L. ZYSBERG

Method

Settings an d S tu dy Design

The study was conducted in a large financial organization

providing investment services to a broad range of clients, in

Israel. The organization employs about 7000 individuals, about

66% of whom are based in 180 branches nationwide. Data col-

lection took place in a series of specially designed assessment

centers used for the selection of Investments department man-

agers. The position is considered mid-tier management and is

open to inside employees only, typically investment profes-

sionals without official managerial background (though many

have some training in management).

Sample

One hundred and eighty candidates took part in ACs for the

above job, after applying for an internal call for candidates, and

passing a basic screening process based on their resumes. Of

the above sample, 75 were placed in managerial positions with-

in 6 month s following the AC. For this sample, ages ranged 29 -

50 (mean age = 41.00; sd = 7.65), 60% were men and 40%

were women. Tenure with the company at the time of applica-

tion ranged 5 - 25 years. They all had at least a Bachelor’s de-

gree and 20% had a graduate level degree or equivalent.

Instruments

Assessment centers were specially designed for this position

by a team of expert Industrial-Organizational psychologists

working for the organization, to reflect behaviors according to

the job description provided by the organization HR division.

The assessment centers included: 1) A self- presentation task in

which participants planned and performed a time-limited self-

presentation; 2) A discussion group, simulating professional

credit-approva l dilemmas in whic h consensus has to be reached

via discussion; 3) A group “in-basket” assignment simulating

daily assignments of an investment department manager and 4)

A competitive ‘branch promotion event’ assignment in which 2

or more sub-groups competed on designing and presenting the

best promotion event for a new investment product. These tasks,

though tailored for the specific job and organization are based

on widely used paradigms (see for example: Bray & Grant,

1966; Thornton & Gibbons, 2009).

Data from 10 groups (total n = 75) was included in this

analysis. The data was summarized across 6 dimensions rated

by 2 observers (one is an HR specialist and the other an I/O

psychologist from outside the organization). The two observers

discussed each candidate after the AC and reached consensus as

for the grade on each dimension, as well as a general recom-

mendation regarding the candidate’s fit for the position. Grades

were given on a Stanine scale. The dimensions were as follows:

1) General cognitive ability: problem solving, effective infor-

mation processing; 2) Work style: planned, orderly perform-

ance, paying attention to technical details while keeping awa-

reness of the group goals; 3) Interpersonal relations: open, ef-

fective and assertive communication, collaboration and sensi-

tivity to others; 4) Service & Sales orientation: service aware-

ness, perceiving client-oriented service as a priority, identifying

and taking opportunities to broaden the business and customer

base; 5) Organizational commitment: Embracing organiza-

tional values and priorities, identification with the organization

and its interests; 6) Leadership potential: initiating action, as-

suming responsibilities and motivating others. These dimen-

sions fit a model of generalized dimension structure presented

in a meta-analysis of a large number of studies of assessment

centers (Arthur, Day, McNelly, & Edens, 2006).

Demographic data was collected via a short questionnaire.

Data analysis included gender, age, and tenure.

Criterion data—bonus for managerial performance: as a cri-

terion for managerial performance we collected data regarding

the managers’ performance-based bonus, at the end of the year

following the AC. Bonus is calculated and paid by the HR divi-

sion, ranges 0 to 30 units, each unit representing a given per-

centage of the employee’s monthly salary. Bonus is paid once a

year only in branches reaching or surpassing their business

objectives and goals. Differential bonus is awarded based on

profits, and performance appraisal provided by the employee’s

supervisor. Though there is room for personal judgment, bonus

sums are monitored carefully by the corporate office and super-

visors are held liable for the fairn ess a nd perf ormance cong ru-

ency of the process. Thus it is assumed that this data is a valid

indication of managerial performance through the corporate

lens.

Procedure

After obtaining the organization’s approval for data collec-

tion, we retrieved data from the corporate files making sure no

identifying markers are left in the data to allow tracing indi-

viduals, thus assuring anonymity.

The data was then analyzed using SPSS 19.0 (IBM, 2012).

Results

Before testing the hypotheses we examined the distribution

of our main variables and the general associations among them.

