

Clutter, M., Mendell, B., Newman, D., Wear, D., & Greis, J. (2005).

Strategic factors driving timberland ownership changes in the US

south. Athens, GA: Center for Forest Business, University of Geor-

gia; USDA Forest Service; Southern Group of State For es te rs.

Conner, R. C. (1998). South Carolina’s forests, 1993. Asheville, NC:

USDA Forest Service, Southern Research Station.

Daniels, T., & Lapping, M. (2005). Land preservation: An essential

ingredient in smart growth. Journal of Planning Literature, 19, 316-

329. doi:10.1177/0885412204271379

Deutsch, C. H. (2000). International paper offers $6.2 Billion for

champion. The New York Times, 26 April 2000.

Diamond, J., Chappelle, D. E., & Edwards, J. D. (1999). Mergers and

acquisitions in the forest products industry. Forest Products Journal,

49, 24-36.

Egbert, C. D., Morris, J. A., Nodine, S. K., & Straka, T. J. (1992). For-

estry and South Carolina’s forest resources—Their economic im-

portance. Clemson: Clemson University Cooperative Extension Cir-

cular 675.

Fasano, G. A., & Straka, T. J. (2009). Timberland investing for finan-

cial planning. Journal of Financial Planning, 22, 56-63.

Georgia-Pacific Corporation (2000). Plum Creek Timber Company to

merge with Georgia-Pacific Corporation’s the Timber Group. Geor-

gia-Pacific News, 18 July 2000.

Gerhardt, D. W. (2003). M ea dWestvaco’s perspective on survival i n th e

global economic. URL (last checked 5 July 2012).

http://www2.sfasu.edu/forestry/sevices/proceedings/dwgTexas13103

A.pdf

Gilpin, K. N. (1995). International paper plans to buy federal paper

board. The New York Times, 7 November 1995.

Gunnoe, A., & Gellert, P. K. (2011). Financialization, shareholder

value, and the transformation of timberland ownership in the US.

Critical Sociology, 37, 265-284.

doi:10.1177/0896920510378764

Harris, T., Baldwin, S., & Siry, J. (2010). United States timberland

markets 2000 to mid-2010: Transactions, values, & market research.

Athens, GA: Timber Mart-South.

International Paper Company (2006). International paper agrees to sell

5.1 million acres of US forestland for $6.1 billion. Stamford, CT: In-

ternational Paper Company.

Irland, L. C., & Howard, T. E. (1989). Innovative forms of timberland

ownership: What are the driving forces ? The Consultant, 34, 32-37.

Lutz, J. (ed.). (1999). Southern timberland activity. James W. Sewall

Company Timberland Report, 1, 2.

McDermott, J. (2011). MeadWestvaco 3-year old real estate unit looks

to cover all bases. Charleston, SC: The P ost a nd Cou rier.

Mendell, B. C. (ed.). (2007). Timberland ownership and forest industry

changes in the US northeast. James W. Sewall Company Timberland

Report, 9, 1-3.

Parker, M. (2009). MeadWestvaco sells 25,000 acres in S.C. for $49 M.

Charleston Regional Business Journal, 30 April 2009.

Reuters. (2006). International paper to sell most of its forestland. The

New York Times, 5 April 2006.

Seabrook, C. (2003). Sale of timber creating a land rush. Chicago Tri-

bune, 23 August 2003.

Sheffield, R. M. (1978). Forest statistics for South Carolina, 1978.

Asheville, NC: USDA Forest Service, Southeastern Forest Experi-

ment Station.

Tansey, J. B. (1986). Forest statistics for South Carolina, 1986. Ashe-

ville, NC: USDA Forest Service, Southeastern Forest Experiment

Copyright © 2012 SciRes.

284