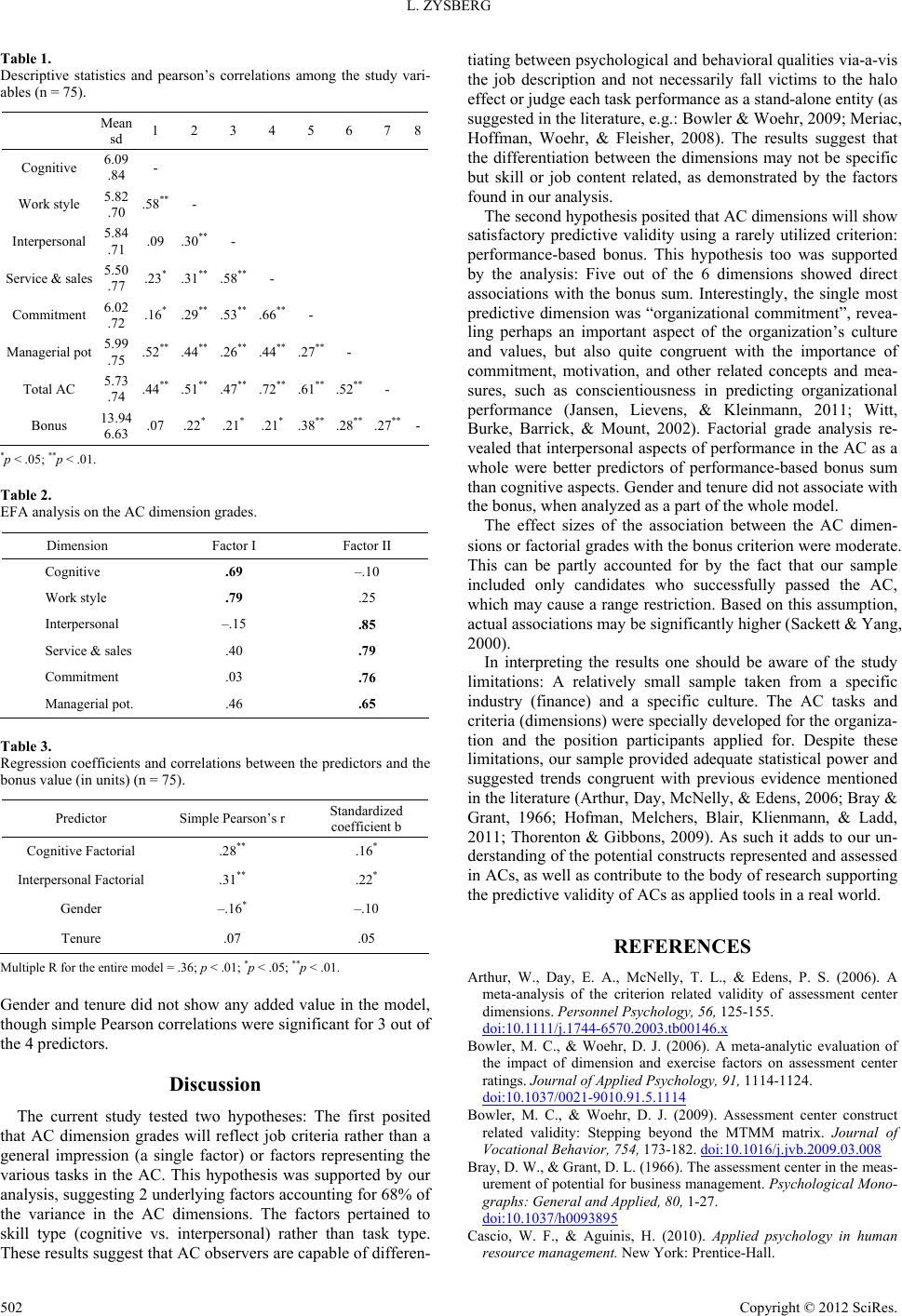

Table 1 summarizes descriptive statistics and Pearson’s corre-

lations between the study variables.

The results reveal a distribution of grades and the bonus units

allowing for parametric statistical analysis (Coolican, 2010).

The analysis shows that 5 of the 6 dimension ratings in the

AC correlated positively with the bonus criterion. “Organiza-

tional commitment” showed the strongest association while

“cognitive skills” did not associate with the criterion at all. The

correlations reveal association patterns within the AC dimen-

sions suggesting underlying factors. The correlations also indi-

cate moderate associations between various AC dimension

grades, the AC final recommendation grade and the bonus

value.

We then proceeded to conduct an exploratory factor analysis

(EFA) to reveal potential factors within the AC dimensions.

The Varimax rotated model accounted for 68% of the total

variance suggesting 2 factors. Table 2 depicts the EFA results.

The 2 factor structure matches a conceptual differentiation

between cognitive/intellectual aspects and interpersonal aspects

of performance in the AC. We then calculated a mean score for

dimensions loading on the Cognitive factor and the dimensions

loading on the Interpersonal factor. We used these factorial

scores in a regression analysis, as well as tenure and gender to

predict the bonus value. Table 3 summarizes the results of the

analysis.

The results show that a multiple R of .36 (p < .01) was ac-

counted for by the interpersonal and cognitive factor grades.

Copyright © 2012 SciRes. 501